For the trade details click on this link to the trades

We all know by now or should that this is a very overextended and disconnected from reality market. Extraordinary liquidity and compassionate finance largess from the Federal Reserve keeps the rally alive. Value is hard to come by and insiders are telling you as much. There will always be something of value to buy but the companies insiders are still buying into are increasingly obscure.

Allied Esports Entertainment up 26.17% was the standout performance-wise for the week. Knighted Pastures LLC bought 552,862 shares of AESE at $1.14. Insiders have been selling all year so this is a noticeable turnabout. AESE is easily confused with Esports Entertainment which trades under the appropriate symbol GMBL. To make things even more complicated, they worked together to draw 1.7 million unique viewers for the VIE.gg CS:GO Legend Series tournament, which ended Sunday, September 13. The two-week competition, which also generated over 1 million hours watched and reached 98,000 peak viewers, is the most-watched Legend Series event since the tournament series was created in 2017.

I am still trying to figure out exactly what this company does and who Knighted Pastures is ( not a good sign in either case), but I am intrigued by a company that has management selling all year and now someone is buying this penny stock and of course, all matter of video games is one of the main beneficiaries from the Pandemic. As part of my due diligence, the two things I recommend all investors to do is read the 10K business description as you might find a coherent explanation of the business particularly separated from all the marketing hype. Then LISTEN not read the transcript of the latest earnings call to try to pick up some of the body languages of management.

Named to Fast Company’s World’s Most Innovative Companies list for 2019, Allied Esports is a premier esports entertainment company with a global network of dedicated esports properties and content production facilities. Its mission is to connect players, streamers and fans via integrated arenas and mobile esports trucks around the world that serve as both gaming battlegrounds and every day content generation hubs. I guess this is putting people together and turning video gaming into a spectator sport. If you’ve ever watched your millennial and Gen Z children play video games with their friends in your house, you’ve probably been amazed as I have that people will watch other people play video games. Allied Esports’ locations currently include 11 properties in the top three esports markets across the globe: North America’s HyperX Esports Arena Las Vegas; HyperX Esports Truck “Big Meta”; Esports Arena Orange County and Esports Arena Oakland; Europe’s HyperX Esports Truck “Big Betty” and HyperX Studio in Hamburg, Germany.

Amazon realized there was a market there when they bought Twitch for 970 Million cash in 2014. According to Wikipedia-As of February 2020, it had 3 million broadcasters monthly and 15 million daily active users, with 1.4 million average concurrent users. So to be clear AESE is about crowds gathering together to watch gamers playing with fellow gamers all around the world. While Activision, Take-Two, Amazon, and YouTube build and grow the virtual gaming market, it’s inevitable that some of it will spill over the real world gathering and AESE is the prime beneficiary of that. The Company has never made money and is burning cash. With just 5.7 million in the bank and burning $6.5 million in the last quarter, it will have to do something to fix the balance sheet while management sorts out their strategy. I’d have my bankers on the phone with Google or Amazon to broker a deal ASAP.

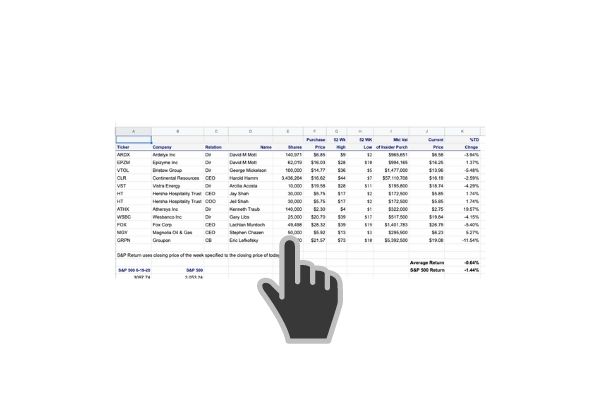

ARDELYX Inc up 13.46% Director Mott bought 170,000 shares at $5.89. Mott is a principal in NEA Associates, one of the leading venture capital firms. ARDX spiked 13% on the news. Their lead candidate tenapanor, discovered and developed by Ardelyx, is a first-in-class, targeted therapy for the treatment of hyperphosphatemia in patients with chronic kidney disease (CKD) on dialysis. Tenapanor has a unique mechanism of action and acts locally in the gut to inhibit the sodium/hydrogen exchanger 3 (NHE3). This results in a conformational change of the epithelial cell junctions, reducing permeability specific to phosphate, resulting in decreased phosphate absorption through the paracellular pathway, the primary pathway of dietary phosphate absorption.

Following successful clinical development, they have filed for U.S. regulatory approval of tenapanor for the control of serum phosphorus in adult patients with CKD on dialysis. If approved, tenapanor would provide a novel approach for the treatment of hyperphosphatemia (elevated serum phosphorus), a major co-morbidity factor in people with CKD and a significant unmet medical need.

Tricida Inc. up 10.77% After a massive crash and burn, CFO Parker is back nibling at TCDS with 15,000 shares at $6.78. The last time he purchased shares was before the FDA sent their drug application packing and he purchased $1Million worth at $30.09 per share.

Tricida, Inc., is a pharmaceutical company focused on the development and commercialization of its investigational drug candidate, veverimer (also known as TRC101), a non-absorbed, orally-administered polymer designed to treat metabolic acidosis in patients with chronic kidney disease (CKD). Metabolic acidosis is a chronic condition commonly caused by CKD that is believed to accelerate the progression of CKD, increase the risk of muscle wasting and cause the loss of bone density.

This is a big opportunity for the Company. After the previously mentioned setback, Tricida revised the protocol for its VALOR-CKD outcome trial. The revised protocol has a group sequential design, no interim analysis for sample size adjustment, and unblinded interim analyses for early stopping for efficacy after 150 primary endpoint events, anticipated in the second half of 2021, and 250 primary endpoint events, anticipated in mid-2022, have accrued. The interim analyses will be conducted by an independent unblinded Interim Analysis Committee, and the trial will remain blinded unless it is stopped early for efficacy. If this trial is successful, Tricida intends for it to serve as the confirmatory trial for accelerated approval or form the basis for traditional approval of veverimer.

Tricida currently has the financial resources to fund its operations into at least mid-2022, prior to modifying any of its material agreements. Cash, cash equivalents and investments as of September 30, 2020 were approximately $376M. Tricida currently has $75M principal amount of debt which has a final maturity of April 2023 and has $200M in outstanding principal amount of 3.5% Convertible Senior Notes which mature in May 2027.”

ATLAS TECHNICAL CONSULTANTS Inc up 6.63% Several insiders are buying ATCX, the largest purchase being CFO Quinn’s purchase of 75,000 shares at $5.81. Atlas provides professional testing, inspection, engineering, environmental, and consulting services from more than 100 locations nationwide. They deliver solutions to both public and private sector clients in the transportation, commercial, water, government, education, and industrial markets. We mentioned this name as a good way to plan a potential infrastructure bill from the new Biden administration. If the Democrats take the Senate with a sweep of the upcoming Georgia senate runoffs, expect ATCX to rock. Even without a Democratic win, pundits say this is something where Republicans and Democrats may find bipartisan agreement.

ESCALADE INC up 5.81% Director Glazer purchased 20,884 shares of ESCA at $18.59. Escalade, Incorporated (Escalade) has manufactured and distributed sporting goods and recreational equipment for over 95 years. Leaders in their respective categories, Escalade’s brands include Bear Archery and Trophy Ridge archery accessories; STIGA® and Ping-Pong® table tennis; Accudart® and Unicorn® darting; Onix™ pickleball equipment; Goalrilla™, Goalsetter®, Goaliath® and Silverback® residential in-ground basketball systems; the STEP® fitness products; Woodplay® premium playsets; Cue and Case Sales – a leader in specialty billiard accessories; and Lifeline – a leader and innovator in personal fitness products. Escalade Sports products are available at sporting goods dealers and independent retailers nationwide.

This is a very reasonably priced debt-free company having a great year. The Pandemic has clearly added to the consumer at home sporting demand. A director bought $612k of shares at $11.42 back in June. At 11.9 times trailing earnings, Escalade is a buy.

HC2 HOLDINGS Inc up 4.76%

MANNKIND CORP up 3.11% up I will have to see more than $100,000 of insider buying at Mankind before I’ll get interested. MannKind Corporation is a biopharmaceutical company focusing on the discovery, development, and commercialization of therapeutic products for diseases such as diabetes and pulmonary arterial hypertension. Based in Westlake Village, California, the company was founded in February 1991

BlackRock Capital Allocation Trust up 2.47% It’s encouraging when you see the portfolio manager upping his ownership. That’s what Richard Rieder did when he purchased 18,182 shares at $22.28. It’s odd to see one of these trusts trading at a premium to NAV when so many are at a discount. BlackRock Capital Allocation Trust’s (BCAT) (the ‘Trust’) investment objectives are to provide total return and income through a combination of current income, current gains and long-term capital appreciation. The Trust invests in a portfolio of equity and debt securities. Generally, the Trust’s portfolio will include both equity and debt securities. At any given time, however, the Trust may emphasize either debt securities or equity securities. The Trust utilizes an option writing (selling) strategy in an effort to generate current gains from options premiums and to enhance the Trust’s risk-adjusted returns. The Trust began trading in the Fall and has appreciated with the market.

MultiPlan Corp up 2,17% Real money is trading hands here in this battleground stock. We love it when a Company is the subject of a well planned and publicized short-seller attack and instead of just responding by just disputing the accusations, they back it up with material buying of their shares by management, institutional shareholders, and members of the board of directors. On November 11th, short-seller Muddy Waters announced a new short position in MPLN.

12-4-20 Hellman and Friedman 10% shareholder added 1,7172 shares at $8.29

12-2-20 Director August purchased 826,265 shares at $6.99

11-17-20 President Galant bought 28,550 shares at $7.08

11-16-20 Director Klein purchased 700,000 shares at $7.11 and on 11-16 he purchased 741,999 shares at $6.59

MultiPlan was founded in 1980. It announced it was merging with Churchill III, the third SPAC created by Churchill Capital. If you don’t know what a SPAC is by now, you’re living under the proverbial investment rock.

Churchill Capital Corp III CCXX.N, a special purpose acquisition company (SPAC), and MultiPlan Inc said they have reached a definitive agreement to merge in a deal worth about $11 billion that will take the U.S. healthcare services firm public. The deal at the time of its announcement in July represented the largest-ever SPAC merger, said Multiplan parent Hellman & Friedman (H&F). The merged company will operate under the name MultiPlan, which will be listed on NYSE, the companies said in a joint statement on Sunday, adding that the deal will expand MultiPlan’s data analytics platform.MultiPlan will receive up to $3.7 billion of new equity or equity-linked capital that will reduce the firm’s debt. The transaction includes $1.3 billion worth of fully committed common stock at $10 a share and $1.3 billion in convertible debt, convertible at $13 per share.

MultiPlan Chief Executive Mark Tabak will be CEO of the combined company, with David Redmond staying on as chief financial officer. As a public company, MultiPlan will be better equipped to expand organically with adjacent mergers and investments in new technology, Tabak said.

Under the deal, Churchill, which went public in February, will provide up to $1.1 billion of cash raised during its initial public offering (IPO). MultiPlan will continue to operate its business with a relentless focus on delivering service excellence to its payer customers. The existing management team, led by long-standing CEO Mark Tabak, CFO David Redmond and Chief Revenue Officer Dale White, will continue to lead the business, and Hellman & Friedman affiliates (“H&F”) will remain MultiPlan’s largest shareholder.

The capital from this transaction, combined with Churchill’s expertise, will enable MultiPlan to continue to enhance its core offerings to payers through a significant increase in its data analytics platform, extend into new payer customer segments and expand its platform, increasing the value MultiPlan provides to more than 700 payers, their 60 million consumers and MultiPlan’s 1.2 million providers that serve them. Further, the transaction will better position MultiPlan to capitalize on the entire $50 plus billion total addressable market, rather than its current subset of $8 billion, organically and through M&A.

Allen Thorpe, Partner at Hellman & Friedman, said, “MultiPlan’s performance as a privately held company has been outstanding. This transaction strengthens the Company and will allow it to further penetrate the broad and fast-growing healthcare market, driving efficiencies and cost savings that benefit the sector and deliver great outcomes for payers, providers and consumers.” He further added, “We are excited to join forces with the Churchill team and continue our partnership with MultiPlan to deliver value for its many customers.”

“We are pleased to partner with MultiPlan to drive its next phase of growth. MultiPlan is on the right side of healthcare, significantly reducing costs to insurers, employers and consumers,” said Michael S. Klein, Chairman and CEO of Churchill. “MultiPlan has an unmatched, long-term track record of customer satisfaction and delivering high returns to investors. This transaction will enable the Company to enhance its capital structure and position it for substantial incremental growth. MultiPlan fits perfectly with Churchill’s core mission to provide intellectual and financial capital to power the growth of great, market leading companies who operate in attractive industries, and can succeed more rapidly in the public markets with increased capital and the benefit of Churchill’s Operating and Strategic Partners.”

In October of 2020, combined with Churchill III a SPAC merged into the Company effecitvely bringing it public. On October 12, H&F Investors disclosed a 32% stake. On October 30th, MPLN filed to sell 633.7M shares of stock for holders. Basically this is all the shares in the company so I think it’s got more to do with the mechanics of merging into the SPAC than everyone selling out. I plan on calling the Company to find out more about this if I can’t figure it out from the

So what exactly is Multiplan? Taken from the 10K, the Company combined uses technology-enabled provider network, negotiation, claim pricing and payment accuracy services as building blocks for medical and dental payors to customize the healthcare cost management programs that work best for them. MultiPlan is a leading value-added provider of data analytics and technology-enabled end-to-end cost management solutions to the U.S. healthcare industry as measured by revenue and claims processed. MultiPlan delivers these critical solutions through the following offerings:

- Analytics-Based Services, which reduce medical costs for consumers and payors via data-driven algorithms which detect claims anomalies;

- Network-Based Services, which reduce medical costs through contracted discounts with healthcare providers and include one of the largest independent preferred provider organizations in the United States; and

- Payment Integrity Services, which reduce medical costs by identifying and removing improper and unnecessary charges before claims are paid.

Black Knight Inc. down -0.94% Director Otting purchased 2,222 shares at $90 per share on 12-2 and followed on 12-4 with 3,383 more at $88.66 Otting, former Comptroller of the Currency joined the board of BKI in June so I am not jumping up and down over this. Directors usually own some stock in companies that they sit on the boards of. But it was in June, so the timing is interesting.

CuriosityStream Inc. down -1.59% Director Hendricks bought 78,000 shares of CURI at $8.99 per share. Curiosity Stream is a streaming service for the relentlessly curious. You get access to thousands of documentaries for $15 per year. Curisoity Stream went public by way of a SPAC. How unusual, right? Scott Devitt of Stifel anlayst initiated coverage of CuriosityStream with a Buy rating and $12 price target, telling investors that he sees upside opportunity given the company’s veteran operators, multiple global content monetization opportunities, and current equity value of under $400M. Devitt notes that CuriosityStream was created by John Hendricks, the founder of the Discovery Channel and former Chairman of Discovery Communications. B. Riley on the same day put a buy on CURI with a target of $16. Sadly enough the Company filed to sell 13.89 M shares of stock on November 20th, putting an end to a rally it was having.

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019

[…] is not the first time he purchased shares either. We blogged about it when it was $8.99 per share, about half of what it is trading at now. Seriously can you afford not […]