The S&P was up 1.84% for the week on top of last week’s 2% run. New index highs are the norm but there was scant insider buying. Corporate officers and directors brazenly unloaded hundreds of $millions dollars worth of company stock during the earnings blackout period, shielded by the loophole that 10b5-1 provides. This post will examine the few hardy souls that stepped up and bought their company’s stock.

Name: Staglin Garen K

Position: Director

Shares Bought: 2,500, Average Price Paid: $107.12 Cost: $267,800

Company: ExlService Holdings Inc. (EXLS)

EXL Service is an American multinational professional services company mainly involved in operations management and analytics. EXL offers insurance, banking, financial services, utilities, healthcare, travel, transportation, and logistics services. The Company is headquartered in New York and has more than 31,000 professionals in locations throughout the United States, Europe, Asia, Latin America, Australia, and South Africa. ExlService Holdings Inc. (EXL) is a leading operations management and analytics company that helps its clients build and grow sustainable businesses. By orchestrating its domain expertise, data, analytics, and digital technology, EXL looks deeper to design and manage agile, customer-centric operating models to improve global operations, drive profitability, enhance customer satisfaction, increase data-driven insights, and manage risk and compliance. Headquartered in New York, EXL has approximately 31,900 professionals in locations throughout the United States, the United Kingdom, Europe, India, the Philippines, Colombia, Canada, Australia, and South Africa. EXL serves customers in multiple industries, including insurance, healthcare, banking, financial services, utilities, travel, transportation and logistics, media, and retail.

Garen K. Staglin has served as Independent Chairman of the Board of the Company since 2014. Mr. Staglin has over 40 years of experience in the financial services and technology industries. Based in part on Mr. Staglin’s expertise in the financial services and technology industries and his experience as a member of public company boards of directors, the Company has concluded that Mr. Staglin should serve as a director. Mr. Staglin is an investor in several private companies and hedge funds and is a Special Limited Partner for FT Ventures, a $600 million equity firm headquartered in San Francisco, California. FT Ventures is an investor in EXL Service.

Opinion: I wish all the stocks I owned had charts that looked like the one above. This is a pretty notable transaction by Staglin since it was part of a 10b5-1 buying program, a rare occurrence indeed. Staglin bought an identical amount of stock just a week ago paying $106.83 per share. Another director bought 1425 shares at $103.38 per share on 6-10-21.

=

Name: Simoncini Matthew

Position: Director

Shares Bought: 22,727, Average Price Paid: $22.00 Cost: $499,994

Name: Heng Jun Hong

Position: Director

Shares Bought: 4,545, Average Price Paid: $22.00 Cost: $99,990

Company: Luminar Technologies Inc. (LAZR)

Luminar (Nasdaq: LAZR) is an autonomous vehicle sensor and software company with the vision to make autonomy safe and ubiquitous by delivering the only lidar and associated software that meets the industry’s stringent performance, safety, and financial requirements. Luminar has rapidly gained over 50 industry partners, including 8 of the top 10 global automotive OEMs. Luminar went public through a SPAC last November backed by Alec Gores, Peter Thiel, Volvo, GoPro founder Nick Woodman, and others.

Luminar claims to have built a new type of lidar from the chip level up, with technological breakthroughs across all core components. Lidar, light detection and ranging radar, measures distance using laser light to generate a highly accurate 3D map of the world around the car. The sensor is widely considered critical to the commercial deployment of autonomous vehicles. Automakers have also begun to view lidar as an important sensor to be used to beef up the capabilities and safety of its advanced driver assistance systems in the new cars trucks and SUVs available to consumers.

LAZR claims to have created the only lidar sensor that meets the demanding performance, safety, and cost requirements to enable Level 3 through Level 5 autonomous vehicles in production, bypassing the traditional limitations of legacy lidar technology. Integrating this advanced hardware with their custom-developed software stack enables a turn-key independent solution to accelerate widespread adoption across automakers at a series production scale.

Matthew Simoncini has over 35 years of experience in the automotive and automotive-related industries in evaluating companies, emerging technologies, and management teams, with significant expertise in due diligence and assessing the suitability of acquisition opportunities. As President and Chief Executive Officer of Lear from 2011 to 2018, Matthew was responsible for the company’s strategic direction and operational leadership. Previously he was Lear’s Chief Financial Officer, responsible for global finance operations. He joined Lear in 1999 after Lear acquired UTA, where he was Director of Global Financial Planning & Analysis. He has also held financial and manufacturing positions with Variety Corporation’s Kelsey-Hayes Company and Horizon Enterprises Inc. He began his career at Touche Ross & Co. and is a certified public accountant.

Jun Hong Heng is the Founder, and Chief Investment Officer of Crescent Cove Advisors, LP (“Crescent Cove”), a technology investment firm focused on working with founders and management teams to build the iconic companies of tomorrow. He is also the Chairman and Chief Executive Officer of COVA Acquisition Corp. Previously, Mr. Heng served as Principal at investment firm Myriad Asset Management from 2011 to 2015, where he focused on Asian credit and equity, including special situations. From 2008 to 2011, he served as Vice President of Argyle Street Management, a spin-off from the Goldman Sachs Asian Special Situations Group.

Opinion: I really can’t get excited over this buy and neither has the market as it’s trading down 8.4% in a week the market was up 1.8%. This was part of a spot 9M share secondary Morgan Stantely did for selling shareholders. Matthew spent almost $500k buying shares. This appears to be more than a perfunctory director-type purchase. Simoncini is a knowledgeable industry insider in his own right so it’s just possible that the market may have gotten it wrong.

Perhaps the reason the secondary didn’t work too well was that the founder, Austin Russell, sold 10,500,000 shares on the offering. I can’t blame the billionaire founder and Stanford dropout for selling a 10% or so portion of his holdings netting him $220 million. It certainly dampens investor appetite with Musk telling the world that pursuing lidar for autonomous driving is a “fool’s errand”.

That could be changing in a very big way though. According to a Bloomberg article citing the Verge

“A Tesla Model Y was photographed in Florida sporting rooftop lidar sensors made by buzzy sensor manufacturer Luminar. The sighting caused a bit of a stir among Tesla watchers, given Tesla CEO Elon Musk’s well-established disdain for the laser sensors commonly used by autonomous vehicle companies to create 3D maps of their environment.

Even more notably, Tesla has reportedly entered a partnership with Luminar to use lidar for “testing and developing,” according to Bloomberg. What exactly this partnership entails we don’t know for sure — neither company is commenting. But it could point to some shortcomings in the technology Tesla is using to power its “Full Self-Driving” driver assist feature.”

According to the company, “In March 2021, we entered into a relationship with SAIC Motor Corporation, the largest automaker in China, pursuant to which Luminar is expected to power the autonomous capabilities and advanced safety features in SAIC’s new R brand vehicles for series production with its industry-leading lidar as well as components of its Sentinel software system. The R brand program is expected to begin series production with Luminar starting in 2022, with the parties’ longer-term goal being widespread standardization across all vehicle lines. As part of the close collaboration, we will also be establishing an office in China to be located in Shanghai alongside SAIC Motor, where SAIC would also be providing local support. The parties expect to deliver the first autonomous production vehicles in China, establishing SAIC’s technology leadership position and Luminar’s production launch in the region.”

The big question is are there too many lidar companies? Already Wired magazine is writing that there are too many lidar companies to survive. Volkswagen recently invested in Aeva, there’s Google’s Waymo and Velodyne, to just name a few. Unfortunately, I can’t answer that question or who the winner or winners will be but there will certainly be a lot of stock for sale in the future.

The first and often last document I look at in researching any company is the 10k. This is the document that has teeth and legal consequences. It’s written by the CEO, CFO, in-house legal counsel, outside lawyers, and the auditor. If it ain’t true, it probably isn’t making it in the 10k.

So how good and unique is Luminar’s technology?

From the company’s 10k “Reflecting roughly nine years of development at this stage (the first five of which were in stealth), Luminar offers a unique lidar architecture and proprietary component-level innovation (built from the chip-level up), resulting in superior range and resolution capabilities, ensuring confidence in perception across a broad set of operational domains and unlocking the next generation of vehicle safety. Our lidar and perception software are built upon a longer wavelength lidar design, which has been widely embraced as necessary to broadly deploy truly autonomous vehicles. As a result, we believe that we are the only provider of lidar for automotive autonomy applications that achieves the industry’s stringent requirements and perception capabilities. Our technological prowess and differentiated approach is supported by an extensive intellectual property portfolio of 93 issued patents, in addition to 84 pending or allowed patents as of February 2021.”

And what about the competition?

As far as I can tell no one has a patent on the underlying concept of lidar. According to Wikipedia

Lidar (/ˈlaɪdɑːr/, also LIDAR, or LiDAR; sometimes LADAR) is a method for determining ranges (variable distance) by targeting an object with a laser and measuring the time for the reflected light to return to the receiver. Lidar can also be used to make digital 3-D representations of areas on the earth’s surface and ocean bottom, due to differences in laser return times, and by varying laser wavelengths. It has terrestrial, airborne, and mobile applications.

Lidar is an acronym of “light detection and ranging”[1] or “laser imaging, detection, and ranging”.[2] Lidar sometimes is called 3-D laser scanning, a special combination of a 3-D scanning and laser scanning.[3]

From the 10K again

Position: Chairman

Shares Bought: 294,118, Average Price Paid: $16.02 Cost: $4,712,505

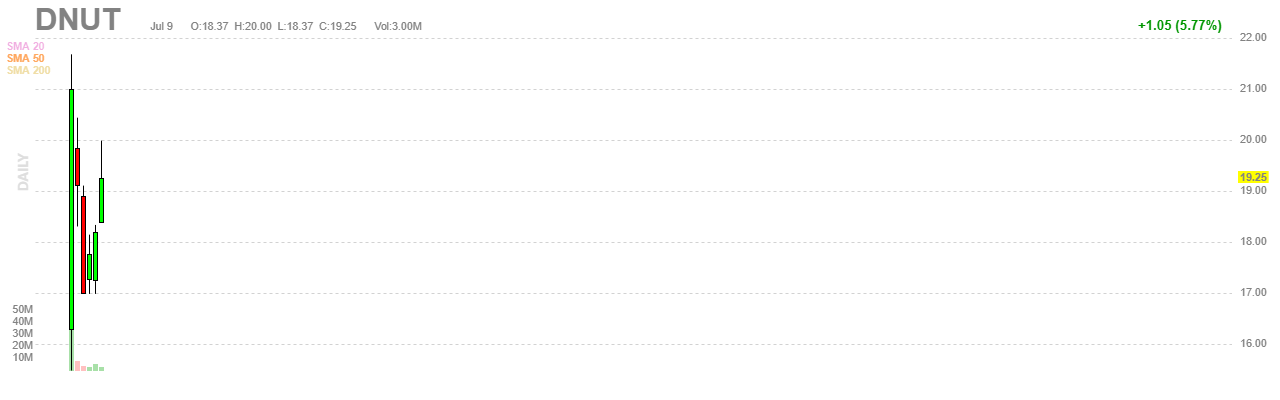

Company: Krispy Kreme Inc. (DNUT)

Krispy Kreme Doughnut Corporation is a global retailer of premium-quality sweet treats, including its signature Original Glazed ® Doughnut. Headquartered in Winston-Salem, N.C., the Company has offered the highest-quality doughnuts and great-tasting coffee since it was founded in 1937. Krispy Kreme Doughnuts is proud of its Fundraising program, which has helped non-profit organizations raise millions of dollars in needed funds for decades. Krispy Kreme doughnuts can be found in approximately 12,000 groceries, convenience, and mass merchant stores in the U.S. The Company has nearly 1,400 retail shops in 33 countries.

Opinion: There ought to be limits on how many times a company can go public, go private, and then public again. Apparently, there are no limits to investor’s naivete and private equity and investment banker greed.

On April 5, 2000, the corporation went public on the NASDAQ at $21 using the ticker symbol KREM. On May 17, 2001, Krispy Kreme switched to the New York Stock Exchange, with the ticker symbol KKD. Krispy Kreme led all IPOs up 543% since Nasdaq topped out that year. By 2005, the company’s stock had lost 75-80% of its value, amid earnings declines, as well as an SEC investigation over the company’s alleged improper accounting practices.

In May 2016, JAB, a secretive European holding company announced it made an offer to purchase the company for $1.35 billion. The transaction closed on July 27, 2016.

JAB, a European holding company has built a coffee empire out of a disparate group of brands including Keurig, Peets, Panera Bread, Dr. Pepper, and Coty, the cosmetics giant. Even the leader of PepsiCo, Indra Nooyi, when asked on an earnings call in 2018 about the logic of JAB. She was quoted as saying “I’m sure there’s some towering strategic logic,” PepsiCo Inc. CEO Indra Nooyi said during a recent earnings call, “but we are still searching for it.”

I think we’ve found the logic. The company went public again on the Nasdaq on July 1, 2021, under the name Krispy Kreme Inc. with a $3 billion valuation and the DNUT symbol.

“With this IPO, we believe JAB Holdings is looking to cash out at the expense of new investors,” the report said. “A $3.6 billion valuation implies Krispy Kreme will reverse its profit nosedive, grow profits by nearly 700% and make more money than quick-service restaurant (QSR) industry incumbents like The Wendy’s Co. (WEN). Such a scenario looks unlikely given the shift in consumer preferences toward healthier foods and the failure of its past growth strategy to achieve the economies of scale needed to operate profitably.”

Position: CEO

Shares Bought: 25,000, Average Price Paid: $8.00 Cost: $200,000

Company: Cel Sci Corp. (CVM)

Cel-Sci Corporation (NYSE American: CVM) is a biotechnology company that is testing drugs for the treatment of cancer, autoimmune and infectious diseases through the research and development of immunotherapy products. CEL-SCI is dedicated to research and development directed at improving cancer treatment and other diseases by utilizing the immune system, the body’s natural defense system. CEL-SCI’s lead investigational therapy, Multikine®* (Leukocyte Interleukin, Injection), is currently being developed as a potential therapeutic agent aimed at harnessing the patient’s immune system to produce an anti-tumor response. Data from Phase I and Phase II clinical trials suggest that Multikine simulates the activities of a healthy person’s immune system, enabling it to use the body’s anti-tumor immune response. Multikine is the trademark we have registered for this investigational therapy. This proprietary name is subject to review by the U.S. Food and Drug Administration, or FDA, in connection with our future anticipated regulatory submission for approval.

Geert Kersten has served in his current leadership role at CEL-SCI since 1995. Mr. Kersten has been with CEL-SCI from the early days of its inception since 1987. He has been involved in the pioneering field of cancer immunotherapy for almost two decades and has successfully steered CEL-SCI through many challenging cycles in the biotechnology industry. Mr. Kersten also provides CEL-SCI with significant expertise in finance and law and has a unique vision of how the company’s Multikine® product will change the way cancer is treated. Before CEL-SCI, Mr. Kersten worked at the law firm of Finley & Kumble and worked at Source Capital, an investment banking firm located in McLean, VA.

Opinion: On July 7th the Company took the unusual step in sending out a letter to address what it calls some of the confusion regarding the Phase 3 study results that were released last week. Adam Feuerstein of Stat wrote that the drug didn’t work and that the company was data mining results. Apparently, the market agreed with his analysis. Cel-Sci stock plunged from $27.33 to $8.89, losing 70% of its value by the close of the week.

Now it gets interesting. The CEO, putting his money where his mouth is, buys $200,000 worth of stock at $8 on 7-6. Two other directors buy a paltry $10,000 each at $8. That was enough to stem the slide and the shorts. My own opinion is that it will take a lot more than $10,000 buys to restore confidence.

Follow us on Twitter for real-time insider buying alerts at https://twitter.com/theinsidersfund.

[custom-twitter-feeds]

Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried many vendors, and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial, so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization, and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years, and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 are horrendously poor. Also, planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001, when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or me. In short, you can lose money following them. We have, and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019, 4th Best in November 2020, 4th Best in January 2021 (I kid you not)