The insider buying spigot opened a bit wider this week, but don’t mistake activity for conviction. Yes, we saw some heavyweight swings—Jared Isaacman dropping $16.3 million on Shift4 Payments and Amrize’s freshly-minted CEO Jan Jenisch betting $23.3 million on his construction materials spinoff. These aren’t lunch money purchases.

But here’s what gnaws at me: in a world hypnotized by AI’s insatiable appetite for data centers and energy infrastructure, are we witnessing genuine bottom-fishing or just executives with more money than sense? Eli Lilly’s triumvirate of buyers—Ricks, Fyrwald, and Skovronsky—collectively dropped $2.7 million around $640 per share. That’s either supreme confidence in their obesity/diabetes pipeline or spectacular timing dysfunction.

The breadth tells a story too. From Akamai’s CEO Leighton ($3.6M) to various healthcare plays, we’re seeing scattered buying across sectors that Wall Street has left for dead while chasing the next AI darling. Black Stone Minerals, PENN Entertainment, Sonos—these aren’t exactly the sexy names gracing CNBC’s mad money segments.

What’s missing? The tsunami. Every meaningful market bottom since 2001 has been preceded by a deluge of insider buying that makes this week look like a light drizzle. We’re seeing $50 million in notable purchases when historically we need $500 million to signal genuine capitulation.

The irony is palpable: while everyone debates whether NVIDIA is worth $3 trillion, actual business operators are quietly backing up the truck on their own unloved shares. Maybe they know something about intrinsic value that momentum chasers have forgotten.

Still waiting for the real flood. This week’s activity suggests the smart money is stirring, but we’re nowhere near the insider buying euphoria that typically marks generational bottoms. Patience remains the play.

Listen to the podcast here

Name: Hadi Partovi

Position: Director

Transaction Date: 08-13-2025 Shares Bought: 1,358 shares an Average Price Paid of $740.00 for Cost: $1,004,920

Company: Axon Enterprise Inc. (AXON):

Axon Enterprise, Inc., headquartered in Scottsdale, Arizona, develops and markets conducted energy devices under the TASER brand, along with cloud-based software and hardware solutions for law enforcement and public safety organizations worldwide. Its offerings include body and in-car cameras, digital evidence management platforms, records management systems, advanced analytics, and related accessories, training, and warranties. Products are distributed through direct sales, online platforms, partners, and resellers. Founded in 1993 as TASER International, Inc., the company rebranded as Axon Enterprise, Inc. in 2017.

Hadi Partovi has served as an Independent Director of Axon Enterprise Inc. since around 2010. He is the Co-Founder and CEO of Code.org, a nonprofit advancing computer science education, and an early investor and advisor to leading technology companies including Facebook, Dropbox, Uber, Airbnb, SpaceX, and Zappos. Previously, he held senior leadership roles at MySpace, iLike, Microsoft MSN, Tellme Networks, and Microsoft Internet Explorer. Partovi earned both his B.A. and M.S. in Computer Science, summa cum laude, from Harvard University.

Hedge Fund Insomniac’s Opinion: Axon’s value proposition is compelling, built on a powerful, integrated ecosystem that fosters a durable competitive moat. The company’s strategic shift to a high-margin, recurring-revenue model has fundamentally de-risked its financial profile, providing a stable and predictable revenue stream backed by a massive $10.7 billion backlog. However, this analysis reveals a significant and persistent discrepancy between the company’s current market valuation and its DCF-derived intrinsic value. The market’s valuation appears to be excessively optimistic, pricing in a flawless execution of ambitious growth initiatives in AI and drone technology and anticipating a long-term growth trajectory that exceeds traditional, conservative assumptions. While the company is an undeniable market leader with a robust business model, its current valuation does not offer a sufficient margin of safety for a value-oriented investor. The stock is a growth story with a premium valuation that is highly dependent on the flawless execution of future initiatives, a risk that investors must be willing to accept.

Name: Montarce Lucas

Position: EVP & CFO

Transaction Date: 08-15-2025 Shares Bought: 715 shares an Average Price Paid of $691.79 for Cost: $494,627

Name: Naarden Jacob Van

Position: EVP & Pres., Lilly Oncology

Transaction Date: 08-13-2025 Shares Bought: 1,000 shares an Average Price Paid of $647.36 for Cost: $647,360

Name: David A. Ricks

Position: President, Chairman, and CEO

Transaction Date: 08-12-2025 Shares Bought: 1,632 shares an Average Price Paid of $644.77 for Cost: $1,052,263

Name: J. Erik Fyrwald

Position: Director

Transaction Date: 08-12-2025 Shares Bought: 1,565 shares an Average Price Paid of $642.33 for Cost: $1,005,242

Name: Daniel Skovronsky

Position: EVP, CSO & President, LRL & LLY Imm

Transaction Date: 08-12-2025 Shares Bought: 1,000 shares an Average Price Paid of $634.40 for Cost: $634,405

Company: Eli Lilly & Co. (LLY):

Eli Lilly and Company, founded in 1876 and headquartered in Indianapolis, Indiana, is a global pharmaceutical leader that discovers, develops, and markets medicines across diabetes, oncology, immunology, and neuroscience. Its portfolio includes diabetes treatments like Basaglar, Humalog, Humulin, Jardiance, Mounjaro, Trulicity, and Zepbound for obesity; oncology therapies such as Alimta, Cyramza, Erbitux, Jaypirca, Retevmo, Tyvyt, and Verzenio; and immunology and neuroscience products including Olumiant, Taltz, Omvoh, Cymbalta, Ebglyss, and Emgality. The company collaborates with partners such as Incyte, Boehringer Ingelheim, Roche/Genentech, AbCellera, Verge Genomics, AdvanCell, and Chugai Pharmaceutical to advance treatments in oncology, autoimmune diseases, and other critical health areas.

Lucas Montarce is Executive Vice President and Chief Financial Officer at Eli Lilly and Company, where he has served since 2001. Over more than two decades with Lilly, he has held global leadership roles including President and General Manager for the Spain-Portugal-Greece region, Group Vice President and Corporate Controller & CFO of Lilly Research Laboratories, and Senior Vice President and CFO of Lilly International and Elanco Health. Originally from Buenos Aires, Argentina, Mr. Montarce earned a bachelor’s degree in business accounting from the Catholic University of Argentina and an MBA from the Center for Macroeconomic Studies of Argentina.

Jacob Van Naarden is Executive Vice President and President of Lilly Oncology at Eli Lilly and Company, a role he has held since 2019. He joined Lilly following its acquisition of Loxo Oncology, where he had been Chief Operating Officer, and played a key role in integrating and advancing Lilly’s oncology research and development programs. Earlier in his career, he worked in biotechnology investment, operations, and consulting at HealthCor Management, Aisling Capital, and Goldman Sachs. Mr. Van Naarden holds an A.B. in Molecular Biology from Princeton University.

David A. Ricks has served as President and CEO of Eli Lilly and Company since January 2017 and was elected Chairman of the Board in June 2017. Joining Lilly in 1996 as a business development associate, he advanced through roles in U.S. marketing, sales, and international operations, including General Manager positions in Canada and China, President of Lilly USA, and President of the Bio-Medicines division. Ricks earned his Bachelor of Science from Purdue University in 1990 and his MBA from Indiana University in 1996.

J. Erik Fyrwald has served on Eli Lilly & Co.’s Board of Directors since 2005, contributing extensive leadership expertise from his roles as CEO of Syngenta and currently CEO of International Flavors & Fragrances. A seasoned executive with a strong strategic and operational background, he holds a Bachelor of Science in Chemical Engineering from the University of Delaware (1981) and completed the Advanced Management Program at Harvard Business School.

Daniel M. Skovronsky, M.D., Ph.D., has served as Executive Vice President, Chief Scientific Officer, and President of Lilly Research Laboratories and Lilly Immunology since 2021, following a progression of leadership roles at Eli Lilly & Co. since its 2010 acquisition of Avid Radiopharmaceuticals, the company he founded. Previously Chief Medical Officer, Senior Vice President of Clinical and Product Development, and Vice President of Diabetes Research and Tailored Therapeutics, he has driven major R&D and business development initiatives across multiple therapeutic areas. He holds a B.S. in Molecular Biophysics and Biochemistry from Yale University and both an M.D. and Ph.D. in Neuroscience from the University of Pennsylvania.

Hedge Fund Insomniac’s Opinion:

Eli Lilly and Company (LLY) has recently experienced a significant stock price plunge, dropping more than 15% in a single day, which analysts attribute to disappointing clinical trial data for its oral weight-loss pill, orforglipron. While the drug met its primary endpoints, the average weight loss and a relatively high patient discontinuation rate fell short of the high expectations set by Wall Street, who were comparing it to the company’s highly successful injectable drugs, Mounjaro and Zepbound. Despite this negative news, the company posted a strong second quarter of 2025, beating revenue and earnings expectations, and raising its full-year guidance. This divergence between strong current performance and market disappointment in future pipeline potential caused the stock’s sharp decline. However, in the days following the plunge, several top executives, including CEO David Ricks, made a series of significant open-market purchases of company stock, a move widely interpreted as a strong vote of confidence that the stock is undervalued and the market has overreacted to the orforglipron data.

Name: Katrina L. Helmkamp

Position: Director

Transaction Date: 08-07-2025 Shares Bought: 2,500 shares an Average Price Paid of $159.61 for Cost: $399,026

Company: IDEX Corp. (IEX):

IDEX Corporation, founded in 1987 and headquartered in Northbrook, Illinois, provides applied solutions globally through three segments: Fluid & Metering Technologies, which produces pumps, valves, flow meters, and other fluid-handling equipment for industries such as water, energy, chemicals, agriculture, semiconductors, food, and pharmaceuticals; Health & Science Technologies, which offers precision fluidics, processing technologies, sealing solutions, medical devices, optical components, ceramics, and photonic solutions for life sciences, semiconductors, automotive, aerospace/defense, and medical/dental sectors; and Fire & Safety/Diversified Products, which supplies firefighting pumps, rescue tools, banding devices, lifting bags, and precision dispensing and mixing equipment for fire suppression, paint, automotive, aerospace/defense, and energy industries.

Katrina L. Helmkamp has served as an Independent Non-Executive Director of IDEX Corporation since November 2015 and became Non-Executive Chair of the Board in October 2022. She brings extensive leadership experience from her roles at major companies including Cartus, Lenox Corporation, SVP Worldwide, Whirlpool, and The Boston Consulting Group, and holds a Bachelor of Science in Industrial Engineering and an MBA from Northwestern University.

Hedge Fund Insomniac’s Opinion:

IDEX Corporation’s investment merits are based on its diversified portfolio of mission-critical engineered products, which provides a strong competitive moat. While revenue growth has been inconsistent, a 5-year average annual growth rate of 5.55% shows a healthy long-term trend. The company does not detail its recurring revenue percentage, but it has a history of strong growth in this area. Recent profitability metrics show a net margin of 14.05%, and its profitability is competitive within its industry. A recent insider purchase of 2,500 shares by a director could be a sign of confidence in the company’s future despite a recent stock price drop. The short interest is low, at 2.88% of the float. A DCF analysis by a third party suggests the stock is undervalued.

SWOT Analysis:

- Strengths: Diversified business, strong market position in niche areas.

- Weaknesses: Declining returns on equity and assets, recent negative earnings growth.

- Opportunities: Strategic acquisitions and capitalizing on new technologies.

- Threats: Economic downturns and intense competition.

Customer concentration is not a major issue as revenue is diversified across multiple end-markets and geographic regions.

Name: William R. Jellison

Position: Director

Transaction Date: 08-11-2025 Shares Bought: 3,000 shares an Average Price Paid of $145.98 for Cost: $437,940

Company: Masimo Corp (MASI):

Masimo Corporation, founded in 1989 and headquartered in Irvine, California, develops and delivers patient monitoring technologies, automation systems, and connectivity solutions worldwide. Its offerings include Masimo Signal Extraction Technology pulse oximetry for accurate readings in motion and low perfusion, the rainbow SET platform for noninvasive multi-parameter blood monitoring, and additional solutions such as acoustic respiration monitoring, NomoLine capnography, gas and regional oximetry, brain function and hemodynamic monitoring, and neuromodulation. The Masimo Hospital Automation platform features applications like Patient SafetyNet, Replica, and MyView, while its portfolio also includes nasal high-flow respiratory support, telehealth tools, and home wellness devices. Masimo serves healthcare providers, veterinarians, and consumers through direct sales, distributors, and OEM partnerships.

William R. Jellison has served as an Independent Director at Masimo Corporation since September 2024, bringing extensive management expertise from his tenure as Chief Financial Officer at Stryker Corporation and senior financial roles at Dentsply and Donnelly. Recognized for his proficiency in med-tech financing, corporate governance, and M&A strategy, he also chairs Masimo’s Audit Committee. Jellison holds a bachelor’s degree in business administration from Hope College.

Hedge Fund Insomniac’s Opinion:

Masimo (MASI) is a medical technology firm with a strong competitive moat derived from its patented Signal Extraction Technology (SET), which provides superior pulse oximetry readings. The company’s business model is characterized by a high-margin, recurring revenue stream from disposable sensors tied to its large installed base of monitoring devices. Over the past five years, Masimo has achieved a 16.7% revenue CAGR, but its profitability and share price have been impacted by the financial drain of its now-divested consumer electronics segment and high-profile litigation, particularly its patent dispute with Apple. The company is currently undergoing a significant strategic pivot under new management, refocusing on its core healthcare business. The stock has a high short interest of 46.75%, indicating considerable bearish sentiment. A DCF valuation, based on a 7.2% discount rate, suggests a fair value of around $136 per share, making the stock’s valuation sensitive to future growth projections and the resolution of its legal and operational challenges.

Name: Gregory Hayes

Position: Director

Transaction Date: 08-14-2025 Shares Bought: 8,350 shares an Average Price Paid of $119.90 for Cost: $1,001,165

Company: Phillips 66 (PSX):

Phillips 66 is a diversified energy manufacturing and logistics company with global operations, including in the U.S., U.K., and Germany. Its five business segments are Midstream, Chemicals, Refining, Marketing & Specialties, and Renewable Fuels. The company transports crude oil and refined products, processes natural gas and NGLs, manufactures petrochemicals and specialty chemicals, and refines crude into fuels such as gasoline, distillates, and jet fuel. Its M&S division markets petroleum products, lubricants, and base oils, while the Renewable Fuels segment converts feedstocks into renewable diesel, jet fuel, and other low-carbon fuels. Founded in 1875, Phillips 66 is headquartered in Houston, Texas.

Gregory J. Hayes has served as an independent director on the Board of Phillips 66 since July 2022. He chairs the Nominating and Governance Committee and is a member of the Human Resources & Compensation, Public Policy & Sustainability, and Executive Committees. A certified public accountant, Mr. Hayes holds a bachelor’s degree in economics from Purdue University.

Hedge Fund Insomniac’s Opinion:

Phillips 66 (PSX) is an energy manufacturing and logistics company with a diversified business in refining, midstream, chemicals, and marketing. Its competitive advantage lies in its extensive midstream infrastructure, which provides stable, fee-based revenue. The company’s 5-year revenue growth rate has been around 13.9%, though revenue has recently declined. It lacks a significant recurring revenue stream. A recent DCF analysis suggests the stock may be undervalued, with a target price around $171.70. Management is focused on expanding stable segments like midstream. Recent news includes strategic acquisitions to bolster its midstream business, while short interest remains low at 1.97%. The company has a diversified customer base, primarily in the U.S

Name: Vivek Jain

Position: Chairman and CEO

Transaction Date: 08-14-2025 Shares Bought: 21,929 shares an Average Price Paid of $112.84 for Cost: $2,474,375

Company: ICU Medical Inc. (ICUI):

ICU Medical, Inc., founded in 1984 and headquartered in San Clemente, California, designs, manufactures, and markets medical devices for infusion therapy, vascular access, and critical care worldwide. Its product portfolio includes needle-free connectors, catheter patency devices, closed system transfer devices, non-coring needles, disinfection caps, infusion pumps, irrigation solutions, ambulatory and syringe infusion systems, and drug infusion safety software. The company also provides hemodynamic monitoring equipment, anesthetic and respiratory systems, temperature management solutions, and related professional services. ICU Medical serves acute care hospitals, wholesalers, ambulatory clinics, home healthcare providers, and nursing homes globally.

Vivek Jain has served as Chairman of the Board and Chief Executive Officer of ICU Medical, Inc. since February 2014. He previously led CareFusion Corporation’s Procedural Solutions division as President and held senior roles in strategy and corporate development at Cardinal Health, along with executive positions at Philips and JPMorgan. Mr. Jain holds a Bachelor of Arts degree in Economics from the University of Chicago.

Hedge Fund Insomniac’s Opinion:

ICU Medical, a medical device company, has expanded its business through acquisitions, resulting in a 5-year revenue CAGR of approximately 17.5%, from $1.27 billion in 2020 to $2.38 billion in 2024. However, it faces profitability challenges with a recent negative net profit margin of -3.87%, in contrast to some competitors like Align Technology (ALGN) which has a positive 11.04% margin. A key competitive moat is its integrated product portfolio, creating high switching costs for hospitals. Recent stock price movements were influenced by a Q2 2025 earnings beat, while the company continues to manage regulatory scrutiny. Short interest is a variable metric, recently reported at 5.29%. The company’s customer base is concentrated on acute care hospitals, a key risk to monitor.

Name: Jared Isaacman

Position: Executive Chairman, 10% Owner

Transaction Date: 08-08-2025 Shares Bought: 196,426 shares an Average Price Paid of $82.81 for Cost: $16,266,182

Company: Shift4 Payments Inc. (FOUR):

Shift4 Payments Inc. is a leading U.S.-based independent software and payment processing solutions provider, ranked by total payment volume processed. Serving hundreds of thousands of businesses across nearly every industry—from small owner-operated firms to global multinationals—the company processes billions of transactions annually. Its solutions simplify commerce management across multiple channels, regions, and systems through seamless integration of software and hardware tools, enhancing operational efficiency, payment acceptance, and customer experience.

Jared Isaacman, Executive Chairman and Director of Shift4 Payments Inc., owns approximately 10% of the company and has led it since founding it as United Bank Card in 1999. He guided the company through its IPO in 2020 and has remained in leadership from inception. Isaacman holds a Bachelor of Science in Professional Aeronautics from Embry-Riddle Aeronautical University’s Worldwide Campus, earned in 2011.

Hedge Fund Insomniac’s Opinion:

Shift4 Payments is a high-growth payment processor with a robust 24.3% revenue CAGR over the past five years, reaching $3.33 billion in 2024. The company’s strength lies in its integrated platform and specialization in the hospitality and entertainment sectors, creating a strong competitive moat with high switching costs. A notable portion of its business is recurring, with subscription revenue increasing by 90% in 2024. While recent profitability has been mixed, its non-GAAP P/E ratio of 16.45 suggests it may be undervalued compared to peers. Recent news, including a Q2 2025 earnings beat, has positively impacted the stock. However, a significant short interest of 20.53% indicates a high level of bearish sentiment. The company’s customer base is highly diversified, with no single customer accounting for more than 3% of its volume.

Name: Timothy Throsby

Position: Director

Transaction Date: 08-14-2025 Shares Bought: 20,000 shares an Average Price Paid of $89.37 for Cost: $1,787,311

Name: Antonia Korsanos

Position: Director

Transaction Date: 08-10-2025 Shares Bought: 8,065 shares an Average Price Paid of $80.05 for Cost: $645,603

Name: Jamie Odell

Position: Director

Transaction Date: 08-07-2025 Shares Bought: 8,275 shares an Average Price Paid of $78.81 for Cost: $652,154

Company: Light & Wonder Inc. (LNW):

L&W, headquartered in Las Vegas, Nevada, is a leading global cross-platform gaming company specializing in content and digital markets. Its portfolio spans supplying game content, gaming machines, casino management systems, and table game products and services to licensed gaming operators; offering social casino, casual, and other online games directly to consumers; and delivering a full range of digital gaming content, distribution platforms, player account management systems, and other iGaming solutions. The company operates through three segments—Gaming, SciPlay, and iGaming—reflecting its diverse offerings.

Timothy Throsby has been a member of Light & Wonder Inc.’s Board of Directors since 2020. He brings extensive global financial leadership experience, having served as CEO of Barclays Bank plc and President of Barclays International, where he led a major transformation of the business. He previously held senior roles including Global Head of Equities at JPMorgan, President of Citadel Asia in Hong Kong, and executive positions at Goldman Sachs, Lehman Brothers, Credit Suisse, and Macquarie Bank. Mr. Throsby holds a Bachelor of Economics from the University of Sydney, a Jurisprudence degree from the University of Oxford, and completed the Advanced Management Program at Harvard Business School.

Antonia Korsanos joined Light & Wonder in 2020 as Vice Chair of the Board, after serving as a senior advisor since mid-2019, and became Chair in August 2022. She brings extensive expertise in finance, technology, strategy, M&A, risk management, and regulatory compliance, honed during her tenure as CFO and Company Secretary at Aristocrat Leisure. Ms. Korsanos holds a Bachelor of Economics in Accounting and Finance from Macquarie University.

Jamie R. Odell has served as Chair of the Board since 2020, continuing from Scientific Games through its transition to Light & Wonder, after joining as a senior advisor in May 2019. With over 30 years of global leadership experience in consumer products, technology, and gaming, he previously served as CEO and Managing Director of Aristocrat Technologies from 2009 to 2017, driving major global transformation. Earlier, he held senior executive and managing director roles at Foster’s Group, Beringer, and Allied Lyons across the U.S., Europe, Asia, and Australia.

Hedge Fund Insomniac’s Opinion:

Light & Wonder Inc. (LNW) is a global gaming company operating in three main segments: Gaming, iGaming, and SciPlay. LNW’s moat comes from its strong brand, diverse product portfolio, and significant global licensing agreements, which create high barriers to entry. The company has demonstrated positive revenue growth, with a recent year-over-year increase of 9.86%. A key component of its business is recurring revenue. Its stock price can be volatile, as seen with recent mixed earnings reports. Recent short interest is approximately 4.12 million shares, with a short ratio of 3.99. Strengths of the company include its market position and diversified revenue streams, balanced by weaknesses such as historical debt levels. Opportunities lie in the expanding iGaming market, while threats include intense competition and regulatory changes. LNW’s customer base is global and diversified, but large casino operators likely account for a significant portion of its revenue.

Name: Daniel Hesse

Position: Director

Transaction Date: 08-11-2025 Shares Bought: 3,000 shares an Average Price Paid of $72.30 for Cost: $216,89

Name: F. Thomson Leighton

Position: Chief Executive Officer

Transaction Date: 08-11-2025 Shares Bought: 50,000 shares an Average Price Paid of $72.26 for Cost: $3,613,047

Company: Akamai Technologies Inc (AKAM):

Akamai Technologies, Inc., founded in 1998 and headquartered in Cambridge, Massachusetts, delivers security, content delivery, and cloud computing solutions worldwide. Its offerings include web application and API protection, bot and abuse prevention, account and content security, API and microservice traffic protection, as well as cloud computing services such as compute, storage, networking, databases, and scalable Kubernetes deployments via the Akamai App Platform. The company also provides web and mobile performance optimization, global traffic management, application load balancing, media streaming, software distribution, broadcast operations, DNS services, and data analytics.

Daniel R. Hesse has been a member of Akamai’s Board of Directors since August 2016, bringing extensive leadership experience in telecommunications and internet services. He previously served as President and CEO of Sprint Corporation, Chairman and CEO of both Embarq and Terabeam, and held key executive roles at AT&T, where he was instrumental in launching services like AT&T WorldNet and leading AT&T Wireless. Hesse holds a Bachelor of Arts from the University of Notre Dame, an MBA from Cornell University’s Johnson Graduate School of Management, and a Master of Science from the MIT Sloan School of Management.

F. Thomson Leighton, co-founder of Akamai Technologies in 1998, served as Chief Scientist before becoming CEO in 2013, guiding the company’s transformation from a content delivery pioneer to a comprehensive cybersecurity and cloud services provider. He holds a Bachelor of Science in Electrical Engineering and Computer Science from Princeton University and a Ph.D. in Applied Mathematics from MIT.

Hedge Fund Insomniac’s Opinion:

Akamai Technologies, a leader in cloud computing and content delivery, is a mature company with steady revenue growth. Its 5-year revenue CAGR is a modest 4.7%, growing to nearly $4 billion in 2024, as it shifts from its core CDN business to higher-growth security and cloud infrastructure. A key strength is its massive global network, which creates high switching costs and a strong competitive moat. While recent net income has been pressured by strategic investments, its non-GAAP operating margin remains strong at 30%. The stock has been buoyed by a Q2 2025 earnings beat, driven by strong growth in its security and cloud segments. Short interest is moderate, at approximately 8.8 million shares. The company has a well-diversified customer base with no single customer accounting for more than 10% of revenue.

Name: William K. Daniel

Position: Director

Transaction Date: 08-07-2025 Shares Bought: 10,000 shares an Average Price Paid of $67.08 for Cost: $670,800

Company: Henry Schein Inc. (HSIC):

Henry Schein, Inc., founded in 1932 and headquartered in Melville, New York, provides health care products and services to dental and medical practitioners worldwide, as well as alternative care settings. The company operates through three segments: Global Distribution and Value-Added Services, Global Specialty Products, and Global Technology. Its offerings include a wide range of dental merchandise—such as infection-control products, handpieces, preventatives, impression materials, composites, anesthetics, teeth, dental implants, gypsum, acrylics, articulators, abrasives, and PPE—as well as dental equipment, including chairs, delivery units, lights, digital dental labs, X-ray systems, and high-tech restoration tools, along with repair services. In addition, the company supplies branded and generic pharmaceuticals.

William K. Daniel joined Henry Schein Inc.’s Board of Directors as an independent director in May 2025, following a strategic investment collaboration with KKR. He is an Executive Advisor to KKR and previously worked as Executive Vice President at Danaher Corporation, where he led multiple industrial and life sciences business areas. Mr. Daniel has an undergraduate degree in economics from DePauw University and an MBA from the University of Virginia’s Darden School of Business.

Hedge Fund Insomniac’s Opinion:

Henry Schein is a leading distributor in the dental and medical industries, with a strong competitive moat based on its scale and integrated services. The company has a moderate 5-year revenue CAGR of approximately 8.5% and a stable business model, with roughly two-thirds of its revenue being recurring. Despite a healthy return on equity of 14.36%, its profitability has faced pressures, with a net profit margin of 3.05% trailing some competitors. Recent stock volatility was triggered by a significant cybersecurity incident and a miss on Q2 2025 EPS, which impacted sales by 12%. Short interest is notably high at approximately 7.57%, reflecting bearish sentiment. The company’s broad, diversified customer base of over 1 million practitioners is a key strength.

Name: David J. Henshall

Position: Director

Transaction Date: 08-08-2025 Shares Bought: 10,000 shares an Average Price Paid of $48.60 for Cost: $486,000

Company: Blackline Inc. (BL):

BlackLine, Inc., founded in 2001 and headquartered in Woodland Hills, California, provides cloud-based solutions that automate and streamline accounting and finance operations worldwide. Its offerings include financial close and consolidation tools—such as account reconciliations for centralized collaboration, transaction matching for data validation, journal entry automation, variance analysis for identifying unusual account fluctuations, compliance management for control assessments, and Smart Close for SAP—helping organizations improve efficiency, accuracy, and transparency in financial processes.

David J. Henshall has served on BlackLine Inc.’s Board of Directors since September 2024. He is the former President and CEO of Citrix Systems, where he also held leadership roles including COO and CFO, guiding the company through its cloud transformation and operational restructuring. Henshall holds a Bachelor of Science in Business Administration from the University of Arizona and an MBA from Santa Clara University.

Hedge Fund Insomniac’s Opinion:

BlackLine is a cloud-based software company specializing in accounting automation. Its business model is highly predictable, with roughly 94% of revenue being recurring subscriptions. The company’s competitive moat is built on high switching costs and a unified platform. BlackLine has a moderate 5-year revenue CAGR of 16.8%, reaching $653.3 million in 2024, but its growth has been decelerating. A key strength is its 105% dollar-based net revenue retention rate, indicating customer expansion. While GAAP profitability is inconsistent, its non-GAAP operating margin is a healthy 22.1%. The stock has seen positive movement following a Q2 2025 earnings beat, but a notable short interest of approximately 6.9 million shares remains. The company’s customer base is well-diversified, with no significant concentration risk.

Name: Ian A. Johnston

Position: Chief Financial Officer

Transaction Date: 08-08-2025 Shares Bought: 10,500 shares an Average Price Paid of $47.71 for Cost: $500,987

Name: Denise R. Singleton

Position: Chief Legal Officer & Corp Sec

Transaction Date: 08-08-2025 Shares Bought: 4,000 shares an Average Price Paid of $47.64 for Cost: $190,560

Name: Jan Philipp Jenisch

Position: Chairman & CEO

Transaction Date: 08-08-2025 Shares Bought: 500,000 shares an Average Price Paid of $46.56 for Cost: $23,279,383

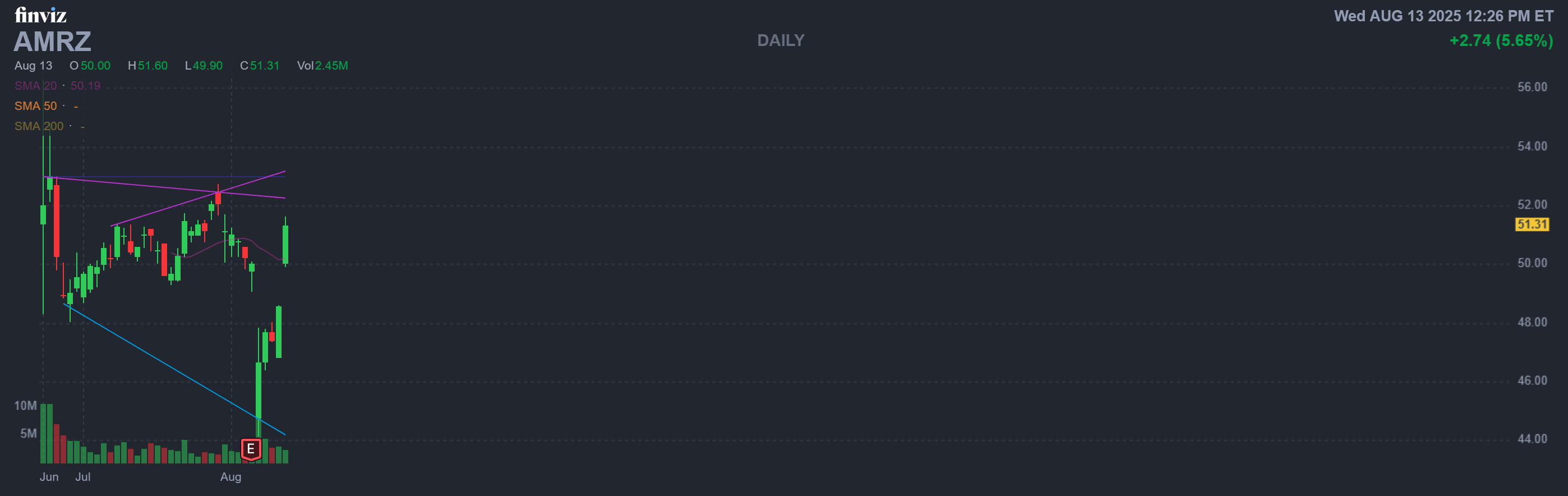

Company: Amrize Ltd (AMRZ):

Amrize Ltd. is a publicly traded construction solutions company serving the North American market, formed from a mid-2025 spin-off of Holcim. It offers a comprehensive portfolio of advanced construction materials, including cement, aggregates, ready-mix concrete, asphalt, and building envelope products such as roofing systems, insulation, shingles, waterproofing, adhesives, and sealants, designed for both residential and commercial applications.

Ian A. Johnston has served as CEO of Amrize Ltd. since 1998, leveraging decades of leadership and financial expertise. Over his tenure, he has held several key roles, including CFO for multiple regional divisions, before advancing to lead the company. He holds a Bachelor of Commerce in Accounting from the University of Ottawa and became a Chartered Professional Accountant in 1999.

Denise R. Singleton has been Chief Legal Officer and Corporate Secretary of Amrize Ltd. since September 2024, bringing extensive legal and corporate governance expertise from senior roles at WestRock Company, IDEX Corporation, and SunCoke Energy. She holds a Juris Doctor from Georgetown University Law Center and a Bachelor of Arts in Journalism from Marquette University.

Jan Philipp Jenisch has been Chairman and CEO of Amrize since its spin-off and public listing in mid-2025, having previously joined as Chairman of the Parent Board in 2023. He formerly served as CEO of Holcim from 2017 to April 2024 and as Chairman from 2023 to 2025, following his tenure as CEO of Sika AG from 2012 to 2017. Renowned for restructuring global construction materials companies and driving strategic growth, he holds an MBA from the University of Fribourg and received an honorary doctorate in 2021 for his leadership achievements.

Hedge Fund Insomniac’s Opinion:

Amrize Ltd. (AMRZ), a building solutions company, was spun off from Holcim in June 2025. With a recent twelve-month revenue of $11.619 billion and a net income margin of 13.3%, it has a respectable start as a new publicly traded company. The competitive moat is based on its established market position and a diversified product portfolio. However, due to its recent public debut, a five-year revenue growth rate is not available. The stock has experienced volatility, with recent news including a price target reduction by RBC Capital to $54 from $61, despite a report of solid Q2 results. The short interest is approximately 8.8 million shares, and its customer base is broad.

Name: J. Kevin Willis

Position: Chief Financial Officer

Transaction Date: 08-14-2025 Shares Bought: 12,725 shares an Average Price Paid of $39.41 for Cost: $501,506

Company: Valvoline Inc. (VVV):

Valvoline Inc. is a leading provider of automotive preventive maintenance services with a strong retail presence across the United States and Canada. Known for being quick, easy, and trusted, the company focuses on growing its service network, enhancing customer convenience, and driving innovation to meet evolving vehicle care needs while building long-term shareholder value.

J. Kevin Willis was appointed Chief Financial Officer of Valvoline Inc. in May 2025, following a distinguished career at Ashland Inc., where he served as Senior Vice President and CFO from 2013 to 2025 and played a pivotal role in Valvoline’s successful 2016 IPO. With deep expertise in finance, operations, and corporate strategy, Willis has been recognized as a trusted industry leader. He holds a BBA in Accounting from Eastern Kentucky University and an MBA from Northwestern University’s Kellogg School of Management.

Hedge Fund Insomniac’s Opinion:

Valvoline Inc. (VVV) has successfully transitioned into a services-focused company, leveraging its strong brand and network of over 2,000 service centers. The business model is highly recurring, fostering strong customer loyalty. While the company’s overall revenue growth has been negative due to a major divestiture, its core services business is growing, with a recent 4.2% year-over-year increase. The company’s profitability is healthy, with a Q1 2025 net margin of 9.33%, although net income decreased by 9.18% year-over-year. The stock has been positively influenced by recent earnings beats, but short interest remains high at 10.17 million shares, or 8% of the float, reflecting a significant bearish sentiment. The customer base is highly diversified.

Name: Theodore R. Samuels II

Position: Director

Transaction Date: 07-28-2025 Shares Bought: 9,000 shares an Average Price Paid of $27.62 for Cost: $248,580

Name: Sarah London

Position: Chief Executive Officer

Transaction Date: 08-08-2025 Shares Bought: 19,230 shares an Average Price Paid of $25.50 for Cost: $490,365

Company: Centene Corp (CNC):

Centene Corporation is a U.S.-based healthcare company that delivers programs and services to underinsured and uninsured individuals, businesses, and military families through four segments: Medicaid, Medicare, Commercial, and Other. Its Medicaid segment offers coverage for the elderly, blind, and disabled, along with CHIP, foster care, Medicaid plans, long-term services, and other healthcare products. The Medicare segment provides special needs plans, Medicare supplements, and prescription drug coverage, while the Commercial segment offers health insurance marketplace solutions for individuals, and small and large groups.

Theodore R. Samuels II has served as a Director at Centene Corporation since January 2022, bringing over 35 years of financial industry experience, including roles as President of Capital Guardian Trust Company and Global Equity Portfolio Manager at Capital Group. He has significant governance expertise from board positions at Bristol-Myers Squibb and Perrigo and currently serves on Centene’s Compensation and Talent Committee and Governance Committee. Mr. Samuels holds a bachelor’s degree from Harvard University and an MBA from Harvard Business School.

Sarah M. London has served as CEO of Centene Corporation since March 2022, having joined the company in 2020 as Senior Vice President of Technology Innovation and Modernization before advancing to Vice Chair. Her prior experience includes serving as a partner at Optum Ventures and as Chief Product Officer at Optum Analytics. She earned her B.A., magna cum laude, in History & Literature from Harvard College, where she competed in Division I tennis, and later received her MBA with High Honors from the University of Chicago Booth School of Business.

Hedge Fund Insomniac’s Opinion:

Centene Corporation is a major managed care organization with a stable business model, where virtually all of its revenue is recurring. The company has a 5-year revenue CAGR of approximately 4.7%, with LTM revenue reaching $178.2 billion. Its competitive moat is based on its massive scale and expertise in government-sponsored programs. However, the company faces profitability challenges, with a net margin of only 1.15%, which is lower than competitors. The stock recently experienced significant pressure, dropping nearly 40% after the company withdrew its 2025 financial guidance due to higher-than-expected medical costs. Its current forward P/E ratio of 7.2 suggests a compelling valuation compared to the industry average.

Name: Min-Chu (Mike) Chen

Position: Director

Transaction Date: 08-13-2025 Shares Bought: 7,500 shares an Average Price Paid of $22.91 for Cost: $171,825

Name: Chih-Hsiang (Thompson) Lin

Position: President and CEO

Transaction Date: 08-12-2025 Shares Bought: 18,600 shares an Average Price Paid of $22.76 for Cost: $423,413

Name: William H. Yeh

Position: Director

Transaction Date: 08-13-2025 Shares Bought: 18,000 shares an Average Price Paid of $22.54 for Cost: $405,700

Company: Applied Optoelectronics Inc. (AAOI):

Applied Optoelectronics, Inc. is a leading vertically integrated provider of fiber-optic networking technologies serving the internet data center, cable television, telecommunications, and fiber-to-the-home markets. The company designs and manufactures optical communications solutions at multiple levels of integration, from core laser components and subassemblies to complete turnkey systems. Its product development process begins with advanced laser technology and expands into a broad portfolio of solutions tailored to specific markets, applications, and integration needs. AOI is focused on high-performance markets that demand faster connectivity and continuous innovation.

Dr. Min-Chu (Mike) Chen has served as a director of Applied Optoelectronics, Inc. since February 2013. He is Chair of the Nominating and Corporate Governance Committee and a member of the Audit Committee. Dr. Chen has been a partner and board member of EverRich Capital Inc., a financial consulting firm, since 2001, and in 2023 he co-founded KidTech, Inc., a company focused on personalized healthcare solutions for children. He has also held directorships at Iecont Technology Inc., Nanning Baota Biowin Technologies Co., Ltd., and Harbin Neotek Medical Devices Co., Ltd. Dr. Chen earned his Ph.D. in Ocean Engineering from Oregon State University.

Dr. Chih-Hsiang (Thompson) Lin founded Applied Optoelectronics, Inc. in February 1997 and has served as its President and Chief Executive Officer since inception. He has also held the role of Chairman of the Board at various times, most recently in January 2014. Prior to founding AOI, Dr. Lin was a senior research scientist at the University of Houston from 1994 to 1998 and later a research associate professor from 1998 to 2000. He holds a bachelor’s degree in Nuclear Engineering from National Tsing Hua University in Taiwan and earned both his M.S. and Ph.D. in Electrical and Computer Engineering from the University of Missouri-Columbia.

William H. Yeh has served as a director of Applied Optoelectronics, Inc. since May 2000. He has held several key leadership roles, including Chairman of the Compensation Committee, member of the Nominating & Corporate Governance Committee, and Lead Independent Director since April 2018. In these capacities, he has played a pivotal role in guiding the company’s senior leadership and strengthening its governance practices. With extensive experience in the technology sector and long-standing involvement with Applied Optoelectronics, Mr. Yeh has significantly contributed to the company’s strategic direction and growth. He holds a Bachelor of Science degree in Electrical Engineering from the University of California, Berkeley.

Hedge Fund Insomniac’s Opinion:

Applied Optoelectronics, Inc. (AAOI) is a provider of fiber-optic networking products with a non-recurring, project-based business model. This has led to an inconsistent 5-year revenue CAGR of 4.7%, although its recent Q2 2025 revenue more than doubled to $102.95 million. The company is not profitable on a GAAP basis, posting a net loss of $9.1 million in the same quarter. A key risk is the company’s reliance on a few large customers for a significant portion of its revenue. Short interest is notably high at nearly 20% of the float, or 11.83 million shares, reflecting significant bearish sentiment toward the company.

Name: David A. Handler

Position: Director

Transaction Date: 08-08-2025 Shares Bought: 20,000 shares an Average Price Paid of $16.96 for Cost: $339,300

Company: PENN Entertainment Inc. (PENN):

Penn Entertainment, Inc. is a leading North American provider of integrated entertainment, sports content, and casino gaming, operating across multiple jurisdictions with a diverse portfolio that includes casinos, racetracks, and online betting platforms such as Hollywood Gaming, L’Auberge, ESPN BET, and theScore BET. Leveraging strategic partnerships, including with ESPN, and its ownership of theScore, the company combines a strong IT infrastructure with an in-house content studio to deliver seamless digital betting experiences, while its PENN Play loyalty program enhances customer engagement through personalized rewards and experiences.

Mr. Handler has served as Board Chair of PENN Entertainment since June 2019 and as a director since 1994, bringing extensive experience in M&A and strategic advisory services. He co-founded Tidal Partners in August 2022, focusing on the technology industry, after founding and leading Centerview Partners’ Technology Advisory Practice from 2008 to 2022, and previously serving as Managing Director at UBS Investment Bank from 2006 to 2008.

Hedge Fund Insomniac’s Opinion:

PENN Entertainment, Inc. (PENN) operates a unique omnichannel strategy, integrating its vast network of over 40 retail casinos with its digital platforms like ESPN BET. The company’s recent Q2 2025 report showed strong performance, with revenue of $1.77 billion and a positive EPS of $0.10, beating analyst expectations. Despite this, PENN remains unprofitable on a GAAP basis, with a net loss of $18.3 million, and its interactive segment posted an Adjusted EBITDA loss of $62 million. Short interest is high at 19.44 million shares, representing 15.77% of the float, indicating strong bearish sentiment. The company has a 5-year revenue CAGR of 10.38% and continues to invest heavily in its digital business for future growth.

Name: Thomas L. Carter Jr.

Position: CEO, President, and Chairman

Transaction Date: 08-07-2025 Shares Bought: 72,210 shares an Average Price Paid of $12.18 for Cost: $879,347

Company: Black Stone Minerals L.P. (BSM):

Black Stone Minerals L.P. is a leading owner and manager of oil and natural gas mineral interests in the United States, with extensive holdings across multiple producing basins. The partnership primarily generates revenue by leasing its mineral properties to exploration and production companies and earning royalty payments from the resulting oil and gas production.

Thomas L. Carter Jr. has served as CEO and Chairman of the General Partner of Black Stone Minerals L.P. since November 2014, taking a break from the role of President between June 2018 and February 2023. He founded the company’s predecessor in 1998 and earlier established the first Black Stone Energy Company in 1980. Carter began his career as a loan officer in the Energy Department at Texas Commerce Bank from 1978 to 1980 and holds both B.B.A. and M.B.A. degrees from the University of Texas at Austin.

Hedge Fund Insomniac’s Opinion:

Black Stone Minerals L.P. (BSM) is an asset-light company that generates high-margin revenue from oil and gas royalties. While its 5-year cumulative revenue growth is -7.8%, recent performance has been strong, with Q2 2025 revenue increasing by 45.49% to $159.49 million. The company is highly profitable, with a net income of $120.0 million and a remarkable net margin of 75.26% in the last quarter. However, the company’s recent 20% distribution decrease in Q2 2025 caused stock volatility. Despite this, bearish sentiment is limited, with short interest at a low 1.65% of the float, and the company maintains a stable balance sheet with a low debt-to-equity ratio of 0.09

Name: Bracken Darrell

Position: Director

Transaction Date: 08-08-2025 Shares Bought: 22,412 shares an Average Price Paid of $11.15 for Cost: $250,000

Name: Thomas Conrad

Position: Chief Executive Officer

Transaction Date: 08-08-2025 Shares Bought: 92,300 shares an Average Price Paid of $11.10 for Cost: $1,024,299

Name: Julius Genachowski

Position: Director

Transaction Date: 08-08-2025 Shares Bought: 22,850 shares an Average Price Paid of $10.95 for Cost: $250,205

Name: Saori Casey

Position: Chief Financial Officer

Transaction Date: 08-08-2025 Shares Bought: 22,727 shares an Average Price Paid of $10.94 for Cost: $248,688

Company: Sonos Inc (SONO):

Sonos, Inc., founded in 2002 and headquartered in Santa Barbara, California, designs, develops, manufactures, and sells audio products and services across the Americas, Europe, the Middle East, Africa, and Asia Pacific. Formerly known as Rincon Audio, Inc. until May 2004, the company offers wireless, portable, and home theater speakers, headphones, components, and accessories, distributing its products through physical stores, websites, online retailers, and custom installers.

Bracken Darrell joined the Sonos Board of Directors on February 12, 2024, bringing extensive experience in consumer brand leadership. He previously served as President and CEO of Logitech International for over a decade, driving product innovation and category growth, and has also held senior roles at Procter & Gamble, Whirlpool, and General Electric. Darrell holds a Bachelor of Arts from Hendrix College and an MBA from Harvard Business School.

Tom Conrad, a member of Sonos’ Board of Directors since 2017, became interim CEO in January 2025 and was officially appointed CEO in July. He brings extensive consumer technology experience from senior roles at Pandora, Snap Inc., and Quibi, where he contributed to core user interface development. Conrad holds a Bachelor of Science in Computer Engineering from the University of Michigan.

Julius Genachowski has served on Sonos Inc.’s Board of Directors since September 2013 and became Chairperson in May 2023. He was Chairman of the U.S. Federal Communications Commission from 2009 to 2013 and previously held senior roles at IAC/InterActiveCorp and The Carlyle Group. Genachowski also sits on the boards of Mastercard and Mattel and formerly served on Sprint’s board. He holds a B.A. in History from Columbia University, a J.D. from Harvard Law School, and clerked for U.S. Supreme Court Justice David H. Souter.

Saori Casey became Chief Financial Officer of Sonos, Inc. on January 22, 2024, overseeing the company’s financial, accounting, real estate, technology, and investor relations functions. She previously spent nearly 13 years as Vice President of Finance at Apple and 15 years in finance leadership roles at Cisco Systems during its major growth phase. Casey holds a B.A. in Economics from the University of California, Santa Barbara, and an MBA from the Peter F. Drucker Graduate School of Management at Claremont Graduate University.

Hedge Fund Insomniac’s Opinion:

Sonos Inc. (SONO) is a consumer electronics company with a competitive moat built on its proprietary ecosystem and strong brand loyalty, which leads to a 62% repeat purchase rate. While the company has a healthy non-GAAP gross margin of 44.7%, it is not profitable on a GAAP basis, reporting a net loss of $76.4 million over the last twelve months. Its revenue growth has been inconsistent, with a 5-year CAGR of 1.95%. In Q3 2025, revenue was $344.8 million, a 13.2% year-over-year decline. Short interest is notable at 6.89% of the float, or 7.1 million shares, indicating some bearish sentiment. The customer base is highly diversified.

Name: Gary Blackford

Position: Director

Transaction Date: 08-13-2025 Shares Bought: 60,000 shares an Average Price Paid of $10.99 for Cost: $659,300

Company: Avanos Medical Inc. (AVNS):

Avanos Medical, Inc., headquartered in Alpharetta, Georgia, is a medical technology company focused on delivering innovative device solutions that improve patient outcomes and reduce healthcare costs. Its portfolio centers on Digestive Health and Pain Management, offering products that support nutrition from hospital to home and aid recovery while reducing opioid reliance. Founded in 2014 in Delaware, Avanos manufactures in the U.S. and Mexico and markets its leading brands globally.

Gary D. Blackford has served on the Board of Directors of Avanos Medical, Inc. since October 2014 and was appointed Chairman in April 2020. He brings extensive executive leadership experience, having previously been Chairman and CEO of Universal Hospital Services until early 2015, as well as CEO of Curative Health Services and ShopforSchool. In addition to his role at Avanos, he serves on the boards of ReShape Lifesciences, Children’s Hospitals and Clinics of Minnesota, and Lifespace Communities. Blackford was selected for Avanos’ board for his expertise in executive leadership, finance, international business, governance, and public company board service. He earned his undergraduate degree from the University of Iowa in 1979 and his graduate degree from Creighton University in 1982.

Hedge Fund Insomniac’s Opinion:

Avanos Medical is a medical device company with a limited competitive moat and an inconsistent financial profile. The company’s revenue has declined over the past five years, with a cumulative growth of -2.94%. While Q2 2025 revenue grew by 1.9% to $175.0 million, the company is not profitable on a GAAP basis, posting a net loss of $76.8 million. Despite beating analyst estimates, the stock dropped by 12.89% after the Q2 report, reflecting concerns over a declining gross margin of 55.7% and ongoing profitability issues. Short interest is low at 4.23%, indicating limited bearish sentiment.

Name: Stephen A. Kaplan

Position: Director

Transaction Date: 08-11-2025 Shares Bought: 46,509 shares an Average Price Paid of $6.77 for Cost: $314,866

Company: Townsquare Media Inc.(TSQ):

Townsquare is a community-focused digital and broadcast media company that delivers digital marketing solutions primarily outside the top 50 U.S. markets. Its digital advertising arm, Townsquare Ignite, leverages proprietary programmatic technology, an in-house demand and data management platform, and a network of 400+ local news and entertainment websites, apps, and national music brands to connect businesses with target audiences. Through Townsquare Interactive, the company offers subscription-based marketing services such as website design, hosting, SEO, and a SaaS management platform for small and medium-sized businesses. Additionally, its extensive network of local radio stations provides both advertising opportunities and relevant community-focused content.

Stephen A. Kaplan has been a director of Townsquare Media Inc. since 2010. He is the founder and chairman of Nalpak Capital and previously co-founded Oaktree Capital Group LLC, where he served as an Advisory Partner until 2019. Earlier in his career, he was a partner at Gibson, Dunn & Crutcher. Mr. Kaplan holds a B.S. in Political Science from SUNY Stony Brook and a J.D. from NYU School of Law.

Hedge Fund Insomniac’s Opinion:

Townsquare Media Inc. (TSQ) is a diversified media company successfully transitioning to a digital-first strategy. Its competitive moat is its unique omnichannel approach, leveraging its network of 349 radio stations to drive its digital business. While the company’s overall 5-year revenue CAGR is 0.86%, its digital segment is a key growth driver, now representing 55% of total net revenue. In Q2 2025, digital revenue grew 2.1% year-over-year. The company is profitable on a GAAP basis, with a net income of $2.0 million in the quarter. With a low forward P/E of 6.58 and a high dividend yield of 11.36%, the company may be undervalued, and short interest is minimal at just 1.25% of the float.

Name: John Paulson

Position: Director

Transaction Date: 08-11-2025 Shares Bought: 3,243,049 shares an Average Price Paid of $6.56 for Cost: $21,267,731

Company: Bausch Health Companies Inc. (BHC):

Bausch Health Companies Inc., headquartered in Laval, Canada, is a diversified specialty pharmaceutical and medical device company with operations worldwide. Its five business segments—Salix, International, Solta Medical, Diversified, and Bausch + Lomb—cover a wide range of therapeutic areas, including gastroenterology, hepatology, neurology, dermatology, generics, OTC products, aesthetics, and eye health, with Salix focusing primarily on gastrointestinal products.

John A. Paulson has served as a director of Bausch Health Companies Inc. since June 2017 and was appointed Chair of the Board in June 2022. He is the founder and president of Paulson & Co., a hedge fund established in 1994. Earlier in his career, he worked in mergers and acquisitions at Bear Stearns. Mr. Paulson holds a bachelor’s degree from New York University and an MBA from Harvard Business School.

Hedge Fund Insomniac’s Opinion:

Bausch Health Companies Inc. (BHC) is a diversified healthcare company. While its financial performance has been inconsistent, with a 5-year cumulative revenue growth of 9.91%, recent results are strong. In Q2 2025, revenue grew by 5% to $2.53 billion, driven by its Salix and Solta segments. The company reported a GAAP net income of $148 million and a strong Adjusted Gross Margin of 70.6%. The stock has seen a significant increase of 30% in the past month, following the earnings beat. A key challenge is the substantial $16.1 billion in gross debt, though the company is trading at a low forward P/E of 2.28, which may indicate it’s undervalued.

Name: Peter M. Neupert

Position: Director

Transaction Date: 08-08-2025 Shares Bought: 62,500 shares an Average Price Paid of $6.51 for Cost: $407,150

Company: Fortrea Holdings Inc. (FTRE):

Fortrea Holdings, Inc., founded in 2023 and headquartered in Durham, North Carolina, is a contract research organization providing global biopharmaceutical product and medical device development services. Operating through its Clinical Services and Enabling Services segments, the company offers expertise from clinical pharmacology to full clinical development, along with patient access solutions and trial technology to streamline randomization and drug supply. Fortrea delivers its services through full-service, functional service provider, and hybrid models, offering Phase I–IV trial management, technology-enabled solutions, post-approval services, and consulting.

Peter M. Neupert has served on Fortrea Holdings Inc.’s Board of Directors since its spin-off from Labcorp on June 30, 2023, and was appointed Chairman and Interim Chief Executive Officer in mid-May 2025. He holds a Bachelor of Arts in Philosophy from Colorado College and an MBA from the Tuck School of Business at Dartmouth College.

Hedge Fund Insomniac’s Opinion:

Fortrea Holdings Inc. (FTRE) is a contract research organization that has a volatile financial history, with a 5-year cumulative revenue growth of -5.14%. The company is not profitable on a GAAP basis, posting a large net loss of $374.9 million in Q2 2025 due to a non-cash goodwill impairment charge. However, on an adjusted basis, it reported a profit of $17.6 million, with revenue growing 7.2% year-over-year to $710.3 million. The stock surged over 20% following the earnings beat and raised guidance. A key concern is the company’s recent book-to-bill ratio of 0.79x, which signals a slowdown in new business. Short interest remains high at 14.34% of the float, indicating significant bearish sentiment.

Name: James V. Continenza

Position: Executive Chairman And CEO

Transaction Date: 08-14-2025 Shares Bought: 50,000 shares an Average Price Paid of $5.74 for Cost: $287,000

Company: Eastman Kodak Co. (KODK):

Kodak is a global manufacturer specializing in commercial printing, advanced materials, and chemicals. With more than 79,000 patents developed over 130 years of research and innovation, the company leverages technology and science to enhance visual and creative experiences. Its award-winning products and customer-focused approach have established Kodak as a trusted partner for commercial printers worldwide. Dedicated to environmental stewardship, Kodak also leads the industry in advancing sustainable printing solutions.

James V. Continenza has served as Executive Chairman of Eastman Kodak Company since February 2019 and as Chief Executive Officer since July 2020. He joined Kodak’s Board of Directors in April 2013 and was appointed Chairman in September 2013. With extensive experience guiding technology companies through transformation, he has held senior leadership roles at Vivial Inc., STi Prepaid LLC, Teligent Inc., and Lucent Technologies Product Finance. He has also served on the boards of Cenveo Corporation, Sorenson Communications, Datasite LLC, NII Holdings, Inc., Tembec, and Neff Corporation, among others. Mr. Continenza earned a Bachelor’s degree in Business Administration from the University of Wisconsin–River Falls in 1984.

Hedge Fund Insomniac’s Opinion:

Eastman Kodak Co. (KODK) is a diversified technology company with a limited competitive moat and a history of declining revenues. The company’s 5-year cumulative revenue growth is -6.62%, with Q2 2025 revenue of $263 million, representing a 1% year-over-year decrease. The company is not consistently profitable, posting a net loss of $26 million in Q2 2025, a significant reversal from the prior year. This, along with a low gross margin of just 19%, highlights profitability challenges. Following the earnings report, the stock declined by 3.41%. Short interest is high at 12.93% of the float, indicating significant bearish sentiment.

Name: Dawn N. Fitzpatrick

Position: Director

Transaction Date: 08-13-2025 Shares Bought: 100,000 shares an Average Price Paid of $4.93 for Cost: $493,000

Company: Under Armour Inc. (UA):

Under Armour, Inc., founded in 1996 and headquartered in Baltimore, Maryland, is a global leader in performance apparel, footwear, and accessories for men, women, and youth. Its product lineup spans compression, fitted, and loose-fit clothing, footwear for running, training, basketball, cleated sports, recovery, outdoor, and lifestyle wear, as well as accessories such as gloves, bags, hats, and socks. Beyond products, Under Armour drives growth through brand licensing, digital subscriptions, and advertising initiatives. The company reaches consumers worldwide via wholesale channels, independent distributors, institutional sports programs, branded retail stores, and e-commerce platforms across North America, EMEA, Asia-Pacific, and Latin America.

Dawn N. Fitzpatrick joined Under Armour’s Board of Directors as an Independent Director in April 2025. She is CEO and Chief Investment Officer of Soros Fund Management, where she has served since 2017, after a 25-year career at UBS culminating as Head of Investments for UBS Asset Management. She also brings governance and advisory experience from roles with Barclays, the Federal Reserve Bank of Dallas, the Bretton Woods Committee, and the Bloomberg New Economy Advisory Board. Fitzpatrick earned her bachelor’s degree from the Wharton School at the University of Pennsylvania.

Hedge Fund Insomniac’s Opinion:

Under Armour Inc. (UA) is an athletic apparel company with a limited competitive moat and a challenging financial profile. The company’s revenue growth has been inconsistent, with Q2 2025 revenue of $1.4 billion, representing an 11% year-over-year decrease. While it reported a GAAP net income of $170 million in the quarter, adjusted net income was $131 million. A gross margin of 49.8% was achieved, but overall profitability still lags behind its primary rivals. The stock saw a brief surge after a Q2 earnings beat, but it remains down significantly for the year. Short interest is notable at 7.36% of the float, or 9.08 million shares, indicating a degree of bearish sentiment among investors.

Name: Clint D. Coghill

Position: Director

Transaction Date: 08-12-2025 Shares Bought:350,000 shares an Average Price Paid of $3.82 for Cost: $1,335,989

Company: Amplify Energy Corp. (AMPY):

Amplify Energy Corp., headquartered in Houston, Texas, is an independent oil and natural gas company focused on the acquisition, development, exploitation, and production of energy properties across the United States. Its portfolio includes operated and non-operated interests in producing and undeveloped leasehold acreage, with key assets located in Oklahoma, the Rockies, federal waters offshore Southern California, East Texas/North Louisiana, and the Eagle Ford. The company’s holdings encompass both producing wells and significant resource potential for future development.

Clint D. Coghill was appointed Lead Independent Director of Amplify Energy Corp. on May 16, 2025. With nearly 30 years of experience as a money manager, software entrepreneur, and philanthropist, he co-founded and led Backstop Solutions Group until its sale in 2021, later serving as Head of the Investor Segment at ION Analytics. Previously, he was President and CIO of Coghill Capital Management LLC. He holds a B.A. in Business Administration from the University of Arizona and an M.B.A. from the London Business School.

Hedge Fund Insomniac’s Opinion:

Amplify Energy Corp. (AMPY) is an oil and gas company with a limited competitive moat. While it has an inconsistent revenue history, with a 5-year cumulative revenue growth of -26.65%, its latest Q2 2025 revenue of $68.36 million beat analyst estimates despite a year-over-year decline. The company reported a GAAP net income of $6.4 million in the quarter, with a low P/E ratio of 11.0 and a trailing twelve-month net income of $15.75 million. Its management is focused on debt reduction, selling assets to reduce its debt of $130.0 million as of June 30, 2025. Bearish sentiment is low, with short interest at just 3.56% of the float, and recent insider share purchases indicate confidence.

Name: Christopher Stansbury

Position: EVP & CFO

Transaction Date: 08-14-2025 Shares Bought: 82,000 shares an Average Price Paid of $4.36 for Cost: $357,753

Name: Kathleen E. Johnson

Position: President & CEO

Transaction Date: 08-05-2025 Shares Bought: 135,870 shares an Average Price Paid of $3.69 for Cost: $501,781

Company: Lumen Technologies Inc. (LUMN):

Lumen Technologies Inc. is a global networking company that connects people, data, and applications with speed, security, and ease. Offering a wide range of integrated products and services, it serves both domestic and international business clients, as well as the U.S. mass market. Operating one of the world’s most interconnected communications networks, Lumen enables real-time adjustments to digital programs, helping customers boost productivity, accelerate market access, and reduce costs, while providing the flexibility to adapt IT strategies to rapidly changing demands.

Christopher Stansbury is Executive Vice President and Chief Financial Officer of Lumen Technologies, a role he assumed in April 2022. He leads the company’s global finance, supply chain, and real estate functions. Previously, he served as CFO of Arrow Electronics, held senior finance roles at Hewlett-Packard’s Networking Group, and worked in finance at PepsiCo. Mr. Stansbury earned an MBA from the Wharton School of the University of Pennsylvania and a bachelor’s degree from the University of Western Ontario.

Kate Johnson, President and CEO of Lumen Technologies since 2022, brings extensive expertise in enterprise digital transformation from leadership roles at Microsoft, GE Digital, Oracle, Red Hat, UBS Investment Bank, and Deloitte Consulting. She holds a Bachelor’s degree in Electrical Engineering from Lehigh University and an MBA from The Wharton School, University of Pennsylvania.

Hedge Fund Insomniac’s Opinion:

Lumen Technologies (LUMN) faces significant challenges, including a history of declining revenue with a negative 5-year cumulative revenue growth. Its Q2 2025 revenue was $3.09 billion, a 5.4% decrease year-over-year. The company is not profitable on a GAAP basis, reporting a net loss of $915 million in the quarter due to a $628 million goodwill impairment charge. Its significant debt burden is a major concern. Short interest is high, at 61.72 million shares or 6.53% of the float, reflecting market skepticism despite recent efforts to stabilize the business.

Name: Steven Taslitz

Position: Director

Transaction Date: 08-07-2025 Shares Bought: 200,000 shares an Average Price Paid of $1.42 for Cost: $284,000

Company: BRC Inc. (BRCC):

Black Rifle Coffee Company, founded in 2014 by U.S. Army Veteran Evan Hafer with a one-pound coffee roaster in his garage, is a veteran-operated premium coffee, energy drink, and media brand with distribution through wholesale, direct-to-consumer, and outposts. Headquartered in Salt Lake City, Utah, San Antonio, Texas, and Nashville, Tennessee, with a manufacturing facility in Manchester, Tennessee, the company offers roast and single-serve coffee, ready-to-drink coffee, Black Rifle Energy beverages, branded apparel, brewing equipment, and outdoor lifestyle gear, all while supporting active-duty military, veterans, first responders, and patriotic consumers.

Mr. Taslitz has served as a Director of BRC Inc. since 2018 and also sits on the boards of Datacubed Health, Stella, Fancy Sprinkles, They Are Giant, and Wengen Alberta. He co-founded Sterling Partners in 1983, where he continues to serve as Chairman, and holds a BS in Accounting with Honors from the University of Illinois.

Hedge Fund Insomniac’s Opinion:

BRC Inc., or Black Rifle Coffee Company, is a mission-driven brand with a competitive moat built on brand loyalty. While its 5-year cumulative revenue growth is 22.8%, its recent performance is mixed. In Q2 2025, revenue grew 6.5% year-over-year to $94.8 million, beating expectations. However, the company is not profitable, posting a net loss of $14.5 million and a declining gross margin of 33.9%. The stock dropped over 10% due to profitability concerns. A key strength is the 14.1% growth in its wholesale channel, which is offsetting a 7.8% decline in its direct-to-consumer business. Short interest remains at a moderate 5.13%.

Name: Frank Martell

Position: Chief Executive Officer

Transaction Date: 08-11-2025 Shares Bought: 230,000 shares an Average Price Paid of $1.32 for Cost: $304,710

Transaction Date: 08-08-2025 Shares Bought: 150,000 shares an Average Price Paid of $1.25 for Cost: $187,500

Name: Thomas N. Bohjalian

Position: Director

Transaction Date: 08-11-2025 Shares Bought: 175,000 shares an Average Price Paid of $1.28 for Cost: $223,250

Company: SmartRent Inc. (SMRT):

SmartRent Inc.is an enterprise real estate technology company offering a comprehensive cloud-based management platform for property owners, managers, and tenants. Integrating smart building technology with its software-as-a-service solutions, SmartRent provides continuous visibility and control over real estate assets, helping owners and operators reduce costs, boost revenue, streamline operations, and protect assets, while enhancing the living experience for residents.

Frank Martell, appointed President and CEO of SmartRent Inc. on June 16, 2025, and a Board member since June 2024, brings nearly 30 years of executive leadership in real estate and technology, including prior CEO roles. He holds a Bachelor of Science in Accounting from the Villanova School of Business.

Thomas N. Bohjalian joined SmartRent Inc.’s Board of Directors in June 2025 and serves on the Audit and Compensation committees. With over 30 years of experience in real estate investing and public company governance, he currently chairs the Board of Healthcare Realty Trust and previously served on multiple other boards. He spent nearly 20 years at Cohen & Steers, holding senior roles including Executive Vice President, Head of U.S. Real Estate, and Portfolio Manager. Bohjalian holds a Bachelor of Science in Business Administration and an MBA from Northeastern University.

Hedge Fund Insomniac’s Opinion:

SmartRent (SMRT) is a proptech company providing smart home solutions for the multifamily industry. It’s transitioning to a high-margin, recurring SaaS model. This shift has caused a recent 21% year-over-year revenue decline in Q2 2025 to $38.3 million. However, the market has responded positively, with the stock increasing over 30% after earnings, as Annual Recurring Revenue (ARR) grew 11% to $56.9 million. Recurring revenue now constitutes 37% of total revenue, up from 26% a year ago. The company maintains strong customer relationships with a 108% net retention rate and has initiated a $30 million cost reduction plan, targeting cash flow neutrality by year-end. Despite its strong customer concentration and unprofitability (net loss of -$10.9 million in Q2 2025), its strategic pivot and management’s focus on efficiency have created cautious optimism.

Follow us on Twitter for real-time commentary and insider buying alerts at https://twitter.com/theinsidersfund

If you are a QUALIFIED INVESTOR and are interested in learning how you can be part of the Insiders Fund, schedule some time with me here.

This blog is solely for educational purposes and the author’s own amusement. IT IS NOT INVESTMENT ADVICE. Think of the blog as part of my personal investment journal that I am willing to share with the DIY investor. There are also many parts that I am not willing to share if I think it could influence trading action or be detrimental to the Fund’s partners. We could be long, short, or have no position at all in any of the stocks mentioned and express no written or implied obligation to disclose any of that.

The Insiders Fund and its blogs and posts are not affiliated with, endorsed by, or sponsored by any of the companies mentioned herein. All company names, logos, and trademarks belong to their respective owners. The use of company logos is solely for descriptive and illustrative purposes under fair use. Any information provided is based on publicly available data and should not be considered financial, investment, or legal advice. Readers should conduct their own research or consult with a professional before making any investment decisions.

Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone with any stock market experience pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing of any transaction, buy, sell, exercise, or any other within 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors. SECForm4 is one of the smaller ones, but I like supporting Frank. He is not arrogant. He’s helpful and has great prices. He also trades on his own data, so I like people that eat what they kill.

The bar is different from selling because the natural state of management is to be a seller. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, we analyze unusual patterns with selling, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs, referred to as Rule 10b5-1, are horrendously poor. Also, planned sales that pop up out of nowhere are basically sales and are seeking cover under this corporate welfare loophole. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money on which we are trying to read the tea leaves. I say generally because some 10% shareholders are great investors. Think Warren Buffett and others

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. Do your own analysis. They can easily be wrong, and in many cases, maybe most cases, have no more idea what the future may hold than you or me. In short, you can lose money following them. We have, and we curse aloud; what were they thinking!

We like Fly on the Wall for keeping up with what events might be happening, analysts’ comments, and whatever else could be moving the stock. Dow Jones news service is an essential tool, but many services pick up their feed like they do Bloomberg. For quick financial analysis, it’s hard to beat Old School Value.

A big callout to my assistant Ambreen who sets up this conversation by listing the notable buys that I’ve identified as soon as practically possible. She probes the 10k for a reasonable description of the business. I’ve found that to be the most accurate and succinct place to find out what a business actually does. When I have time, over the weekend, I’ll add some preliminary analysis to the Opinion at the end. Sometimes I won’t update this for a couple of weeks or more. A good way to use this blog is as I do, it’s a reference point and filing cabinet for various stocks with notable insider buying. It’s one of many tools I use. I regularly live on Chat GPT and Microsoft Copilot now. I find the footnotes research very helpful in eliminating errors from AI hallucinations.