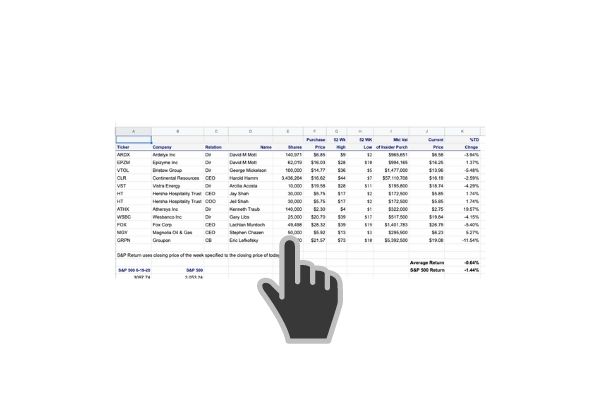

For trade details click on this link to the trades

Now that everyone seemingly is glued to what insiders are doing, it struck me as ironic that they are doing very little. Here are the notable buys from last week, in descending order of return:

insider-trading/1101215.htm”>ALLIANCE DATA SYSTEMS CORP up 23.96%

MSC INDUSTRIAL DIRECT CO INC up 9.74%

ENTERPRISE FINANCIAL SERVICES CORP up 5.48%

BROWN & BROWN Inc up 3.20%

SCHWAB CHARLES CORP up 3.07%

TEXAS INSTRUMENTS INC up 1.81%

CROWN CASTLE INTERNATIONAL CORP down -1.15%

Alliance Data Systems Corporation

Director Gerspach bought 6000 shares of ADS at $68.46. Alliance Data Systems Corporation is a publicly-traded provider of loyalty and marketing services, such as private label credit cards, coalition loyalty programs, and direct marketing, derived from the capture and analysis of transaction-rich data. ADS reported 4th quarter earnings of $3.31 versus $2.41. The Company said that the delinquency ratio was 4.4% versus 5.0$ last month. ADS moved up sharply during the week as it getting a mention on an insider buying segment on CNBC. I wouldn’t chase it here but safe to write February 65 puts. At least that’s what The Insiders Fund did.

MSC Industrial Direct Co

Director 10% Owner Jacobson bought 67,796 shares of MSM at $78.04. This was a monster buy, $5.29 Million. Of course, this is all relative. According to Forbes, Mitchell Jacobson began working for MSC Direct, an office and industrial equipment distributor founded by his father Sidney, in 1976. In 1995, Jacobson took over as CEO of the Melville, N.Y.-based firm, which now distributes hundreds of products, from staplers to air conditioners. Jacobson held the CEO position through 2005 and, since 2013, the non-executive chairman. With nearly 15% ownership, he is the largest shareholder.

I don’t see what Jacobson is buying here. The recovery is underway. It will pick up speed, no doubt but MSM is already above pre Pandemic prices.

Enterprise Financial Services Group Inc

Brown & Brown Insurance

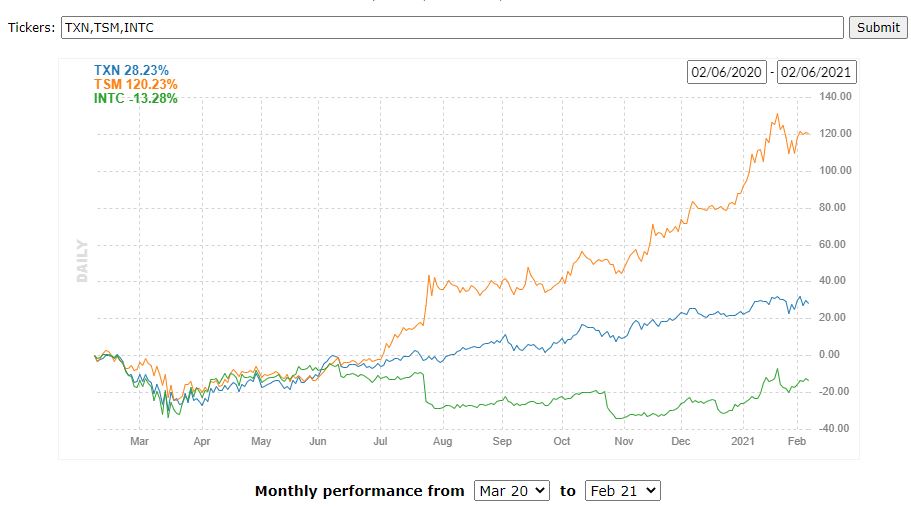

Texas Instruments

Click the chart above to enlarge

Crown Castle

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019