For trade, details click on this link to the trades

COTY Inc up 16.52%

BridgeBio Pharma Inc. up 6.69%

Corvus Pharmaceuticals Inc. up 7.43%

TWO HARBORS INVESTMENT CORP. up 5.53%

Beyond Air Inc. up 0.90%

Black Knight Inc. up 1.45%

TWO HARBORS INVESTMENT CORP. up 4.`3%

NU SKIN ENTERPRISES Inc up3.20%

SVB FINANCIAL GROUP up 3.27%

Adtalem Global Education Inc. up 0.80%

LPL Financial Holdings Inc. up .72%

EVEREST RE GROUP LTD down -2.07%

CVS HEALTH Corp down 2.19%

KKR & Co. Inc. down 2.83%

Bumble Inc. down 5.88%

Longeveron Inc.down 38.29%

Coty Insiders are at it again. Three different insiders bought last week on the latest of a string of earnings disappointments at this multinational beauty company. Coty owns around 77 brands as of 2018. Wikipedia .

Hope springs eternal at Coty. I don’t know what they are putting in the makeup but you can’t make up these votes of confidence. Last week, Director Singer, Prize, and Goudet bought 75,000, 15,225, and 50,000 shares of COTY at prices between $6.60 and $6.86. Coty had been reeling from overpaying for Clairol’s stagnant beauty brands when the pandemic hit.

The CEO of Corvus Pharmaceuticals purchased 100,000 shares at $3.50 on a 9.78 million share secondary offering. Orbimed Advisors, a health care focused investment manager, purchased $1.3M of common stock at $3.5 adding to their holdings. Corvus Pharmaceuticals is an immunology-focused biopharmaceutical company developing drugs and antibodies that target the most critical cellular elements of the immune system. On February 4th they started a Phase 3 trial of their molecule, CPI-006, for the treatment of hospitalized patients with Covid-19. They expect to enroll approximately 1000 patients with a readout in the 4th quarter of 2021.

We would not buy the stock for a Covid play, though, as the field seems crowded, more so with vaccines rolling out. Their pipeline includes five proprietary agents with differentiated mechanisms of action. Those in the most advanced stages of development are focused on targeting the most critical cellular elements of the immune system. Covid-19 is the furthest along.

Director Carey purchased 15,000 shares of Beyond Air at $6.67. Carey has been accumulating shares since 6-13-2019 when he purchased 19,418 XAIR at $5.15. His purchases accelerated in August when he purchased 80,000 shares. Beyond Air is a clinical-stage medical device and biopharmaceutical company using nitric oxide to treat respiratory and other diseases. Their LungFit™ system uses proprietary technology to generate nitric oxide from ambient air and transform the lives of patients with respiratory conditions and severe lung infections. A separate unique delivery system allows for the administration of ultra-high nitric oxide concentrations directly to solid tumors.

No question they could sell a bunch of these units to vendors at Grateful Dead concerts but I have no idea of the practicality of these units in the “approved” medical usage market. Biotech and med techs are particularly dangerous investments when they get a product or drug approved. It’s put up or shut up time. That’s just about where XAIR is now. The way I’d play it is to see how the product sells once it is approved. It will likely disappoint as these things take time to educate the buyers and build a market. Once on the market for a few months to a year, if it starts to show sales momentum, then buy. Otherwise, we have been sitting on the sidelines.

Two insiders bought shares in BridgeBio Pharma. Brian Stephenson, PH.D and CFO bought 8,000 shares at $62.50 and Director Scott plunked down a cool $1 million at $62.50. When you see two insiders buying the stock at the same price, it’s a certain tip-off they did a secondary. But that’s the nature of biotechs. A biotech CEO is nothing more than a glorified fundraiser for a nonprofit. That’s not meant to belittle the effort. These are real dollars the directors and officers are spending to buy their own risky stock. All the more striking because Stepheson has spent the last year selling hundreds of thousands worth of stock at half of where he bought it. Go figure that? Perhaps that is what it took to get the secondary off the ground

BBIO specializes in targeting the known drivers of genetic diseases with precision medicine techniques to develop drugs that show promise of becoming safe, effective therapies. That’s sufficiently amorphous but they do have a few things in Phase III and on the cusp of becoming commercial. Goldman Sachs analyst gave it an $83 target and said it had a catalyst-rich year ahead with significant upside potential for 2021. If it pulls back to the secondary price and holds there for a day or two, I’d pull the trigger. They are tackling rare diseases that are quite horrible. It would be wonderful if you could make some money and help mankind. We have it on our shopping list.

Two Harbors Investment Group looks like a good high yield opportunity when the CEO and the CIO both are buying stock. CEO Greenburg purchased 35,000 shares of TWO at $6.58. CIO Koeppen bought 20,000 shares at $6.66 effectively giving copy caters the all clear for a while. At Friday’s close, this yields 9.8%. The real trick though is in a rising rate environment like it seems we might be headed into, will these kinds of residential mortgage REITs come back to bite you in the ass. I don’t know the answer to that so I wouldn’t be a long-term investor but for now, the coast is clear if you want to pick up a dividend or two. Remember you can lose more on principal with interest rates rising than you can hope to pick up with extra income from a high dividend. I think you should be very careful with this name.

Nu Skin Enterprises announced a horrific quarterly forecast on its recent earnings report. They blew out their earnings, reporting $1.40 4th Qtr EPS versus consensus $1.19 but forecast Q1 revenue of $610-$640 M versus consensus of $647 million. The stock got whacked appropriately. NUS is one of those hometown success stories that have taken the multi-level marketing model to unforeseen heights. I know the company had been growing rapidly but Provo, UT-based MLM NuSkin saw year-over-year revenues fall by 10% as a result of the continued regulatory pressure in China. The COVID-19 disease outbreak is expected to depress results even further in the coming year.

Founded in 1984, Nu Skin Enterprises, Inc. (NYSE:NUS), is a direct selling company that distributes more than 200 premium-quality anti-aging products in both the personal care and nutritional supplements categories. Nu Skin operates throughout Asia, the Americas, Europe, Africa and the Pacific. The company’s global operations generated $2.42 billion in revenue during 2019. In 2019, the Nu Skin Force for Good Foundation and through its charity partners donated $10.3 million to improve the lives of children throughout the world. Since 2002, Nu Skin distributors and employees have donated more than 700 million meals through its Nourish the Children® initiative to hungry and malnourished children around the world.

Insiders apparently believe the market may have overreacted to this earnings-related news. I tend to agree. Now I’ve never been one that’s had a lot of respect for the MLM model of sales but $640 million a quarter in cosmetics and skincare sales during a pandemic is an impressive number no matter how you look at it. Apparently the Chairman of the Board, Steven Lund felt something similar when he coughed up $1 million to buy 20,850 shares at $48.05. Director Campbell followed suit with 9,910 shares at $50.64. NUS is a cash cow and trades at just 10.6 times free cash flow. It has a pristine balance sheet with more cash on hand than debt. This is a value buy and we are into it. Just keep this in mind, MLM skeptics, NUS skin with its cash flow and pristine balance sheet could buy just about any skin care company they want including, $AMRS, Biossance, or Pipette. Nuskin is tied to Utah and that means tied to the Mormon church, which just happens to be one of if not the fastest-growing religions. Thousands of young Mormon missionaries traveling around the world every year can spread the Nu Skin gospel as well. Strong buy here on this pullback.

Director Phelan bought 2500 shares of ATGE at $41. Adtalem Global Enterprises is the new name for Devry. Devry itself has had so many reincarnations that picking a name no one can remember is actually logical.

For-profit higher education in the United States has been the subject of hearings by the United States Senate Committee on Health, Education, Labor, and Pensions. Specifically, regarding DeVry, the Committee[12] found that over half of the students enrolled at DeVry in 2008-2009 withdrew by mid-2010.[13] DeVry spends more on marketing than on student instruction.[13] Approximately 80% of DeVry’s revenue is Federal education funds.[13]As of 2013, DeVry Inc. was under investigation by the Attorneys General of the states of Illinois and Massachusetts.[14][15]

Whatever your position is on for-profit education, insiders have been steadily buying ATGE. Director Malafrone bought 6000 at $39.25 on 2/5/20 and Director Burke picked up 1000 at $40.06 on 2/4/20. I have a feeling business is getting better. Maybe all these unemployed people going back to school to get retooled during the pandemic may boost revenue.

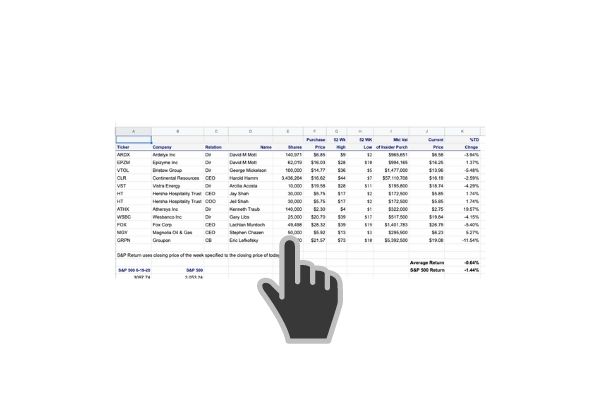

![]()

Director Ludwig added to his holdings of CVS Health purchasing 3000 shares at $72 last week. There have only been two insider buys during the last twelve months at CVS. VP Lotvin bought 5000 shares at $53.13 on 5/11/20. You are not going to get rich buying CVS but you will probably make money in the short term. I see bullish divergence on the 7 day time period. If you’re a swing trader, you’ll understand what I’m saying. CVS sees FY21 free cash flow from operations of $12-12.5 B. If that holds up they could pay down their monstrous $59B long-term debt in just five years. That would be a better use of cash than share buybacks. Vaccination for the pandemic is a shot in their arm as they are going to get a lot people coming into the stores rolling up their sleeves.

Director Scully bought 26,000 shares of KKR & Co., Inc at $48.13. KKR is an American global investment company that manages multiple alternative asset classes, including private equity, energy, infrastructure, real estate, credit, and, through its strategic partners, hedge funds. Wikipedia. Wealth begets wealth in this country. I bet Scully wishes he hadn’t sold his stock in 2016 when he unloaded 168,400 shares at $14.22.

When the Chief Scientific Officer of a biotech company buys $1 million of his Company’s stock, normally stock traders take notice. Not here. Joshua Hare made an open market purchase of 103,000 shares of Longeveron at $9.98 on the Company’s IPO. Within a week, he’s down a stunning 38%. Longeveron has been one of the worst-performing IPOs in one of the strongest markets I’ve ever seen. Is Aging Frailty just a hoax? Another one of the live forever theories promulgated by aging billionaires. The answer to that really won’t matter. If the FDA approves something for aging frailty it will be a blockbuster. Just like on the HBO show Silicon Valley where the aging tech magnates are transfusing themselves with the blood of young techies they hire. It reminds me of something Oscar Wilde opined in his 1889 essay The Decay of Lying that, “Life imitates Art far more than Art imitates Life.

LGVN is a clinical-stage biotechnology company developing cellular therapies for aging-related and life-threatening conditions. Their lead investigational product is Lomecel-B™, which is derived from culture-expanded medicinal signaling cells (MSCs) that are sourced from bone marrow of young healthy adult donors. They believe that by using the same cells that promote tissue repair, organ maintenance, and immune system function, we can develop safe and effective therapies for some of the most difficult diseases and conditions associated with aging.

So what’s wrong with this picture? A lot of people believe in the regenerative power of stem cells, including doctors and scientists although there is plenty of skepticism too. You won’t find any major health insurance companies that will pay for stem cell treatment. It doesn’t help either that the FDA has a warning on their website about stem cell treatment.

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019