For trade details click on this link to the trades

| insider-trading/1556739.htm”>Thryv Holdings Inc. | THRY | 31.92% |

| Veritiv Corp | VRTV | 9.07% |

| Advantage Solutions Inc. | ADV | 8.72% |

| Advantage Solutions Inc. | ADV | 6.96% |

| Limoneira CO | LMNR | 6.71% |

| MANAGEMENT CO"}” data-sheets-hyperlink=”https://www.secform4.com/insider-trading/922864.htm”>APARTMENT INVESTMENT & MANAGEMENT CO | AIV | 3.59% |

| Limoneira CO | LMNR | 1.58% |

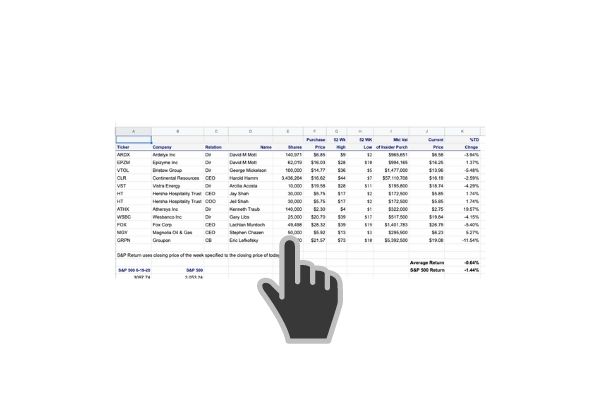

Most people have never heard of these companies. That’s where we are at in this cycle. That’s not a good sign for the overall market returns. When the companies you’ve heard of are not buying their own stock, it means they don’t see much value- or it’s flat in the middle of the quarterly earnings blackout which is exactly what it is. Officers and directors are getting a paycheck whether they buy stock or not but we at the Insiders Fund are on the hunt every day. And deft traders could have certainly put game on the table if they were paying attention. Insiders returned 9.79% versus the S&P 500’s weekly 1.57% gain.

CEO Joe Walsh bought 200,000 shares of Tryv Holdings at $18.76 scoring a whopping 31.92% weekly gain on this timely purchase. THRY is a publicly-traded software as a service company. It is headquartered in Dallas, Texas and operates in 48 states with more than 2,400 employees. The company began as a conglomerate of Yellow Pages companies. In June 2020, Thryv reported $1.3 billion in revenue over a twelve-month period. Wikipedia

It seems they’ve reinvited themselves as a small business customer experience company, providing free tools for

- Online listing accuracy check

- Ratings and reviews evaluation

- Customer sentiment analysis

- Social media relevance

- Website experience & performance review

- And more…

But where they make their money is selling credit card processing services, Quickbooks integration, and payment services. They did $1.1 billion in revenues in 2020 down substantially from the $2.418 billion in 2019. They did a 1-8 reverse split in August of 2020. Companies that are doing well split their stock to make it more affordable for everyday investors. They do reverse splits because the stock has sunk to such lows that institutions don’t buy stocks below $5.

Director Macadam bought 5000 shares of Veritif at$30.49 not quite making the $200k cutoff at $197,450. We don’t pay attention to smallish insider buys as they could be window dressing. Most companies expect if not require officers and directors to purchase some shares in their companies. He probably wishes he bought more as he is up 9.05% on the buy.

The bottom line is that this company is broken, riddled with fleas and I wouldn’t touch it. That being said it was up 32% on the week.

Two insiders purchased shares in Advantage Solutions. Now it’s getting a bit more interesting. Professional board member, ex-CEO of Gillette, James Kilts purchased 64,463 shares at $10.89. Overall I’m not that impressed with Kilt’s insider track record but he must have made a lot of money while being CEO of Gilette. When he buys he goes big. The $702 k purchase was not even on the large side for his typical buys. The CEO Tany Domier purchased 27,250 shares at $11.07.

This is where it gets complicated. This is from their most recent 10K-“We are a leading provider of outsourced solutions to consumer goods companies and retailers. We have a strong platform of competitively advantaged sales and marketing services built over multiple decades – essential, business-critical services like headquarter sales, retail merchandising, in-store sampling, digital commerce and shopper marketing. For brands and retailers of all sizes, we help get the right products on the shelf (whether physical or digital) and into the hands of consumers (however they shop). We use a scaled platform to innovate as a trusted partner with our clients, solving problems to increase their efficiency and effectiveness.”

I could go on and on and not make this any clearer. ADV is a big company. They manage and turnkey a lot of business for retailers on Amazon, taking a share of the revenues and profits. They recorded $3.155 billion in revenues in the 4th quarter of 2020 alone. Unfortunately, that’s the only quarter they have as a public company. Advantage Solutions filed to sell 50M shares of Class A common stock for holders. Om March 25th of this year, Advantage Solutions filed to sell 255.5M shares of common stock for holders. If the stockholders are so eager to sell, I’m not sure why Mr. Kilts or the CEO is buying. We purchased a few shares for a trade but after doing a bit more analysis we will be unloading these before the real stampede parade hits. You can buy just about any stock that an insider buys for a couple of days with impunity. Do your research to decide if this is something you want to invest in. Just remember, though, if it is thinly traded, it might be like the lyrics in the Beach Boys’, Hotel California. “We are programmed to receive You can check out any time you like, But you can never leave!”

![]()

Jose De Jesu Loza has been hungry for Lioneira. This is his 4th purchase this month of this agricultural company, think LEMONS, is involved in producing citrus and real estate profits from their agricultural holdings. They are partnered with Lennar and Hovanian on some of their tracts. I actually like this business a little. If you have to buy and you don’t. This is the one I’d buy and hold this week.

REITs are where we are seeing some cluster buying. This time director Terry Considine purchased 300,000 shares of Apartment Investment and Management at $5.72. He was up 3.59% by the end of the week. THIS IS COMPLICATED. Tesla replaced AIV in the S&P 500 on 12/21/20. They spun off their apartment rental business as AIRC on 12/14/20. The stock dropped 85% on that spinoff. So the question is what is left at AIV? Aimco spun off Apartment Income REIT so the resulting company could focus on developing and redeveloping apartment communities. I’m not personally fond of financial engineering and this is what this looks like to me. I’ll pass.

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. I basically use it as my own worksheet. If we make money off this endeavor, no one will be more surprised than me. My sincere hope is that self-directed investors can learn from my realms of experience. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019, 4th Best in November 2020, 4th Best in January 2021 (I kid you not, 2 is actually my lucky number. I’m hoping for that in February when were up 15%)