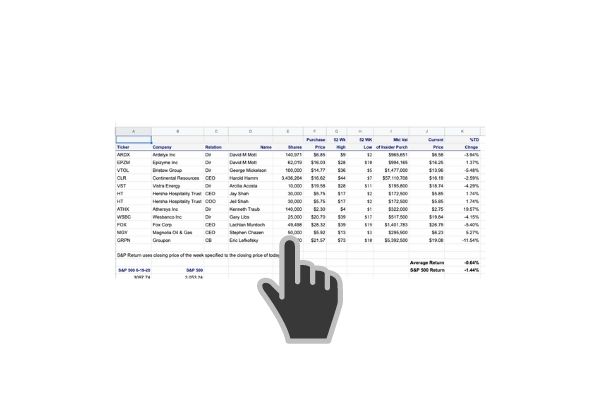

For trade details click on this link to the trades

ATLAS TECHNICAL CONSULTANTS Inc up 28.91%

Organogenesis Holdings Inc. up 3.04%

Kraft Heinz Co up 2.71%

MARAVAI LIFESCIENCES HOLDINGS Inc up 2.52%

BIOGEN Inc up 1.89%

American Homes 4 Rent up 1.89%

HORMEL FOODS CORP up 0.87%

HC2 HOLDINGS Inc down -1.15%

CNX Resources Corp down-1.27%

Black Knight Inc. down -1.27%

Biogen is our pick of the week. Biogen made a fresh push to get aducanumab approved after the early read on the trials was discouring. The stock ran up significantly on the potential for the first drug to show efficacy in the devasting disease, Alzheimer. Biogen, once again robbed bullish investors and the stock The FDA advisory board was not impressed with the data from the trials and BIIB sold off by 28.65% or $18 billion dollars. That’s when the CEO purchased 3,100 shares at $241.31 spending $748,047 to do it. Notably, though there were no insider selling after that punishing news including Alexander Denner on the board representing famed biotech hedge fund investor, Sarissa Capital. BIIB is part of that small group of value biotechs, trading at just 8X earnings.

According to the November 6th article in Science, Biogen’s Alzheimer’s drug candidate takes a beating from FDA advisers,

“If the U.S. Food and Drug Administration (FDA) wants to approve the first new drug for Alzheimer’s disease in 17 years, it will have to do so against the overwhelming recommendation of the experts it turned to for advice on the matter. An independent advisory panel convened by the agency today to review data on the antibody drug candidate, called aducanumab, concluded that even the strongest available clinical trial data don’t support its effectiveness.

FDA, which is expected to decide about aducanumab by March 2021, doesn’t have to follow the advice of its advisory committees, but it typically does. If approved, aducanumab would be the first Alzheimer’s drug prescribed to slow cognitive decline and would likely bring in tens of billions of dollars in sales for its developer, Biogen. It might also vindicate the battered theory that clearing the brain of the sticky protein called beta amyloid can effectively treat the disease.

During a public comment section of the meeting, people with Alzheimer’s— including some who participated in Biogen studies—and their caregivers strongly urged FDA to approve the drug. But many researchers, including most of the advisory committee members, weren’t convinced by the two large clinical trials of aducanumab—only one of which found evidence of benefit. And the committee was uncomfortable with rosy interpretations of Biogen’s data that FDA presented today and in documents, it released this week.

I’m willing to play the March 2021 date as the stock is likely to rise even with the remote possibility of approval as this is the holy grail of pharma.

Several insiders bought Atlas Technical Consultants ATCX, the most notable being CFO Quins purchase of 75,000 shares at $5.81. Atlas provides professional testing, inspection, engineering, environmental and consulting services from more than 100 locations nationwide. We deliver solutions to both public and private sector clients in the transportation, commercial, water, government, education and industrial markets. They prominently feature their engagement on the ultra-modern Jobs inspired Apple campus. This might be a good infrastructure spending play assuming that the new Biden administration is able to pass some bipartisan infrastructure spending. This seems likely but buying something up 28% is risky. We’ll watch this name for now but this looks like a lock. I can’t think of a better play than an engineering firm like this for a big traditional type of infrastructure play. The Company features bridges, rails, damns, and airports on their website.

![]()

Director Mackie bought 38,710 shares at $5.71 of this allograft medical device company, Organogenesis Holdings. The Company just completed a secondary at $3.25 so it’s unusual to see a director buying the stock at higher prices when there was an opportunity just a few weeks earlier to purchase ORGO shares cheaper. Organogenesis is a leading regenerative medicine company focused on empowering healing through the development, manufacturing and sale of products for the advanced wound care, and surgical and sports medicine markets. Most medical procedures and devices have been negatively impacted by Covid.

![]()

Kraft Heinz Co Director Scefi bought 90,000 shares at $33.22. KHC has an outsized dividend yield of 4.69%. Food staple and packaged food stocks have not had a great year in the stock market. Grocery store shelves are being picked clean and business is great in the store but many of these food giants have restaurant businesses that are down. In addition, increased costs due to Covid are crimping grocery store profits. None the less high paying dividend stocks should perform eventually in a low yielding interest rate environment. Goldman has a $39 price target which seems realistic. It may take a cooling off in the market though before the marginal buyer is interested in KHC.

Hormel Foods VP Lykken bought 6873 shares of HRL at $46.97. We like KHC better but either name is likely to produce some alpha if bought near the prices at the insiders bought.

![]()

Billionaire investor Wayne Hughes has done well with his massive stake in American Homes 4 Rent. He purchased 342,00 shares at $29.05. American Homes 4 Rent is a real estate investment trust based in Agoura Hills, California that invests in single-family rental homes. As of December 31, 2019, the company owned 52,552 homes in 22 states. Its largest concentrations are in Atlanta, Dallas-Fort Worth, and Charlotte, North Carolina. Its obvious in hindsight that buying up massive amounts of single-family homes and renting them out while participating in the appreciation has been a great business since the housing crash of 2009. I just don’t understand his end game. The paltry yield of 0.68% does nothing for investors. At what point do investors cash out and sell the appreciated assets?

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer friendly and responsive I’ve used. This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believe they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001, when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019