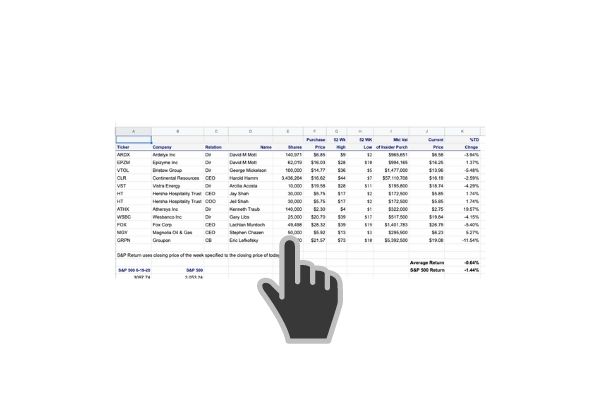

For trade, details click on this link to the trades

For trade, details click on this link to the trades

The efficient market hypothesis assumes that all current information is reflected in the current price of a security. According to the EMH, stocks always trade at their fair value on exchanges, making it impossible for investors to purchase undervalued stocks or sell stocks for inflated prices. When we look at insider buying and selling, we are examining and theorizing the possible motives of the people that know the company the best. What information do they possess that is not already priced into the stock?

Name: Gotlieb Irwin

Position: Director

Shares Bought: 100,000

Average Price Paid: $3.97

Company: COMSCORE Inc. is an American media measurement and analytics company providing marketing data and analytics to enterprises, media and advertising agencies, and publishers. Comscore is a trusted partner for planning, transacting, and evaluating media across platforms. They are a powerful third-party source for reliable measurement of cross-platform audiences with transformative data science and vast audience insights across digital, linear TV, over-the-top (OTT), and theatrical viewership.

Opinion: SCOR was the biggest winner for the week, up 20% from where insides bought. This is the second insider buy in the last few months. Director Livek spent $731K buying 200,000 shares at $3.65 on 3-17. I looked at the Company then and passed because I didn’t see any way an old-school television rand movie rating business reinvents itself. This CEO buy warrants a second look.

The latest quarter in the 10Q showed stagnant revenues and declining profitability. At least they had positive cash flow due to an adjustment in the warrants liability and account payables. Not really the kinds of items that you can depend on repeating. They have a good balance sheet but there is a convertible deal out there that could put some overhang on the stock. Starboard, Cerebus Qurate own a convertible preferred stock of $204.0 million ($68.0 million per investor) at $2.47 per share.

Even though the convert is already in the money, management is buying and that’s a lot of confidence they can get this old dog up and running again.

Name: Laurence Andrew M

Position: VP

Shares Bought: 50,000

Average Price Paid: $36.00

Company: Franchise Group is an owner and operator of franchised and franchisable businesses that continually looks to grow its portfolio of brands while utilizing its operating and capital allocation philosophies to generate strong cash flow for its shareholders. Franchise Group’s business lines include Pet Supplies Plus, American Freight, The Vitamin Shoppe, Buddy’s Home Furnishings, and Liberty Tax Service. On a combined basis, Franchise Group currently operates over 4,600 locations predominantly located in the U.S. and Canada that are either Company-run or operated pursuant to franchising agreements.

Mr. Laurence has served as the Executive Vice President of Franchise Group since October 2, 2019. he has also been a partner of Vintage since January 2010 and is responsible for all aspects of its transaction sourcing, due diligence, and execution.

Opinion: I am not excited about the businesses but this is a large buy, $1.8 million. It was part of an investor group that purchased $36 million at $36 back in a private placement on May 21. All in all, it’s a pretty shoddy lot except for Liberty Tax Services which they just sold.

I bought this last year piggybacking on the CEO, Randall’s purchase of 149,785 shares for $24.99. I spent a little time looking at it and asked myself why do I want to own a run-of-the-mill operation like this and sold it for a small gain. Now it’s up 40% six months later and the same CEO as part of an investor group shelled out $36 million to buy 1,000,000 shares at $36. So what the heck am I missing?

It seems like this is financial engineering with a good sponsor B.R. Riley behind them. They sold off Liberty for over $200 million to a SPAC and took back a healthy piece of the SPAC. They acquired Pet Supplies. No doubt they will use their stock as a public currency to buy and grow other franchises.

Name: Jabbour Anthony M

Position: CEO

Shares Bought: 47,700

Average Price Paid: $20.96

Company: The Dun & Bradstreet Corporation is an American company that provides commercial data, analytics, and insights for businesses. It is headquartered in Jacksonville, Florida. Often referred to as D&B, the company’s database contains more than 300 million business records worldwide.

Opinion: Anthony Jabbour is the Chief Executive Officer (CEO) of Dun & Bradstreet. Anthony concurrently serves as CEO of Black Knight, Inc., a premier provider of integrated software, data, and analytics to the mortgage industry. Prior to joining Black Knight, Anthony was the Chief Operating Officer of FIS, a global leader in financial services technology, ranked as the number one fintech for the past several years. As you can see from the chart above he hasn’t done much yet to make this old-school business relevant today. DNB is debt-burdened from a private equity deal. while credit reporting agencies, Equifax and Experian have soared in value.

Jabbour is betting literally millions of dollars of his own money on this turnaround. On 2-11, he shelled out $1 million at $23.26, on 11-6-2020 another $1 million at $26.31, one 7-2-20 $4.4 million at $22 as part of the IPO. Just remember though that DNB went private in 2018 in a $5.38 billion deal. Although public shareholders haven’t done well this time around, private equity has doubled their investment with DNB’s $9.3 billion market cap at today’s prices. These investors will have only so much patience for Mr. Jabbour to do his magic before they start unloading their stock. We own this stock and wish we haven’t but aren’t selling either.

One word of suggestion to Mr. Jabbour. Find someone who knows how to sell advertising to Facebook and Google. You’re not Steve Jobs, Elon Musk, or even Jack Dorsey who can run more than one. successful business.

Name: Jabbour Anthony M

Position: CEO

Shares Bought: 13,900

Average Price Paid: $71.77

Company: Black Knight is a leading provider of integrated software, data and analytics solutions that facilitate and automate many business processes across the homeownership life cycle. Black Knight is committed to being a premier business partner that clients rely on to achieve their strategic goals, realize tremendous success, and better serve their customers. By delivering best-in-class software, services, and insights with a relentless commitment to excellence, innovation, integrity, and leadership.

Opinion: With home purchases, related accessory goods, and just about everything related to the home on fire, one has to question why Black Knight software isn’t lighting it up. Perhaps it has something to do with their massive investment in DNB and their dual CEO structure. It’s nice to see Mr. Jabbour investing $1 million in BKI as well as DNB. Cleary his financial advisor has explained the risks of investing in the company you own. You lose your job, your company, and your investment all at the same time. The Company cited risks to their investment in DNB in their 10 K (surprising how few retail investors read this important document at all) Risks Related to Our Investment in DNB from the 10K As of December 31, 2020, we have invested $492.6 million in Dun & Bradstreet Holdings, Inc. DNB may not be successful in developing and implementing its strategic plans to transform its businesses, including realigning management, simplifying and scaling technology, expanding and enhancing data and optimizing its client services.

Name: Berle Dolf A

Position: CEO

Shares Bought: 36,500

Average Price Paid: $17.45

Company: Lindblad Expeditions Holdings is an expedition travel company that focuses on ship-based voyages through its Lindblad Expeditions brand and on land-based travel through its subsidiaries, Natural Habitat Adventures, Off the Beaten Path, and DuVine Cycling and Adventure. In 2021, they acquired Off the Beaten Path, based in Boseman, Montana, and DuVine Cycling and Adventure

Opinion: Lindblad Expeditions works in partnership with National Geographic to inspire people to explore and care about the planet. If you make a ton of money on this stock you have to hop on one of their off-the-chart trips. I have been wondering what all these executives that are unloading millions of dollars of stock can do with the money. An expedition trip with Lindblad could cost a family of four $50,000. Carnival, Royal Caribbean, and anything travel-related has staged a comeback in the market in anticipation of pent-up demand.

It’s the perfect way to spend some of that dough that corporate insiders are raking in from unloading their stock at record prices. The market is currently fragmented and primarily comprised of private operators like Silversea Expeditions, Quark Expeditions, Compagnie du Ponant, Hurtigruten, and UnCruise Adventures. They compete with land-based operators Abercrombie & Kent, Overseas Adventure Travel and Mountain Travel Sobek.

In 2019 the Company earned $.29 share and about -$33.4 million free cash flow. There are about 50 million shares outstanding which put the company’s market cap at around $875. An enterprise value of $1.2 billion might not be too bad considering they have a number of vessels and an iconic brand. They just need to figure out how to make money.

I wonder if the new CEO finds it frustrating that while he is buying the company’s stock, his directors are selling. He bought shares in May at $16.49 spending about $362K. Berle came on board, pun intended, around March from Top Golf where he was the CEO. This has been a family business and the Lindblad’s are handing over the reins to a new guy. I’d rather spend my money on a National Geographic adventure cruise with them before committing to investing. If you’re an analyst out there, take me with you. The company views itself with hotel metrics like a gross yield of $1349 per night. That’s a pretty expensive hotel room.

Name: Kasbar Michael J

Position: CEO

Shares Bought: 10,000

Average Price Paid: $31.40

Company: World Fuel Services Corp.

Description:

World Fuel Services Corporation (WFS, World Fuel) is an energy, commodities, and services company based in Doral, Florida. The company ranked No. 91 in the 2018 Fortune 500 list of the largest United States corporations. WFS focuses on the marketing, trading, and financing of aviation, marine, building, and ground transportation energy commodities and related services. As of 2013, WFS also operates in natural gas and power.

Opinion: This one is a layup. Most of their business comes from jet fuel. There’s been a lot of things out of people’s control during this pandemic but not many more than governmental curbs on air travel. This is a trading business. Given that they know how to trade fuel, more airplane travel equals more profit. How much is already priced in the stock? With all the focus on ESG investing, I doubt much is priced in already.

Name: Bridgeford Gregory M

Position: Director

Shares Bought: 5,100

Average Price Paid: $99.02

Company: Dollar Tree Inc is an American chain of discount variety stores that sells items for $1 or less. Headquartered in Chesapeake, Virginia, it is a Fortune 500 company and operates 15,115 stores throughout the 48 contiguous U.S. states and Canada. Its stores are supported by a nationwide logistics network of twenty-four distribution centers. In addition, the Company operates one-dollar stores under the names of Dollar Tree and Dollar Bills. This Company also operates a multi-price-point variety chain under the Family Dollar banner.

Opinion: Do you really want to compete with Walmart and Amazon? I don’t and I would trade it before I would hold it.

Name: Sandfort Gregory A

Position: Director

Shares Bought: 4,280

Average Price Paid: $58.45

Company: Genesco Inc is an American publicly owned specialty retailer of branded footwear and accessories and is a wholesaler of branded and licensed footwear based in Nashville, Tennessee. Genesco operates more than 1,475 retail stores throughout the United States, Puerto Rico, Canada, the United Kingdom, and the Republic of Ireland and wholesales branded and licensed footwear to more than 1,050 retail accounts through its various subsidiaries.

Opinion: I wish all the stocks I owned had stock charts looking like Genescos. This is a rather smallish buy from a new director. I don’t think it means anything important about future prices.

Name: Balen John V

Position: Director

Shares Bought: 3,000

Average Price Paid: $95.87

Company: Cardlytics Inc. is an advertising platform in banks’ digital channels. They partner with financial institutions to run their banking rewards programs that promote customer loyalty and deepen banking relationships. In turn, they have a secure view into where and when consumers are spending their money. They also use these insights to help marketers identify, reach, and influence likely buyers at scale and measure the true sales impact of marketing campaigns.

Opinion: John V. Balen has served as a member of the Cardlytics board of directors since August 2008 and this is the second time he’s bought stock, buying 50% more at twice the price on this pullback. That’s bullish behavior and I’d follow suit trying to stay as close to his purchase price as ever. I’m still researching what caused the precipitous dip the first week as their large purchase of Bridg had been announced on April 13th.

Name: Mongeau Claude

Position: Director

Shares Bought: 2,350

Average Price Paid: $282.69

Company: Norfolk Southern Corp provides rail transportation services. This Company transports raw materials, intermediate products, and finished goods primarily in the Southeast, East, and Midwest and, via interchange with rail carriers, to and from the rest of the United States. Norfolk Southern also transports overseas freight through several Atlantic and Gulf Coast ports.

Opinion: If you’ve been halfway following the financial news, you’d know there was a bidding war to buy Kansas City Souther by the two Canadian rail giants, Canadian National, and Canadian Pacific. Canadian National won the prize which leaves Canadian Pacific, the jilted suitor.

Is it just chance that Claude Mongeau former president and chief executive officer of the Canadian National Railway Company, buys stock in NSC? Some think Canadian Pacific will come knocking on NSC or CSX door asking to merge sparking another bidding war.

Although faced with diminishing coal and petroleum traffic, railroads should benefit from the deindustrialization of America and the efforts to bring the supply chain home. We’re all in on NSC and leaving the cigar butts where we found them.

Follow us on Twitter for real-time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019, 4th Best in November 2020, 4th Best in January 2021 (I kid you not)