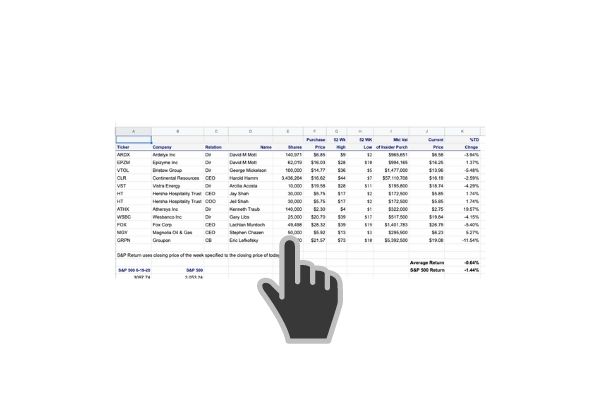

For trade, details click on this link to the trades

For trade, details click on this link to the trades

The efficient market hypothesis assumes that all current information is reflected in the current price of a security. According to the EMH, stocks always trade at their fair value on exchanges, making it impossible for investors to purchase undervalued stocks or sell stocks for inflated prices. When we look at insider buying and selling, we are examining and theorizing the possible motives of the people that know the company the best. What information do they possess that is not already priced into the stock?

Name: Mcguire Terrance

Position: Director

Shares Bought: 96,153

Average Price Paid: $3.12

Company: Cyclerion Therapeutics Inc is an independent, publicly traded company working at the forefront of CNS drug development. Their mission is to develop innovative medicines that improve brain function for patients in desperate need of new treatment options. The NO-sGC-cGMP signaling pathway is critical to essential neuronal function and overall brain health, and impaired NO-sGC-cGMP-signaling is believed to play a vital role in the pathogenesis of many neurodegenerative diseases. They are building on a growing body of data about this pathway to advance a pipeline of severe conditions of the CNS.

Opinion: We are not buying CYCN. This transaction was a private placement issued directly by the company. Terrance is a partner at Polaris Ventures, a VC firm. I usually discount these kinds of insider buys as it’s not his money necessarily and they usually don’t have a big impact on stock prices. Not the case this week. Cyclerion was the winner of the week, shares advancing 27%

Nowhere is insider buying more critical to forming an investment opinion than it is in biotech. Since it may take years of blinded studies in humans before a drug can prove efficacious, even the best scientists and analysts are left in the dark, except the occasional insider. Maybe they’ve seen a peek preview? Maybe some pharma company has come knocking on their door for an acquisition.

Mr.Terrance G. McGuire is an Independent Director at Cyclerion Therapeutics, Inc. Terrance has made over nine trades of the Cyclerion Therapeutics stock since 2013, according to Form 4 filed with the SEC. Most recently, he bought 96,153 units of CYCN stock worth $299,997 on 3 June 2021. The most significant trade he’s ever made was buying 626,117 units of Cyclerion Therapeutics stock on 8 April 2019, worth over $10,017,872.

Name: Hecht Peter M

Position: CEO

Shares Bought: 823,170

Average Price Paid: $3.28

Company: Cyclerion Therapeutics Inc

Dr. Hecht is Chief Executive Officer & Director at Cyclerion Therapeutics, Inc

Name: Lucier Gregory T

Position: Director

Shares Bought: 5,000

Average Price Paid: $41.12

Company: Berkeley Lights is a leading Digital Cell Biology company focused on enabling and accelerating the rapid development and commercialization of biotherapeutics and other cell-based products for our customers. The Berkeley Lights Platform captures deep phenotypic, functional, and genotypic information for thousands of single cells in parallel and can also deliver the live biology customers desire in the form of the best cells. Their mission is to accelerate the use of cell-based products by providing researchers access to the Berkeley Lights Platform to find the best cells in a fraction of the time and at a fraction of the cost of traditional methods.

Opinion: BLI is part of the Kathie Woods ArKK Innovation ETF. Like many of her holdings, it’s had a poor run of it lately. We missed this one. Our proprietary technical analysis spits out bullish RSI divergence on 5-1 thru 5-11 but the price was closer to $37-$40 than $48.80 Friday’s closing price. On top of it, the CTO just sold 8250 shares at $44.46. If you’re going to play these short-swing trades, you have to follow us on our private Twitter feed at twitter.com/theinsidersfund

Name: Drachman Jonathan G

Position: CEO

Shares Bought: 50,000

Average Price Paid: $9.51

Company: Neoleukin Therapeutics emerged from the University of Washington Institute for Protein Design in January of 2019. They are creating next-generation immunotherapies using breakthrough de novo protein design technology. They use natural protein complexes as inspiration to develop custom-designed proteins with superior pharmaceutical properties.

Opinion: Biotech has been a notable laggard and it will take more than insider buying in a handful of obscure stocks to change the market mood. Biogen Alzheimer’s approval last week might have been the catalyst for a change in sentiment but three scientists from the FDA advisory committee that reviewed the efficacy and safety of the drug resigned in protest. Insurance and Payers were up in arms about the Company’s trial balloon pricing of $56,000 per year. Some public policy experts opined that because Alzheimer’s is so prevalent in society, the cost would bankrupt the Medicare system of payments.

The Insiders Fund has put an opportunistic short on Biogen in case the FDA pulls back from the broad approval they granted and caretakers refuse to pay for a drug that doctors don’t believe in. What’s all this to do with Neoleukin. Nothing really but if the sector is in the doldrums, it’s hard for individual stocks to buck the trend.

Jonathan is a seasoned clinician, researcher, and biopharmaceutical executive who joined Neoleukin at the company’s founding in 2018. For 14 years prior, he was at Seattle Genetics, where he most recently served as Chief Medical Officer and Executive Vice President of Research and Development.

Name: Bartlett Mark S

Position: Director

Shares Bought: 25,000

Average Price Paid: $28.03

Company: WillScot Mobile Mini Holdings Corp. Now that WillScot and Mobile Mini have joined forces, they’re better equipped than ever to do what they do best – make life easier for customers. As North America’s leader in the creative, flexible workspace and portable storage solutions, they are the only provider on the continent that can deliver everything customers need. Space. Storage. Furnishings. Services. Everything. With one order from us, they’re Ready to Work.

Opinion: With people on the move again, buying new homes, and workers coming back- money is being spent on storage one way or the other and they are well-positioned as the dominant niche player. We can’t buy everything we want as money runs out but this is one that is likely to work, just not as well as some others.

Mr. Bartlett is a former partner of Ernst & Young LLP and has served as a Director since November of 2017. He joined the accounting firm in 1972 and worked there until his retirement in 2012, serving as managing partner of the firm’s Baltimore office and senior client service partner for the mid-Atlantic region.

Name: Watters John P

Position: COO

Shares Bought: 25,000

Average Price Paid: $18.75

Company: FireEye is a publicly-traded cybersecurity company headquartered in Milpitas, California. It has been involved in the detection and prevention of major cyber attacks. In addition, it provides hardware, software, and services to investigate cybersecurity attacks, protect against malicious software, and analyze IT security risks. FireEye was founded in 2004.

Opinion: With ransomware and cybercrime almost part of the daily news, one would think that the stock would be performing better than it has. FireEye has had a spotty history; lots of promise but failed to execute. It initially focused on developing virtual machines that would download and test internet traffic before transferring it to a corporate or government network. The company diversified over time, in part through acquisitions. In 2014, it acquired Mandiant, which provides incident response services following the identification of a security breach.

They recently announced that they sold the products group for $1.1 billion in cash and were rebranding the Company as their world-renowned Mandiant® consulting practice. With this approach, they claim to eliminate the complexity and burden of cybersecurity for organizations struggling to prepare for, prevent, and respond to cyber-attacks. They have over 9,900 customers across 103 countries, including more than 50 percent of the Forbes Global 2000.

Wall Street analysts were lukewarm about the news. It’s ironic that the Street is lukewarm on the deal but the insiders are voting with their dollars. Director Coviello and COO Waters voted with their dollars

It does seem an easy fix to just hire someone like Fireye and let them design and arrange the potpourri of hardware and services a Fortune 500 company needs today to operate in a persistent state of cyber threat. We did purchase FireEye but believe you have to be careful what you pay. This is not one that is running away from you on day one.

Name: Coviello Arthur W Jr

Position: Director

Shares Bought: 4,800

Average Price Paid: $20.18

Company: FireEye Inc

Name: Sandfort Gregory A

Position: Director

Shares Bought: 4,280

Average Price Paid: $58.45

Company: Genesco Inc. is an American publicly owned specialty retailer of branded footwear and accessories and is a wholesaler of branded and licensed footwear based in Nashville, Tennessee. Genesco operates more than 1,475 retail stores throughout the United States, Puerto Rico, Canada, the United Kingdom, and the Republic of Ireland and wholesales branded and licensed footwear to more than 1,050 retail accounts through its various subsidiaries.

Buying at the top of a 52-week price range, Mr. Sandfort knows business at Genesco is good and getting better. but that probably has little to do with the purchase. Genesco is going through a broad refresh of its board which will grow Genesco’s board to nine members. This comes about five weeks after investment firm Legion Partners Asset Management proposed a slate of seven candidates to replace the entire Genesco board bar. The managers of Legion, who control nearly 6 percent of Genesco’s stock, say the company needs new strategic ideas and should sell off certain divisions.

This should be interesting. I wouldn’t interpret his purchasing stock as anything more than hey I’m on your board, I’ll take that money you pay me for attending board meetings and buy stock with it. There is nothing to lose and everything to gain. The question is, do we have anything to gain. The stock has been a proverbial dog with fleas but has run up on anticipation of moves by Legion Partners. Bottom line- it’s too late for us to play this game.

Name: Riley Bryant R

Position: CEO Chairman 10% Owner

Shares Bought: 33,316

Average Price Paid: $66.91

Company: B. Riley Financial’s diverse suite of services goes beyond traditional financial service offerings. By leveraging cross-platform expertise and assets, B. Riley Financial companies are uniquely positioned to provide full service, collaborative solutions to their clients at every stage of the business life cycle and in all market conditions.

Opinion: Riley is a money maker. For that alone, I’m following and buying. Bryant R. Riley has served as Chairman and Co-Chief Executive Officer of B. Riley Financial. B. Riley Financial. Financial services executive with extensive experience in investment banking, brokerage, corporate finance, and creative deal structuring with deep capital markets expertise. Currently Chairman and co-CEO of B. Riley Financial, a publicly traded, diversified provider of financial and business advisory services.

Name: Verdun Robert

Position: Director

Shares Bought: 50,000

Average Price Paid: $9.13

Company: This is from the Company’s PR, “UWM Holdings Corp. has been the #1 wholesale lender in the country for six consecutive years now — and with 20% market share and counting, it’s a title they intend to keep for many years to come. Because even after 35 years of exponential growth, they continue to expand our operations at an unprecedented pace as we follow a long-term plan developed to keep us ahead of the curve and strategically prepared to take full advantage of any future ebbs and flows of the mortgage industry.”

Opinion: We sold the $9 puts. That means we will buy a ton of it this coming week if it’s below $9 on Friday’s close. Why puts? Even though there is strong insider sponsorship by Verdun, UWM has become a fast-money Reddit Wall Street Bets crowd stock. This investing community is fickle, another way of saying I don’t understand them, and no one knows when they turn or how much buying power the crowd really has.

Mr. Robert A. Verdun is an Independent Director at UWM Holdings Corp., an Independent Director at SLANG Worldwide, Inc., and a Chief Executive Officer at Thirdwave LLC. He is on the Board of Directors at UWM Holdings Corp., SLANG Worldwide, Inc., and United Wholesale Mortgage LLC. Mr. Verdun was previously employed as President-Newmark’s Corporate Services Division by Computerized Facility Integration LLC.

Name: Sipes David

Position: CEO

Shares Bought: 43,000

Company:8×8 Inc. is an American provider of Voice over IP products. Its products include cloud-based voice, contact center, video, mobile and unified communications for businesses. According to the company, IIT began as a chip designer. The company produced coprocessors for microprocessors as well as graphics accelerator chips for the personal computer market during the late 1980s. The company later changed its name to 8×8 and began producing products for the video conferencing market

Opinion: Mr. Sipes David was appointed CEO on December 10, 2020. Most recently, as RingCentral’s Chief Operating Officer, he led product, engineering, and go-to-market functions for their 9 global offices and 350K+ customers worldwide. With robust and talented technology and a go-to-market team, they created a world-class customer-first culture, growing the company from $10MM per year to more than $75.

It’s a little hard to see in the chart above, but EGHT had been showing positive RSI divergence for two or three bars from 6-1-thru 6-3 after spending the previous two weeks basing on a steep decline and a few analyst downgrades. Some analysts see this industry getting more competitive, with Zoom (ZM) building a competitive phone offering from a video-first angle, RingCentral (RNG) continuing to grab large components of the market through distribution deals and Vonage (VG) enabling customization through embedded APIs.

EGHT reported revenue $144.7M, consensus $140.01M. “We surpassed our goal of achieving profitability ahead of schedule, driven by continued upmarket momentum in enterprise markets due to our differentiated, integrated cloud contact center and communications product,” said Dave Sipes, Chief Executive Officer at 8×8, Inc. “We sit at the center of massive markets migrating quickly to the cloud with a differentiated offering in which to capitalize on these substantial tailwinds.”Sipes had been waiting to buy stock as a new CEO and this was the 1st quarter with him at the helm. He had good instincts or luck when he bought. This is the perfect chart pattern for a bullish RSI divergence. EGHT has been on a tear but in recent weeks it’s topped out at $39.22. In comes, the new CEO with a $1 million dollar buy on 6-8. He’s up a quick 14.57% or $147,570 for two days. It’s hard to see on the chart above but EGHT is now bumping up against the 200 day moving average resistance. Hopefully, it will tread water and decline some at it is also in the stochastic overbought area. You have to be fast but this is a backup the truck buy.

Name: Morfitt Martha A M

Position: Director

Shares Bought: 4,800

Average Price Paid: $330.00

Company: Lululemon Athletica inc is a healthy lifestyle-inspired athletic apparel company for yoga, running, training, and most other sweaty pursuits, creating transformational products and experiences which enable people to live a life they love. Setting the bar in technical fabrics and functional designs, lululemon works with yogis and athletes in local communities for continuous research and product feedback. Lululemon has since expanded to sell its products internationally in 491 stores as well as online. The company has expanded to sell a variety of athletic wear, including performance shirts, shorts, and pants, as well as lifestyle apparel and yoga accessories.

Opinion: You can’t ignore the obvious success of Lululemon. It defined a category and turned the nations’ women into yoga pant wearers and spawned dozens of competitors. You also can’t ignore a $1.58 million dollar buy from Martha Morfitt. The challenger I see is that Lulu has been consolidating for some time while people try to figure out whether the end of the pandemic is going to slow down the explosive growth of the sportswear category. There is no doubt that the sundress and mini skirts are going to skirt the growth of loungewear but the stock has been consolidating for some time. I’m waiting for the next act. Maybe Morfitt knows what it is.

Name: Moskovitz Dustin A

Position: CEO Chairman 10% Owner

Shares Bought: 500,000

Average Price Paid: $39.49

Company: Asana Inc Asana is a web and mobile application designed to help teams organize, track, and manage their work. Forrester, Inc. reports that “Asana simplifies team-based work management. Asana helps teams orchestrate their work, from small projects to strategic initiatives. Headquartered in San Francisco, CA, Asana has more than 100,000 paying customers and millions of free organizations across 190 countries. Global customers such as Amazon, Japan Airlines, Sky, and Under Armour rely on Asana to manage everything from company objectives to digital transformation to product launches and marketing campaigns.

Opinion: Asana gave you two great buying opportunities. It pulled back to trendlines at the end of March and the beginning of May. Unfortunately, that’s only obvious in hindsight. Now it’s busted out of all technicals and the CEO just bought $20 million worth of stock as part of a 10b5-1 trading plan.

I have never seen a founder aggressively buying his company’s stock at such an elevated price when he owns so much of it. Dustin Moskovitz is the co-founder and CEO of Asana. It’s so rare that I don’t even know what to make of this ostensibly super bullish trade. As Asana’s CEO, Dustin is dedicated to creating a product that helps the world’s teams collaborate effortlessly, in addition to leading the company’s award-winning culture. Prior to founding Asana, Dustin co-founded Facebook and served as the company’s first Chief Technology Officer and VP of Engineering.

Name: Engebretsen James R

Position: Director

Shares Bought: 5,000

Average Price Paid: $101.42

Company: Federal Agricultural Mortgage Corp. Farmer Mac is committed to helping build a strong and vital rural America by increasing the availability and affordability of credit for the benefit of American agriculture and rural communities. As the nation’s premier secondary market for agricultural credit, They provide financial solutions to a broad spectrum of the agricultural community, including agricultural lenders, agribusinesses, and other institutions that can benefit from access to flexible, low-cost financing and risk management tools.

The Federal Agricultural Mortgage Corporation, commonly known as Farmer Mac, is a stockholder-owned, government-sponsored enterprise or “GSE” created by Congress to improve the availability of long-term credit for America’s farmers, ranchers, rural homeowners, businesses, and communities. Farmer Mac accomplishes this public policy mission by providing a secondary market for qualified agricultural mortgage loans, rural housing mortgage loans, rural utility loans (to cooperative borrowers made by cooperative lenders), and the guaranteed portions of agricultural and rural development loans guaranteed by the U.S. Department of Agriculture.

Opinion: James R. Engebretsen has been on the board since at least 2017. This is his first buy and it’s not a small one. Engebretsen spent $500k, doubling his ownership. Meanwhile, Zions Bank, a major shareholder, has been steadily reducing its holdings, selling its last remaining share on April 1. This undoubtedly has weighed on the price. On May 17th, Sidoti downgraded the bank with a price target of $115.

Name: Wallman Richard F

Position: Director

Shares Bought: 2,000

Average Price Paid: $453.25

Company: Roper Technologies Inc is a diversified technology company( that’s another way of saying they own dozens of companies you’ve never heard of) with annual revenues of $5.4 billion. Roper operates businesses that design and develops software (both license and software-as-a-service) and engineered products and solutions for a variety of niche end markets. Their strong operating capabilities enable them to convert end-market potential into profitable growth and cash flow in order to create value for their investors. Roper is a component of the S&P 500, Fortune 1000, and Russell 1000 Indexes and trades on the New York Stock Exchange under the symbol ROP.

Opinion:

This is Wallman’s 4th purchase of Roper since 2018. He is obviously comfortable with the name. Mr. Wallman served as the Chief Financial Officer and Senior Vice President of Honeywell International Inc., a diversified industrial technology and manufacturing company, and its predecessor AlliedSignal, from March 1995 to July 2003. Mr. Wallman has also served in senior financial positions with IBM and Chrysler Corporation. Mr. Wallman currently serves or has served as a director of Extended Stay America, Inc., Smile Direct, Wright Medical Group (formerly Tornier N.V.), Charles River Laboratories International, Inc., and Boart Longyear. He bought Smile Direct stock back in November which is another name we own.

Rover should have easy comparison quarterly earnings for the remainder of the year. It’s also had a number of analyst upgrades recently, including Argus, Barclay’s, and Oppenheimer.

Name: Global GP LLC

Position: General Partner

Shares Bought: 20,974

Average Price Paid: $27.18

Company: GLOBAL PARTNERS LP

Description:

Global Partners LP (NYSE: GLP) is an American energy supply company ranked 361 in the 2018 Fortune 500. The company is organized as a master limited partnership, and its operations focus on the importing of petroleum products and marketing them in North America. It wholesales products like crude oil, diesel oil, gasoline, heating oil, and kerosene. In March 2012, Global Partners acquired Alliance Energy, another company owned by the Slifka family that operated gas stations in the Northeast. In October 2012, Global Partners announced that it was buying a majority stake in two trans-loading facilities in North Dakota for a fee of around $80 million, expanding its presence in the Bakken region. It expanded in 2014 by acquiring the parent of Xtra Mart convenience stores

Opinion: This is one I would have liked to own back in November when I said Biden winning the election would be good for oil and gas-related stocks. I figured that whenever you made it more difficult to drill for oil and gas in this country, it would drive up the price of the underlying. Nothing like high prices of the underlying commodity to get the stocks working. I deliberately shied away from the midstream and services names and stayed with the E&P names. That was a mistake.

Name: Skonieczny Jr. Mark A

Position: CFO

Shares Bought: 7,000

Average Price Paid: $15.90

Company: REV Group Inc.

Description:

REV Group® is a leading designer and manufacturer of specialty vehicles and related aftermarket parts and services. They serve a diversified customer base, primarily in the United States, through three segments: Fire & Emergency, Commercial, and Recreation. They provide customized vehicle solutions for applications, including essential needs for public services (ambulances, fire apparatus, school buses, and transit buses), commercial infrastructure (terminal trucks and industrial sweepers) and consumer leisure (recreational vehicles). Their diverse portfolio is made up of well-established principal vehicle brands, including many of the most recognizable names within their industry. Several of their brands pioneered their specialty vehicle product categories and date back more than 50 years. REV Group trades on the NYSE under the symbol REVG.

Opinion: This buy was one of three small buys. Normally I wouldn’t bother to write about it but it is part of a cluster buy. It looks like insiders took advantage of the drop-in price caused by the spot secondary at $15.50 on June 9th

Name: Rushing Rodney M

Position: CEO

Shares Bought: 19,292

Average Price Paid: $15.87

Company: REV Group Inc.

Name: Snabe Jim H

Position: Director

Shares Bought: 10,000

Average Price Paid: $64.51

Company: C3.ai Inc.

Description:

C3 AI is a leading enterprise AI software provider for accelerating digital transformation. The proven C3 AI Suite provides comprehensive services to build enterprise-scale AI applications more efficiently and cost-effectively than alternative approaches. The C3 AI Suite supports the value chain in any industry with prebuilt, configurable, high-value AI applications for predictive maintenance, fraud detection, sensor network health, supply network optimization, energy management, anti-money laundering, and customer engagement.

Opinion: I don’t know if Snabe is a bottom fisher, or the other 10 or so officers and directors dumping stock and options have got it right. The founder of C3AI was one of the pioneers of CRM software. Siebel Systems was a software company primarily engaged in the design, development, marketing, and support of customer relationship management (CRM) applications. As an executive at Oracle, Siebel proposed the idea of creating enterprise software applications tailored for marketing, sales, and customer service functions. Oracle management declined his proposal. Siebel left Oracle to found Siebel Systems in 1993 to pursue that opportunity.[18] In 1999, Siebel Systems became the fastest-growing technology company in the United States.[19] Siebel Systems grew to over 8,000 employees in 32 countries, more than 4,500 corporate customers, and annual revenue greater than $2 billion before merging with Oracle in January 2006.[20]

Today Salesforce is the apparent winner in this space. Siebel has a second act. In 2009, Siebel founded C3.ai, originally to provide enterprise software for energy management.[21] C3.ai currently provides an enterprise AI software platform and applications for multiple commercial uses, including energy management, predictive maintenance, fraud detection, anti-money laundering, inventory optimization, and predictive CRM.[22] Its customers include 3M, Royal Dutch Shell, the US Air Force, and New York Power Authority.[23][24] C3.ai was included in the 2019 “CNBC Disruptor 50” list, with a valuation of $2.1 billion.[25]

I spent some time admittedly without great success trying to get a grasp on what C3.ai does. It’s always suspicious when businesses use a lot of timely acronyms and slogans to describe what they do and you still can’t understand it. I think this lengthy description from ZD Net is about as brief a description I can find.“C3.ai, the software company founded by software industry legend Tom Siebel, which on Friday filed to go public, describes its purpose in life as applying artificial intelligence to sales and marketing. What it is actually doing appears to be much more fixing the sins of infrastructure software such as Hadoop, and its commercial implementations by Cloudera and others.ZDNet examined what C3.ai calls its “secret sauce,” the artificial intelligence suite that it says speeds development of CRM.

It turns out, the secret sauce is really more about platform-as-a-service, rather than AI per se, which is funny, given that machine learning, a form of AI, is mentioned fifty-five times in the C3 prospectus, while platform is mentioned only once, in the company’s self-description: “We believe the C3 AI Suite is the only end-to-end Platform-as-a-Service allowing customers to design, develop, provision, and operate Enterprise AI applications at scale.”

What C3.ai has invented is a set of building blocks for putting together a system to analyze data coming from a variety of signals, including traditional databases, but also Internet signals such as social media, and, perhaps most important, sensors, including the kinds of sensors industrial companies might build into equipment in the field that they want to monitor…… The actual artificial intelligence component, at least based on C3.ai’s published materials, is fairly routine and nothing special.”

Whether this is truly unique and different from Domo, Tableau, and other business intelligence offerings is a question I can’t answer yet.

Name: Naylor Jeffrey G

Position: Director

Shares Bought: 2,500

Average Price Paid: $99.16

Company: DOLLAR TREE Inc

Description:

Dollar Tree, formerly known as Only $1.00, is an American chain of discount variety stores that sells items for $1 or less. Headquartered in Chesapeake, Virginia, it is a Fortune 500 company and operates 15,115 stores throughout the 48 contiguous U.S. states and Canada. Its stores are supported by a nationwide logistics network of twenty-four distribution centers. The Company operates one-dollar stores under the names of Dollar Tree and Dollar Bills. The Company also operates a multi-price-point variety chain under the Family Dollar banner.

Opinion: We blogged about Dollar Tree last week. There is really nothing more I can add. When a number of insiders buy or sell their stock that is referred to as cluster buying and selling. I consider that bullish or bearish accordingly.

Follow us on Twitter for real-time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019, 4th Best in November 2020, 4th Best in January 2021 (I kid you not)