Curious how well insiders are doing with their buys? Scroll the significant buys of the last year.

Last week, I started the blog saying, “at some point making money begins to matter. I’ve long scoffed at relative value analysis as a way to cultivate bad habits. It’s addictive and should be banned. Comparing companies by silly metrics as a multiple of sales versus a multiple of earnings seems insane yet the madness of crowd behavior is a well-documented phenomenon. It’s called bubbles and we’ve been in one for quite some time. I love bubble investing- just point me to the next one and make sure you’re not the one standing up when the music dies. One thing about insiders, they rarely fall victim to crowd euphoria egregiously overpaying for their stock. As the bubble bursts, you’ll see more insiders buying. In fact, every market correction for the last 20 years or as long as we have data for ends and only ends with a tsunami of insider buying. Causation or correlation is the correct question to ask. In either case, you can bank on it.

Ironically the first company that we are reporting on is one of the poster boys for overvaluation- NETFLIX. For all of you that have missed out on one of the truly great get-rich stocks of the last decade, read on to find out if this is the chance you’ve been waiting on. I daresay of the scores of analysts that were recommending the stock, this brief overview is more likely to make you money THAN any of the dozen or so illustrious Wall St. analysts. In fact, I can’t think of a profession where you could be so often wrong with such calamitous results and still have a job. Once again the oracle of Omaha says it better than anyone- “you pay a pretty penny for a cheery consensus.” Let me add, “and often a disastrous consequence.”

Name: Hastings Reed

Position: CEO

Transaction Date: 2022-01-27 Shares Bought: 51,440 Average Price Paid: $388.83 Cost: $20,001,609

Company: Netflix Inc. (NFLX)

Netflix Inc (Netflix) provides internet entertainment services for watching movies and television shows. The company offers TV shows and movies such as original series, documentaries, and feature films through an internet subscription on the TV, computer, and mobile devices. It offers DVDs by-mail service in the US. Netflix also operates a separate library of movies that can be watched instantly on subscribers’ TV through mobile applications, Netflix-ready devices, or computers. It licenses, acquires, and produces content, including original programming. The company markets and promotes its service through various marketing partners including multichannel video programming distributors, consumer electronics manufacturers, mobile operators, and internet service providers.

Netflix is headquartered in Los Gatos, California, the US. The company has approximately 222 million paid members in 190 countries. Netflix, Inc. was incorporated in 1997 and is headquartered in Los Gatos, California. As of December 31, 2021, Netflix had over 221.8 million subscribers worldwide, including 75.2 million in the United States and Canada, 74.0 million in Europe, the Middle East and Africa, 39.9 million in Latin America and 32.7 million in Asia-Pacific. It is available worldwide aside from Mainland China (due to local restrictions), Syria, North Korea and Crimea (due to US sanctions). Netflix has played a prominent role in independent film distribution, and is a member of the Motion Picture Association (MPA). Netflix can be accessed via internet browser on computers, or via application software installed on smart TVs, set-top boxes connected to televisions, tablet computers, smartphones, digital media players, Blu-ray Disc players, video game consoles and virtual reality headsets on the list of Netflix-compatible devices. It is available in 4K resolution. In the United States, the company provides DVD and Blu-ray rentals delivered individually via the United States Postal Service from regional warehouses.

Reed Hastings serves as Chairman of the Board, President, Chief Executive Officer of the Company. Mr. Hastings is an active educational philanthropist: he served on the California State Board of education from 2000 to 2004, and after receiving his B.A. from Bowdoin College in 1983 served in the Peace Corps as a high school math teacher in Swaziland. Mr. Hastings previously served on the board of Facebook, Inc. from 2011-2019.

Opinion: I like to say the market is really about people with conviction taking money from those that lack it. There is no more confident buyer than the corporate insider buying their own stock. Reed Hastings, the CEO, has forgone cash compensation for the last few years, taking home is $35 million compensation last year entirely in stock. When he bought $20 million in the Company’s stock last week that was a statement stronger than Bill Ackman’s 3 million share purchase with largely other people’s money.

Netflix like many NASDAQ poster boys has lost 50% of its value since November, culminating on January 21st after reporting earnings that beat but subscriber growth missed estimates. A little-noticed detail is that Netflix upped its monthly subscription fee to $20 per month for its most expensive plan. It’s the third price increase since 2019. I daresay anyone will abandon Netflix for a few dollars more per month. If there was one thing most TV and media watchers would shell out money for, it’s Netflix. After all, NFL football is free on local channels and it’s only for a portion of the year anyway. Netflix is the gorilla in the game and everyone else is a chimpanzee at best.

While the price hikes sting for consumers, it’s safe to expect they’ll continue and stick. Now all this great content and some not so great has come at a cost. Netflix has been on a debt-financed movie production binge and that will probably have to change somewhat. Netflix has created this great library of content by racking up $14.6 Billion in debt. There is little doubt in my mind that current operating cash flow can easily support the interest on the debt but the real question is can subscribers stick around without a steady stream of new and captivating content?

One of the big reasons Netflix needs to shell out so much dough is that competition is heating up. Streaming services are spending a frankly outrageous chunk of change on original programming, with global spend expected to exceed $230 billion in 2022, according to estimates from firm Ampere Analysis. Ampere positions Netflix as the third-largest investor in video content, surpassed only by Disney and Comcast — both of which the firm notes invest in pricey sports rights.

Can Netflix stop borrowing realms of money to support a fickle consumer now that Apple, Disney, NBC, Comcast, and Amazon which bundles it as part of Prome away have decided they have to play in the sandbox? This only makes Facebook and Google look genius in not having to pay a penny for their content as YouTube, Instagram and Facebook pay nothing at all for content as their gargantuan user base gleefully donates it for free. At least for now although some companies like Invisibly.com are trying to change that model. Invisibly founded by the co-founder of PayPal is trying to disrupt that model. More on that for another day, though.

There is also a question of how much would a prudent investor pay for Netflix stock though. For that answer, the esteemed Wall Street analysts that got you into overpaying for Netflix in the first place are all over the place on what to do with their recommendations now. Many downgraded the stock after the recent earnings call. I will provide you with a brief and somewhat hilarious summary of some of the comments from Flyonthewall.com.

- Goldman Sachs analyst Eric Sheridan lowered the firm’s price target on Netflix to $450 from $580 and reiterates a Neutral rating on the shares.

- Jefferies analyst Andrew Uerkwitz downgraded Netflix to Hold from Buy with a price target of $415, down from $737.

- Cowen analyst John Blackledge lowered the firm’s price target on Netflix to $600 from $750 and keeps an Outperform rating on the shares.

- Raymond Jame analyst Andrew Marok says the stock is appropriately valued after the Q4 report. The only sober comments I read.

- Canaccord analyst Maria Ripps lowered the firm’s price target on Netflix to $600 from $750 and keeps a Buy rating on the shares.

- Deutsche Bank analyst Bryan Kraft lowered the firm’s price target on Netflix to $465 from $580 and keeps a Hold rating on the share

- Truist analyst Matthew Thornton downgraded Netflix to Hold from Buy with a price target of $470, down from $690.

- Morgan Stanley analyst Benjamin Swinburne downgraded Netflix to Equal Weight from Overweight with a price target of $450, down from $700.

- Baird analyst William Power downgraded Netflix to Neutral from Outperform with a price target of $420, down from $575.

- Benchmark analyst Matthew Harrigan upgraded Netflix to Hold from Sell without a price target following yesterday’s 20% selloff in after-hours trading following the company’s “weak” Q1 member growth guidance. He is vacating his former $470 price target, though he now estimates the fair value at a slightly lower $450,

- BMO Capital analyst Daniel Salmon lowered the firm’s price target on Netflix to $650 from $700 but keeps an Outperform rating on the shares after its Q4 results and guidance.

- UBS analyst John Hodulik lowered the firm’s price target on Netflix to $575 from $690 but keeps a Buy rating on the shares

- Credit Suisse analyst Douglas Mitchelson downgraded Netflix to Neutral from Outperform with a price target of $450, down from $740

- JPMorgan analyst Doug Anmuth lowered the firm’s price target on Netflix to $605 from $725 and keeps an Overweight rating on the shares.

- Macquarie analyst Tim Nollen downgraded Netflix to Underperform from Neutral with a price target of $395, down from $615.

- Evercore ISI analyst Mark Mahaney downgraded Netflix to In Line from Outperform with a price target of $525, down from $710.

- Piper Sandler analyst Thomas Champion lowered the firm’s price target on Netflix to $562 from $705 and keeps an Overweight rating on the shares

- Pivotal Research analyst Jeffrey Wlodarczak lowered the firm’s price target on Netflix to $550 from $750 and keeps a Buy rating on the shares.

The Insiders Fund, the hedge fund I run, started a position in Netflix last week. Let me share with you some statistics I pulled from my favorite quick valuation tool Old School Value.

DCF valuation =$4.16

P.E. TTM =34.6

P/CF =33.8

Debt/Equity =101.17%

In summary, Netflix is exactly the kind of stock you don’t want to own in this new value-centric market and that’s just why it might work. Growth has been crushed. Greedy short sellers will want to cover and lock in their profits for a great monthly print and the 1-2 combination punch of Ackman and the $20 Million purchase by the CEO might be enough to get them scrambling. We bought it last week but I can’t say how long we will linger. Winter is not coming- it’s already here.

Name: Maclin Todd

Position: CEO

Transaction Date: 2022-01-27 Shares Bought: 2,000 Average Price Paid: $136.01 Cost: $272,020

Company: Kimberly Clark Corp. (KMB)

Kimberly-Clark Corporation, together with its subsidiaries, manufactures and markets personal care and consumer tissue products worldwide. It operates through three segments: Personal Care, Consumer Tissue, and K-C Professional. The Personal Care segment offers disposable diapers, training and youth pants, swimpants, baby wipes, feminine and incontinence care products, and other related products under the Huggies, Pull-Ups, Little Swimmers, GoodNites, DryNites, Sweety, Kotex, U by Kotex, Intimus, Depend, Plenitud, Softex, Poise, and other brand names. The Consumer Tissue segment provides facial and bathroom tissues, paper towels, napkins, and related products under the Kleenex, Scott, Cottonelle, Viva, Andrex, Scottex, Neve, and other brand names. The K-C Professional segment offers wipers, tissues, towels, apparel, soaps, and sanitizers under the Kleenex, Scott, WypAll, Kimtech, and KleenGuard brands. The company sells household use products directly to supermarkets, mass merchandisers, drugstores, warehouse clubs, variety and department stores, and other retail outlets, as well as through other distributors and e-commerce; and away-from-home use products directly to manufacturing, lodging, office building, food service, and public facilities, as well as through distributors and e-commerce. Kimberly-Clark Corporation was founded in 1872 and is headquartered in Dallas, Texas.

Mr. Maclin had a 37-year career at JPMorgan Chase & Co. and its predecessor banks, where he rose to Chairman of Chase Commercial and Consumer Banking in 2013 and served on the company’s Operating Committee. Mr. Maclin currently serves on The University of Texas Development Board, the Advisory Council for McCombs Graduate School of Business, the Executive Committee of The University of Texas Chancellor’s Council, the board of visitors of UT Southwestern Health System, the Steering Committee for the O’Donnell Brain Institute for UT Southwestern, and the board of Southwestern Medical Foundation and a member of its Investment Committee. Mr. Maclin also serves on the board of directors of RRH Corporation, the parent company of Hunt Consolidated, Inc.

Opinion: Maclin was appointed to the board in March of last year. This is his only purchase and all the stock he owns. No one else is buying and I recommend you don’t. All directors buy a perfunctory amount of stock and I daresay this covers his annual stipend for being on the Board. It’s a risk-free investment for Maclin but not for you.

Name: Vestberg Hans Erik

Position: CEO Chairman

Transaction Date: 2022-01-26 Shares Bought: 19,000 Average Price Paid: $52.55 Cost: $998,450

Company: Verizon Communications Inc. (VZ)

Verizon Communications Inc. offers communications, technology, information, and entertainment products and services to consumers, businesses, and governmental entities worldwide. Its Consumer segment provides postpaid and prepaid service plans; internet access on notebook computers and tablets; wireless equipment, including smartphones and other handsets; and wireless-enabled internet devices, such as tablets, and other wireless-enabled connected devices, such as smart watches. It also provides residential fixed connectivity solutions, including internet, video, and voice services; and sells network access to mobile virtual network operators. As of December 31, 2020, it had approximately 94 million wireless retail connections, 7 million broadband connections, and 4 million Fios video connections. The company’s Business segment provides network connectivity products, including private networking, private cloud connectivity, virtual and software defined networking, and internet access services; and internet protocol-based voice and video services, unified communications and collaboration tools, and customer contact center solutions. This segment also offers a suite of management and data security services; domestic and global voice and data solutions, including voice calling, messaging services, conferencing, contact center solutions, and private line and data access networks; customer premises equipment; installation, maintenance, and site services; and Internet of Things products and services. As of December 31, 2020, it had approximately 27 million wireless retail postpaid connections and 482 thousand broadband connections. Verizon Communications Inc. has strategic partnerships with Mastercard Incorporated and Project Kuiper. The company was formerly known as Bell Atlantic Corporation and changed its name to Verizon Communications Inc. in June 2000. Verizon Communications Inc. was incorporated in 1983 and is headquartered in New York, New York.

Hans Erik Vestberg serves as Chairman of the Board, Chief Executive Officer of the Company. Prior to assuming the role of CEO in August 2018 and the role of Chairman in March 2019, Mr. Vestberg served as Verizon’s chief technology officer and president of Global Networks from 2017, with responsibility for further developing the architecture for Verizon’s fiber-centric networks. At Verizon, Vestberg has focused on delivering seamless experiences for customers over network assets consisting of the country’s leading 4G LTE network, the largest 5G test-bed in the U.S., the nation’s biggest residential fiber network, a global internet backbone and undersea cable network carrying much of the world’s internet traffic, and fiber assets in 45 of the top 50 markets in the U.S.

Opinion: Last year Verizon paid its CEO, Vestberg, according to salary.com, As Chairman and Chief Executive $19,097,582 in total compensation. Of this total $1,500,000 was received as a salary, $3,637,500 was received as a bonus, $0 was received in stock options, $13,300,074 was awarded as stock and $660,008 came from other types of compensation. This information is according to proxy statements filed for the 2020 fiscal year.

Vestberg got a raise $1 million dollar raise last year. Investors lost 10% of their money in a year the market was up 28%. Considering the 4.8% dividend it wasn’t so bad. They just lost 5%. I can think of better things to buy. I daresay this is part of a mandatory stock ownership program as well but I just don’t care enough to spend the time researching it. He’s the only officer or director that has bought any stock at all in years. The only other officer or director in the last 5 years to purchase any shares was the CEO who also purchased $1 million worth of stock in February 2020 at $53.47. Two years later the stock is one dollar cheaper and he is no longer the CEO.

Name: Rippel John T

Position: Director

Transaction Date: 2022-01-21 Shares Bought: 10,000 Average Price Paid: $52.00 Cost: $519,970

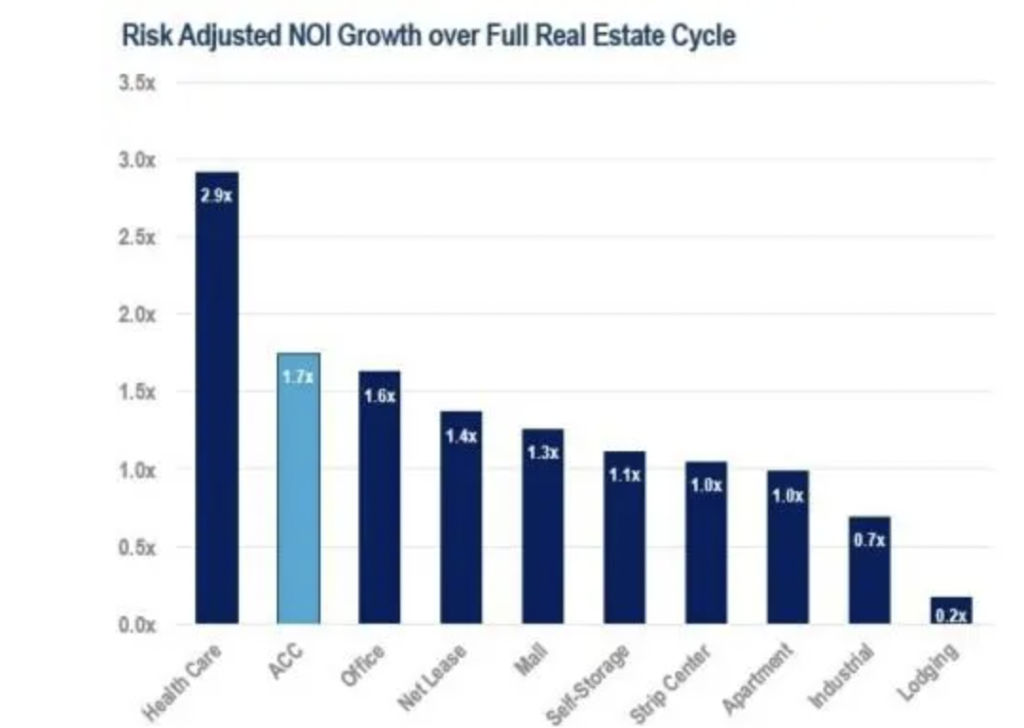

Company: American Campus Communities Inc. (ACC)

American Campus Communities, Inc. is the largest owner, manager and developer of high-quality student housing communities in the United States. The company is a fully integrated, self-managed and self-administered equity real estate investment trust (REIT) with expertise in the design, finance, development, construction management and operational management of student housing properties. As of September 30, 2020, American Campus Communities owned 166 student housing properties containing approximately 111,900 beds. Including its owned and third-party managed properties, ACC’s total managed portfolio consisted of 204 properties with approximately 139,900 beds. Blending their grassroots expertise, flexible approach and depth of resources, American Campus Communities delivers customized solutions to create the communities Where students love living. You won’t find a team more passionate about what they do. To attract and retain exceptional talent, they have created a work environment that is motivating and rewarding, allowing their employees to rise as high as their ambition, and earning ACC accolades including Great Place to Work Certification, Forbes Most Trustworthy Companies, NAHB Development Firm of the Year, and Texas Monthly Best Companies to Work for in Texas. they love what they do, and it shows. From their humble beginning in 1993 with four employees and a single management contract, ACC has become the nation’s largest developer, owner and manager of high-quality student housing communities. Housing more than 128,000 students on more than 90 university campuses across the nation, we’re dedicated to consistently providing every resident with an environment conducive to healthy living, personal growth, academic achievement and professional success.

John T. Rippel is a founding partner of Alliance Residential Company, one of the largest private U.S. multifamily companies, and has been its Chief Investment Officer since 2001 with responsibility for identifying development opportunities and directing the acquisition process for existing communities throughout the country. John began his multifamily career in 1982 as the partner in charge of south Texas development and acquisition for Trammell Crow Residential. In 1994, he led his division to the successful initial public offering of Gables Residential, where he served as a director and its President and Chief Operating Officer. Prior to joining Trammell Crow Residential, John was a CPA with Kenneth Leventhal Company, a national public accounting firm that is currently part of Ernst & Young LLP. John obtained his BBA from the University of Texas at Austin. Rippel will serve as an independent director of the company and as a member of the Audit Committee of the Board.

Opinion: This would be interesting as you would think two years of virtual campus education and outrageous college loans would be a damper on this college and university REIT. At least they would stop paying the dividend for a while as kids sit out the college experience. But guess what. Kids are content with virtual classes but they WANT the social experience. Zoom just doesn’t cut it when you want football games and house parties.

So if the business is so great, in the immortal world of Cuba Gooding in Jerry McGuire, “Show me the Money!” When schools start back up in full and this Covid-19 virus becomes an annoyance instead of a societal disrupter, you can expect ACC to start raising dividends. By the way, Tom Cruise got robbed of the Academy Award for Best Actor. At least Mr. Gooding took home the best supporting role. Dividend investors will be okay buying here but the stock has jumped a bit. I would wait for a point or two pullbacks. When you are depending on yield a point here or there adds up.

ACC pays a reasonable dividend of 3.65% and

Name: Moskovitz Dustin A

Position: CEO Chairman 10% Owner

Transaction Date: 2022-01-26 Shares Bought: 1,250,000 Average Price Paid: $48.97 Cost: $61,206,304

Company: Asana Inc. (ASAN)

Asana is a web and mobile application designed to help teams organize, track, and manage their work. Forrester, Inc. reports that “Asana simplifies team-based work management. Asana helps teams orchestrate their work, from small projects to strategic initiatives. Headquartered in San Francisco, CA, Asana has more than 100,000 paying customers and millions of free organizations across 190 countries. Global customers such as Amazon, Japan Airlines, Sky, and Under Armour rely on Asana to manage everything from company objectives to digital transformation to product launches and marketing campaigns. Asana, Inc. offers a work management platform. The Company’s platform enables teams to orchestrate work, from daily tasks to cross-functional strategic initiatives. With its solution, Asana enables individuals to manage and prioritize across each of the projects. Its solution enables individuals to collaborate with teammates and have visibility into each team member’s responsibilities and progress. The Asana solution aids the team leads to manage work across a portfolio of projects or processes. The Company enables executives to communicate company-wide goals, monitor status, and oversee work across projects to gain real-time insights into which initiatives are on track or at risk. Asana is powered by its multidimensional data model called the work graph. The work graph captures and associates work units, the people responsible for executing those units of work, the processes in which work gets done, information about that work, and the relationships across and within the data.

Dustin Moskovitz is the co-founder and CEO of Asana. As Asana’s CEO, Dustin is dedicated to creating a product that helps the world’s teams collaborate effortlessly, in addition to leading the company’s award-winning culture. Prior to founding Asana, Dustin co-founded Facebook and served as the company’s first Chief Technology Officer and VP of Engineering.

Opinion: Don’t get me started here. If the market for high P.E or no P.E stocks keeps selling off you might be able to buy ASAN a the IPO price last December 2020 at $21 per share. It remains one of my great mysteries in the stock market why a founder keeps buying his stock way over the price he sold it to the public for. Moskovitz is no doubt a smart guy and a billionaire but he doesn’t squat about stock market values. How could he? Not every stock turns into the cash cow that Facebook did. For that matter Silicon Valley billionaires are different than the rest of us- THEY HAVE MORE MONEY.

One word to Dustin- get a copy of Valuation: Measuring and Managing the Value of Companies (Wiley Finance) 7th Edition

Hey, I’ll even loan you mine.

Name: Shaw John Joseph

Position: Director

Transaction Date: 2022-01-25 Shares Bought: 30,000 Average Price Paid: $15.42 Cost: $462,711

Company: Ares Dynamic Credit Allocation Fund Inc. (ARDC)

Ares Dynamic Credit Allocation Fund, Inc. is a closed-ended fixed income mutual fund launched by Ares Management LLC. The fund is managed by Ares Capital Management II LLC. It invests in the fixed income markets of Europe. The fund primarily invests in debt instruments such as senior loans made primarily to companies whose debt is rated below investment grade, corporate bonds that are primarily high yield issues rated below investment grade, debt securities issued by CLOs, and other fixed-income instruments. It focuses on such factors as the overall macroeconomic environment, financial markets, and company specific research and analysis, to create its portfolio. Ares Dynamic Credit Allocation Fund, Inc. was formed on November 27, 2012 and is domiciled in the United States.

Ares Management Corporation (NYSE: ARES) is a leading global alternative investment manager offering clients complementary primary and secondary investment solutions across the credit, private equity, real estate and infrastructure asset classes. We seek to provide flexible capital to support businesses and create value for our stakeholders and within our communities. By collaborating across our investment groups, we aim to generate consistent and attractive investment returns throughout market cycles. As of September 30, 2021, Ares Management Corporation’s global platform had approximately $282 billion of assets under management, with approximately 2,000 employees operating across North America, Europe, Asia Pacific and the Middle East. Ares Dynamic Credit Allocation Fund, Inc. (“ARDC”) is a closed-end management company that is externally managed by Ares Capital Management II LLC, a subsidiary of Ares Management Corporation. ARDC seeks to provide an attractive level of total return primarily through current income and, secondarily, through capital appreciation. ARDC invests in a broad, dynamically-managed portfolio of credit investments. There can be no assurance that ARDC will achieve its investment objective. ARDC’s net asset value may be accessed through its NASDAQ ticker symbol, XADCX. Ares Capital Management II LLC (the “Adviser”) serves as the Fund’s investment adviser. The Adviser is an affiliate of Ares Management LLC (“Ares”). The Adviser’s investment philosophy, portfolio construction and portfolio management involve an assessment of the overall macroeconomic environment, financial markets and company specific research and analysis. Its investment approach emphasizes capital preservation, low volatility and minimization of downside risk. In addition to engaging in extensive due diligence from the perspective of a long-term investor.

John J. Shaw serves as Independent Director of the Company. Mr. Shaw is an independent consultant. In addition to serving as an Independent Director of ARDC, Mr. Shaw serves as an independent trustee of CADC. From 1995 to 2011, he was the President of the St. Louis Rams. Mr. Shaw joined the St. Louis Rams organization in 1980 acting first as Vice-President Finance, Controller/Treasurer from 1980 to 1982 and acting as Executive Vice-President from 1982 to 1995. Prior to joining the St. Louis Rams, Mr. Shaw worked for Arthur Anderson & Co. as a tax adviser from 1977 to 1980. Between 1985 and 2008, Mr. Shaw was a member of the executive committee of the NFL Management Council and has served as a member of the NFL Finance Committee as an executive committee member of NFL Properties. Mr. Shaw received his B.S. from the University of San Diego in 1973 where he graduated as valedictorian of his class and his Juris Doctor from New York University School of Law in 1976.

Opinion: Ok, let’s invest in junk bonds in Europe right before the possibility of the 1st major ground war in Europe in 40 years. I don’t think so but this is a strong bounce candidate if things get resolved peacefully. It does pay 7.58% in dividends but one look at the chart tells you that a 5% drop in share price and those dividends get wiped out by a loss in share price.

Follow us on Twitter for real-time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer-friendly and responsive I’ve used.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

Another source for insider buying and selling and much more is FinViz Elite. FinViz stands for financial visualization and they do an amazing job of providing reams of data and the tools to help you get to the bottom of it, the information that helps me make informed decisions and probable outcomes. I’ve been using their site for years and it only gets better over time.

This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky-dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. Do your own analysis. They can easily be wrong about, and in many cases, maybe most cases have no more idea what the future may hold than you or me. In short, you can lose money following them. We have and we curse aloud, what were they thinking!

We like Fly on the Wall for keeping up with what events might be happening, analysts comment, and whatever else could be moving the stock. Dow Jones news service is an essential tool but many services pick up their feed like they do Bloomberg. For quick financial analysis, it’s hard to beat Old School Value.

No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019