Curious about how well insiders are doing with their buys? Scroll through the blog posts and see for yourself

Before we dive deep into reading the tea leaves of insider buying, I want you to read this missive all the way to the end for our thoughts on Biovhaven BHVN. All I can say is Wow, wow, wow! It’s up a whopping 43.58% this last week. If you were paying attention, the modest Insider Report subscription fee paid for itself for a lifetime with the August 26th report.

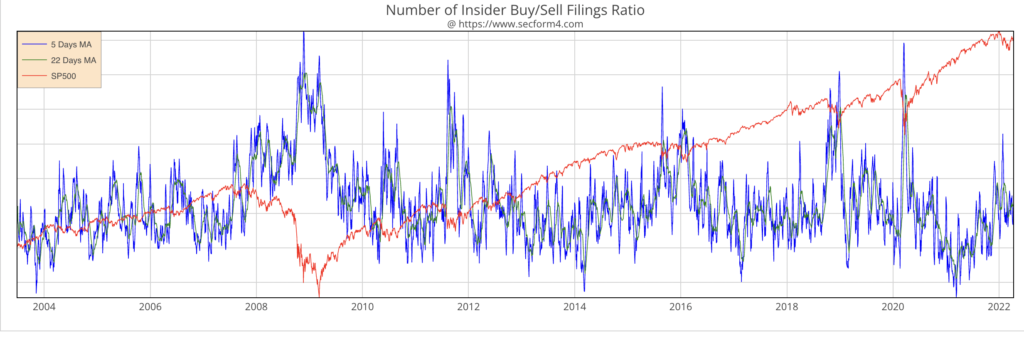

We are now deep into the quarterly earnings blackout, and most insiders are restricted from buying their company’s stock for one or more weeks, at least until the middle of October. All bear markets in the last 20 years have ended with a crescendo of insider buying. As you can see from the cadence of these reports and the insider buying/selling ratio below, we are nowhere near such a cathartic moment.

I wrote two weeks ago that we were sitting on support which I expect to be broken the following week. It collapsed as predicted. Don’t give me credit for being good at market timing or direction. If I could reliably predict either, I’d spend a lot less time analyzing insider behavior.

Nonetheless, there is some chance that this will end in a clearing event, aka crash. But then again it might take years to fix a decade of artificially low-interest rates. We do notice bottoming action although small. There are starting to be multiple buys in REITs and oil and gas drilling and maintenance services. We could very well be putting a bottom in those groups. After last week’s stunning collapse of the XLU, the utility ETF, we might see significant buying insider buying crop up in this sector.

Although we were surprised by the speed at which interest rates have risen, it’s hard to credit the sharp rise in interest rates to the collapse of the sector, but that’s all I can extrapolate. The XLU (utility industry ETF) was trading at $78.22 on September 12th, just three weeks ago at all-time highs. It closed Friday, October 8th at $63.78 for an 18% loss during that time.

That’s really remarkable for a historically stable part of the market. XLU has a 5yr beta of 0.54. That means it’s half as volatile as the market. I’ve been a sharp critic of modern portfolio theory since I was forced to learn it along the way to getting a Master of Analysis and Portfolio Management. Beta is the fundamental underpinning of modern portfolio theory. There is no way a sector ETF with a beta of half the market should lose 18% of its value when the market lost only 10% of its own. Beta is a backward-looking statistic and is useless in predicting the future. The collapse of the XLU is proof. It does support the maxim that past performance is no guarantee of future results, though.

One observation I hear a lot is that we had interest rates at this level for many years without crashing the stock market or the housing market. This is true, but the market was priced a lot lower, and so was your house. That’s not a prediction. It’s just math.

Name: Peter Busch Orthwein

Position: Director

Transaction Date: 2022-10-05 Shares Bought: 20,000 Average Price Paid: $72.50 Cost: $1,450,000.00

Company: Thor Industries Inc. (THO) America loves camping. Americans love the outdoors. Venture to any national park, and you will come to that conclusion, and many of them, more than ever, like doing that in an RV as opposed to hard ground and extensive prepping. The leading company in the business has over a one-year backlog they’re struggling to keep up with trading at a record 3.72 price-to-earnings ratio. Analysts have been downgrading Thor on rising costs, rising rates, and perceived reduced demand.

Thor Industries, Inc. was founded on August 29, 1980,[4] when Wade F. B. Thompson and Peter Busch Orthwein acquired Airstream from Beatrice Foods. The name “Thor” combined the first two letters of each entrepreneur’s name. Airstream had not fared well during the economic downturn of the late 1970s, losing $12 million the year before it was acquired Thompson and Orthwein had also previously acquired the Hi-Lo Trailer Company. Thor restructured Airstream and returned Airstream to profitability within one year.

Its portfolio of brands comprises Airstream, Bison, CrossRoads, Dutchmen, Jayco and Starcraft, among others. It is the world’s largest RV manufacturer. In North America, Thor operates and controls a 50% market share in a near duopoly with Berkshire Hathaway-owned Forest River, which sports a 30% market share. Oddly enough, both companies are headquartered in Elkhart, Indiana.

Peter Busch Orthwein serves as Chairman Emeritus of the Board of the Company. He retired from his position as Executive Chairman of the Company in 2019. Mr. Orthwein has served as a Director of our Company since its inception, Chairman of our Company from 1980 to 1986, Vice Chairman of our Company from 1986 to November 2009, and Treasurer of our Company from 1980 to November 2009. Our Nominating and Corporate Governance Committee and Board believe that his extensive experience with our Company and the industry makes him an asset to the Board.

Opinion: Thor is an exceptionally well-managed company, carefully gauging retail interest in order to align its production capacity in a rapidly changing macroeconomic environment. During its latest quarter, the Company reported Q4 EPS of $5.15 versus a consensus of $3.89 on revenues of $3.82B versus expectations of $3.68B.

I keep waiting for the earnings cuts and inventory build that would accompany the predicted downturn. Analysts are pegging the forward P.E ratio of 8.3 versus the absurdly low 3.5 P.E it is currently trading at. Soaring gas prices might be close to peaking even with OPEC’s latest output cut. The Baker Hughes drilling count has increased dramatically in the last 12 months. Give it another 12 months you possibly see oil in the $60s.

Co-Founder and Chairman Orthwein just purchased $1.45MM on the open market, his largest purchase in five years. Granted we are fighting the diminishing wealth effect, but even as it is, you can’t find a cheaper vacation short of sleeping on the beach and surfing in Nicaragua.

Management at Thor must be frustrated with the price action of the stock. With no controlling founder’s block of stock, I can see Thor being a private equity deal or leverage buyout. When interest rates normalize, a change of name and an AirStream IPO could be a hot deal.

Name: Matthew J Gould

Position: VP

Transaction Date: 2022-09-26 Shares Bought: 4,132 Average Price Paid: $21.15 Cost: $87,386.00

Transaction Date: 2022-09-26 Shares Bought: 8,868 Average Price Paid: $20.61 Cost: $182,734.00

Company: BRT Apartments Corp.(BRT)

Multi-family real estate is owned, managed, and developed by BRT, a real estate investment trust. A real estate investment trust firm is BRT Apartments Corp. The company’s main areas of interest include multi-family property ownership, management, and development. In addition, BRT owns and manages further real estate holdings. All of the company’s assets are made up of multifamily real estate properties, which are typically leased to tenants for a period of one year.

Businessman Matthew J. Gould has served as the CEO of 5 separate organizations. He currently holds the positions of Chairman of Gould Investors LP, Director and Senior Vice President of Majestic Property Management Corp., Chairman and Chief Executive Officer of Georgetown Partners, Inc., Chief Executive Officer of Rainbow Realty Group LLC, and Chief Executive Officer of Rainbow MJ Advisors LLC. Majestic Property Management Corp. is a subsidiary of Gould Investors LP. In addition, Mr. Gould serves as chairman of One Liberty Properties, Inc., director and senior vice president of BRT Apartments Corp., and senior vice president of REIT Management Corp. He is also on the boards of Sportsvite LLC and Halsa Holdings LLC. Both the University of Michigan and Yeshiva University awarded Mr. Gould undergraduate and graduate degrees.

Opinion: Multi-family has been the sweet spot of the REIT market. I don’t see that changing and with higher rates, more potential home buyers are priced out of qualifying for mortgages and locked into their apartments. Higher rates also mean that the hurdle for new development will be higher, lessening supply on the market. Existing multifamily players like BRT should be in the sweet spot once rates settle down which they are probably close to doing that after the rapid Fed hikes. Current dividend yield of 5.2% makes this a choice investment.

Name: Andrea Owen

Position: CEO

Transaction Date: 2022-10-03 Shares Bought: 60,606 Average Price Paid: $16.88 Cost: $1,022,963.00

Company: Herman Miller and Knoll furniture merged in July of 2021 to Inc to create a new company named Millerknoll Inc. (MLKN)

Chairman of HAY ApS, and President & Chief Executive Officer of MillerKnoll are all positions held by Andrea R. Owen. She is also a director of MillerKnoll. In addition to serving on the boards of 8 more businesses, Ms. Owen is a member of Business Leaders For Michigan and the Herman Miller Foundation, Inc. Prior to joining the Global Alzheimer’s Platform Foundation, Inc., Andrea R. Owen served as President of Banana Republic LLC and Executive Vice President & General Manager-Gap Global Outlet at Gap, Inc. The College of William & Mary is where Ms. Owen earned her undergraduate degree.

Opinion: This one is hard to read. The stock has been an absolute disaster since the merger sinking from a high of $50 to its current price the CEO paid per share at $16.88. I think I would be buying a million dollars worth of stock too to keep my job and show some confidence. I’m waiting to see if there are any other insiders following her down the path.

Name: Vlad Coric

Position: CEO

Transaction Date: 2022-10-05 Shares Bought: 485,775 Average Price Paid: $10.31 Cost: $5,009,425.00

Company: Biohaven Ltd.(BRT)

Name: John W Childs

Position: Director

Transaction Date: 2022-10-05 Shares Bought: 274,141 Average Price Paid: $8.98 Cost: $2,461,171.00

Company: Biohaven Ltd.(BRT)

BHVN) was introduced as a brand-new publicly listed business. As per the acquisition agreement with Pfizer (PFE) in May 2022, Biohaven has now formally started operating as a distinct, independent business. Vlad Coric, M.D., the company’s Chairman and Chief Executive Officer, established it with a little over $257.8 million in cash and no debt. Successful medication development and commercialization have a history at Biohaven. With a Prescription Drug User Fee Act goal date set for the first quarter of 2023, Biohaven’s New Drug Application proposal for zavegepant nasal spray was filed with the FDA and accepted for evaluation. Pfizer will now solely market and develop the Biohaven CGRP business internationally following its acquisition for a total price of around $13 billion, which includes the repayment of existing debt. About 3% of the newly formed spinoff business Biohaven is owned by Pfizer. Promoting a Wide Range of Innovative Candidates: Biohaven intends to advance a wide range of unique product candidates that are in the early and late stages of development that are intended to treat neurological and neuropsychiatric illnesses, particularly uncommon diseases with unmet medical needs. Treatments for epilepsy, pain and mood disorders, obsessive-compulsive disorder, spinocerebellar ataxia, and spinal muscular atrophy will be the focus of therapeutic development. The following are some important clinical development initiatives now under progress that make use of these exclusive technological platforms: For SCA and OCD, glutamate modulation is used; for diabetes and weight reduction, myostatin inhibition and neuromuscular illnesses are used.

The Chief Executive Officer of Biohaven Pharmaceuticals is Dr. Vlad Coric. Dr. Coric has more than 50 peer-reviewed papers and is also an Associate Clinical Professor of Psychiatry at Yale School of Medicine. He formerly held the positions of Director of the Yale Obsessive-Compulsive Disorder Research Clinic and Chief of the Yale Clinical Neuroscience Research Unit. He has held the position of president of the American Psychiatric Association’s district chapter in Connecticut, which has 800 members. At Bristol-Myers Squibb and Yale School of Medicine, Dr. Coric has more than 15 years of expertise in drug research and clinical development. Dr. Coric has experience working in cancer, neurology, virology, oncology, and immuno-oncology within the pharmaceutical business. Dr. Coric most recently served as the immuno-oncology indication lead for glioblastoma and neuro-oncology. At the Yale Psychiatry Residency Training Program, where he also held the positions of program-wide chief resident for the Yale Department of Psychiatry and chief resident on the PTSD team at the West-Haven Connecticut Veterans Administration Hospital, Dr. Coric finished his residency training. At Wake Forest University School of Medicine in North Carolina, Dr. Coric obtained his medical degree.

The chairman and partner of the private equity company J.W. Childs Associates, L.P. is Mr. John W. Childs. 1995 saw the co-founding of J.W. Childs Associates. Mr. Childs served as Senior Managing Director of the Thomas H. Lee Company from 1991 to 1995 before creating J.W. Childs Associates. He was in charge of initiating, researching, negotiating, and overseeing leveraged buyout transactions for the THL funds in this position. Prior to joining THL, for seventeen years. Mr. Childs worked for the Prudential Insurance Company of America, where he performed a number of senior roles in the investment sector before rising to the rank of Senior Managing Director in charge of the Capital Markets Group. In addition to serving as a director of Kosta Browne, Esselte, Mattress Firm, WS Packaging, and SIMCOM, he is now chairman of Sunny Delight. He served as Chairman of the Board of CHG Healthcare Services prior to its sale.

Opinion: Wow, wow, wow. I just can’t say how strange this trip has been. The stock is up a whopping 43.58% from Director’s Child’s last buy. We knew something strange was afoot when Director Bailey paid $5 million for Biohaven stock back in August before the Pfizer acquisition at $148.50 per share. The market was giving zero value to the stub of Biohaven stock remaining after Pfizer bought the Nurtec migraine franchise even though Biohaven’s management was going with the newco stub, BHVN.

There was and still is a shortage of information, but the market sure has a way of catching up quickly when insiders started buying the stub. The spinoff stub or whatever you want to call it was trading for $8 and change for a couple of days, and then insiders started buying. I was wondering why anyone would spend $5 million to buy a stock at $148.04 only to get $148.50 back the way the market was reading it.

Well here is your answer. Mr. Market made a major miscalculation. It’s these kinds of gems that the Insiders Report can uncover, but you have to be there with us unless you’re a qualified investor in The Insiders Fund, the hedge fund. We were buying this name at an even lower price than Bailey. Read what we wrote on 8-26-22, “Biohaven agreed to sell Pfizer its groundbreaking migraine drug business for $148.50 per share in cash. The rest of the company will be spun off. The existing management is going with the new company spin-off. Existing BHVN shareholders get $148.50 per share and 0.5 share in the NEWCO with closing expected during the 1st quarter. Getting NEWCO for free at this price with the proven Biohaven management looks like a deal to me. Director must have thought enough of it to tie up $5 Million for a few months”

The market clearly has no idea what the spinoff is worth, but when a successful management team goes with the NEWCO, that tells you something.

Follow us on Twitter for real-time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell the stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other within 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors. SECForm4 is one of the smaller ones but I like supporting Frank. He is not arrogant. He’s helpful and has great prices. He also trades on his own data so I like people that eat what they kill.

We publish a subscription newsletter called The Insiders Report. We offer a free 30-day trial so you have nothing to lose by trying it out. Be sure to carefully read the TERMS OF SERVICE.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course, insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believing they never make mistakes. Do your own analysis. They can easily be wrong, and in many cases, maybe most cases have no more idea what the future may hold than you or me. In short, you can lose money following them. We have and we curse aloud, what were they thinking!

We like Fly on the Wall for keeping up with what events might be happening, analysts’ comments, and whatever else could be moving the stock. Dow Jones news service is an essential tool but many services pick up their feed like they do Bloomberg. For quick financial analysis, it’s hard to beat Old School Value.

No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001 when I quit being an insider myself and devoted myself full time to managing my personal investments. Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019

[…] Childs knocked the ball out of the park by buying Bioven after Pfizer purchased the Company primarily for its migraine Nurtec franchise. I did not even know that there was a company left as the financial media portrayed it as Pfizer […]

[…] An old fave is back. Reassuring to see insiders buy after the stock has taken such a beating recently. We bought a […]