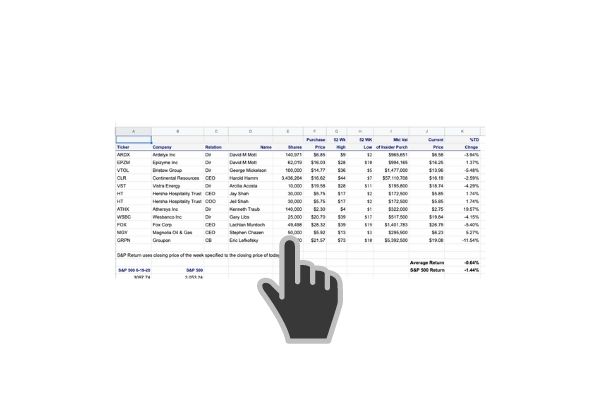

For trade details click on this link to the trades

insider-trading/1114483.htm”>Integer Holdings Corp up 19.94%

ViewRay Inc. up 20.92%

Camping World Holdings Inc. up 14.05%

Magellan Midstream Partners L.P. up 12.94%

Aon plc up 9.64%

CALIX INC up 9.59%

BlackRock Capital Investment Corp up 8.98%

PARSONS CORP up 9.29%

LIONS GATE ENTERTAINMENT CORP up 6.63%

GREEN DOT CORP up 4.80%

Vishay Precision Group Inc. up 5.37%

ASSURANT Inc up 4.47%

VERTEX PHARMACEUTICALS INC up 3.75%

TUPPERWARE BRANDS CORP up 3.49%

Dun & Bradstreet Holdings Inc. up 4.14%

Hanesbrands Inc. up 1.73%

NEW RELIC Inc up 1.02%

LOUISIANA-PACIFIC CORP down -0.57%

Stone Harbor Emerging Markets Total Income Fund down -0.49%

INTERNATIONAL BUSINESS MACHINES CORP down -0.86%

TEXAS CAPITAL BANCSHARES INC down -2.18%

Insider buys were up 9.22% versus the S&P 500 up 2.16% for the week

![]()

CEO Dziedzi purchased 5000 shares of Integer Holdings at $58.12. Integer Holdings Corporation (NYSE:ITGR) is one of the largest medical device outsource (MDO) manufacturers in the world serving the cardiac, neuromodulation, vascular and portable medical markets. The company provides innovative, high-quality technologies and manufacturing to Medical Device OEM’s to enhance the lives of patients worldwide. In addition, it develops batteries for high-end niche applications in energy, military, and environmental markets. Greatbatch™ Medical, Lake Region Medical™ and Electrochem™ comprise the company’s brands.

CEO Dziedzi last bought 3200 shares on 8-7-20 for $64.91. He’s fared better with this purchase, up 19% for the week. ITGR has struggled with growth over the last five years and we see no evidence that this is changing. We are not biting.

CEO Drake purchased 155,000 shares of ViewRay at $3.23. ViewRay® Inc., (NASDAQ:VRAY), designs, manufactures and markets MRIdian® the world’s first MRI-guided radiation therapy system that can image and treat cancer patients simultaneously. MRIdian addresses key limitations of existing external-beam radiation therapy technologies because it integrates MRI technology, radiation delivery, and proprietary software to locate, target, and track the position and shape of soft-tissue tumors while radiation is delivered.

While Covid has definitely been a headwind for many medical device companies, VRAY, no exception, we see little evidence as to VRAY gaining any financial traction in the market. We are not participating in this insider buy.

Director Adams made a huge purchase of 200,000 shares of Camping World Holdings at $24.55. This is noticeable as it’s the largest purchase by management other than the CEO Marcus Lemonis. Everyone knows that the pandemic has created a surge in camping and all outdoor activities. The jury is out though on once an effective vaccine is deployed on whether this camping surge will subside or represent a secular change. Millennials are taking to camping and likely to live the camping lifestyle for quite some time. CWH stock though seems to be mired in a trading range far below its August high price of $42.

Contrarian buyer Director Joung purchased 20,000 shares of Magellan Midstream Partners, MMP at $35.32. MMP has a 10% plus dividend yield. Joung is already up 12% on this purchase. Magellan Midstream Partners, L.P. is a publicly-traded partnership that primarily transports, stores and distributes refined petroleum products and crude oil-based in Tulsa, Okla. Don’t expect growth from this industry in secular decline but it will be a long time before EV vehicles replace combustion ones if every.

Contrarian buyer Director Joung purchased 20,000 shares of Magellan Midstream Partners, MMP at $35.32. MMP has a 10% plus dividend yield. Joung is already up 12% on this purchase. Magellan Midstream Partners, L.P. is a publicly-traded partnership that primarily transports, stores and distributes refined petroleum products and crude oil-based in Tulsa, Okla. Don’t expect growth from this industry in secular decline but it will be a long time before EV vehicles replace combustion ones if every.

Two buys this week at Aon plc. Chairman of the Board, Lester Knight continues to invest heavily in AON, purchasing 10,000 shares at $186.55. He last purchased shares on 5-13 with a massive purchase of 70,000 shares at $195 spending $13,65 Million. COO Brunoe bought 1000 shares at $186.46. The tea leaves are confusing, though, as the same week President Anderson sold 5,000 shares at $197.46

Aon plc is a large Anglo-American, Irish Domiciled global professional services firm that sells a range of financial risk-mitigation products, including insurance, pension administration, and health insurance plans. Aon has approximately 50,000 employees in 120 countries

We remain unimpressed as AON has macroeconomic risk to its global footprint. It doesn’t instill confidence when the President of the Company unloads $1 million worth of stock, either.

![]()

Director Listwin continues to accumulate sizeable amounts of Calix Inc. This time he purchased 20,000 shares at $22.53. Calix is a global provider of the cloud and software platforms, systems and services to deliver unified access networks and smart premises systems. The company was incorporated in 1999.

This is Listwin’s 4th buy-in at Calix since August. CALX appears to be having a very good year, According to Fly on the Wall Jefferies analyst George Notter raised the firm’s price target on Calix to $35 from $30 following the company’s “blowout” Q3 report and Q4 guidance. The analyst, who argues that the current work-from-home environment is a big positive for Calix on the broadband side, said his core thesis remains centered on Calix Cloud. Notter, in a note partially titled “Still Not Too Late to Own This!”, reiterated his Buy rating and said he views his estimates and target multiples for Calix as conservative. Unfortunately, the messaging is not so clear as two other directors are selling including Denuccio’s sale of 97,303 shares at $23.79 and Matthews sale of 10,000 shares at $24.09.

CEO Keenan bought 180,350 shares of BlackRock Capital Investment Corp at $2.64 per share. Insiders have been riding the down staircase here, steadily buying BKCC since since 2016 at ever lower prices. This is CEO Keenan’s largest purchase every although he did buy a similar dollar amount in March of this year at $4.14.

BlackRock Capital Investment Corporation provides middle-market companies with flexible financing solutions, including senior and junior secured, unsecured and subordinated debt securities and loans, and equity securities. This is similar to Golub and ARES Capital, all companies showing quite a bit of insider buying confidence. BKCC has been a lousy investment for years and we don’t see that changing.

CFO Ball bought 20,000 shares of Parsons at $30.25. He last purchased 30,000 shares in March at $29.40. Other insiders have purchased stock in this government IT contractor. Parsons’s focus is on security, defense, and critical infrastrucuture. Revenues have been steadily rising at PSN but the share prices haven’t participated in it. This could be changing and we’ve taken a small investment here.

Lion’s Gate Entertainment director Gordon Crawford purchased 20,000 shares of LGF.B at $8.31. Lion’s gate has a portfolio of hit movies and has been rumored as a buyout candidate for years. The pandemic has frozen out movie production and has hurt movie studios like Lions Gate. Crawford’s purchase might be heralding the end is near.

Director Wes Cummins purchased 10,000 shares in Vishay Precision Group. Vishay Precision Group, Inc. (VPG) is an internationally recognized designer, manufacturer and marketer of: components based on its resistive foil technology; sensors; and sensor-based systems specializing in the growing markets of stress, force, weight, pressure, and current measurements.

Vishay is reporting improved financial performance and a steady order book, above consensus revenue growth. As manufacturing moves back to the U.S, it’s possible that VPG sensors and weighing and control systems will be a beneficiary although commercial aerospace will be a headwind for some time.

Director Bruce Sachs bought 15,000 shares of Vertex Pharmaceuticals at $217.36 per share. There were other insiders selling but those were part of a predetermined sell program known as Rule 10b5-1. VRTX discovered and developed the first medicines to treat the underlying cause of cystic fibrosis (CF), a rare, life-threatening genetic disease. In addition to clinical development programs in CF, Vertex has more than a dozen ongoing research programs focused on the underlying mechanisms of other serious diseases.

We like this buy. Sachs looks like an opportunistic buyer as he sold shares in May at $269.8. VRTX sold off on the news of VX-814 showing liver toxicity leading to discontinuation of the program. Several analysts downgraded the stock but Citicorp analyst saw it as a buying opportunity. While disappointing, the selloff in the shares is “exaggerated,” Bansal tells investors in a research note. The analyst sees fair value for Vertex at $260-$270 per share on cystic fibrosis alone and he thinks the AAT contribution to the current market price was no more than $10-$15 per share. Also, the climate for biotech investing feels less hostile as it’s apparent that big pharma is the cure to the Pandemic, and price controls that will stifle innovation will not likely have broad popular whipping boy support in the crus of the pandemic. We are a healthy buyer.

Tupperware Brands after suffering for a long time has been on a tear this year. People have been eating at home and storing food goods in Tupperware. Director Goudis bought 27,500 shares of TUP at $28.64, near multi-year high. We should have anticipated this one but feel like at this point, we missed it and are not prone to chase. Tupperware once synonymous with food storage and prep has many competitors now.

Along the same lines as beneficiaries of stay at home is Hanesbrands. Director Ronald Nelson bought 80,000 shares of this underwear giant at $12.71-$12.73. This is so obvious. I can just visualize all these people working from home in their underwear and athletic wear. Do you ever wonder about the top-heavy Zoom calls? Is anyone wearing anything waste down besides underwear? HBI pays a healthy dividend of 4.63% at Friday’s closing price of $13.03.

Hanesbrands reported a small beat on Q3 earnings but provided a downbeat Q4 forecast on November 5th due to spiking cases and Covid restrictions in Europe. The stock plummeted 19.6% to $13.16. This looks like a heavy overreaction and we are buyers of HBI.

Director Henshall bought 4,750 shares of New Relic at $54.74. New Relic is a San Francisco, California-based technology company that develops cloud-based software to help website and application owners track the performances of their services. All the cloud-based software companies are overvalued in our opinion but that won’t stop us from jumping all over NEWR.

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer friendly and responsive I’ve used. This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believe they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001, when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019