For trade details click on this link to the trades

insider-trading/1653247.htm”>Waitr Holdings Inc. up 36%

PLx Pharma Inc. up 35.2%

GreenSky Inc. up 17.90%

TENNECO INC up 15.90%

SURO CAPITAL CORP. up 14.33$

Pandion Therapeutics Inc. 11.90%

MultiPlan Corp up 6.32%

AtriCure Inc. up 4.74%

MBIA INC up 4.70%

MORGAN STANLEY up 4.35%

Reynolds Consumer Products Inc. up 4.22%

Paramount Group Inc. up 0.52%

NATIONAL HEALTH INVESTORS INC down -2.38%

G1 Therapeutics Inc. down -6.59%

FLEXSTEEL INDUSTRIES INC down -9.05%

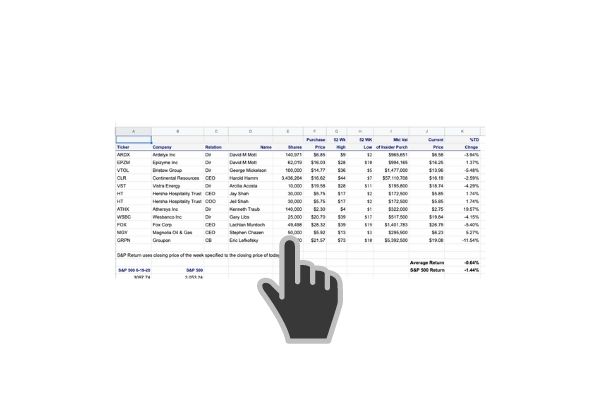

Director Ortale bought 266,113 shares of Waitr Holdings, a 2nd tier restaurant delivery service. WAITR was on their way to the waste dump of failed startups when the Pandemic breathed life into the business model. Now I wish they would expand to Park City. I should have paid heed when restauranteur and Houston Rockets owners Fertitta Tillman bought 1,000,000 shares at $1.42 back in August. Can this business model survive long term? Actually, does this matter when you could have made 32% in a week following Director Ortale? The company reported its 2nd consecutive quarter of continued profitability and operating cash flow.

PLx Pharma Chairman bought 264,900 shares at $3.78. Insiders have been steady if not huge buyers of stock all year, mostly at higher prices. PLXP has a Food and Drug Administration (FDA) approved lead product, Vazalore 325 mg. This is a novel formulation of aspirin that uses the PLxGuard delivery system to significantly reduce acute GI side effects while providing antiplatelet effectiveness for cardiovascular disease prevention as compared with the current standard of care, enteric-coated aspirin. Go figure aspirin has a new song and dance. These shares were purchased as part of a private placement and warrant package priced at $3.78 per share with a five-year warrant at $4.31 per share. This was a slam dunk for now, up 35%. We can’t chase this.

Chairman Zalik bought 1,105,220 shares of fintech online lender GreenSky, Inc. He was up 17.90% on this buy. Is there anything left? GSKY offers merchants immediate financing for their customers. They boast of 16,000 active merchants, 3.5 million satisfied customers with $26 Billion of funded loans. Home Depot is their largest single merchant customer, representing about 4% of total revenue for 2019. Affiliates of Renewal by Anderson represented 16% of revenues. The company has a concentration in the booming home improvement market.

Loans funded by their bank partners are not secured by collateral. While the company is not generally responsible for defaults by their customers, they have agreed to fund an escrow in order to provide a buffer against defaults. Perhaps this is what Citi analyst Cyganovich was referring to as complicated financials. They say their not responsible for defaults yet the 10k says they could lose money from them. It’s hard to have this both ways.

GSKY had a couple of recent downgrades. On November 16th Citi analysts reduced his price target from $4 to $3.50 and kept a sell rating on the stock following Q3 results. His cautious view was based on the company’s complicated financials and concentration risk in both merchants and bank partners.

In their 10k, they state that consumers who transact on our platform typically have super-prime or prime credit scores and find financing with promotional terms to be an attractive alternative to other forms of payment, particularly in the case of larger purchases. We provide a completely paperless, mobile-enabled experience that typically permits a consumer to apply and be approved for financing in less than 60 seconds at the point of sale.

Follow us on Twitter for real time insider buying alerts at https://twitter.com/theinsidersfund

[custom-twitter-feeds]

Insiders sell stock for many reasons, but they generally buy for just one – to make money. You’ve always heard the best information is inside information. Everyone who has any experience at all in the stock market pays close attention to what insiders are doing. After all, who knows a business better than the people running it? Officers, directors, and 10% owners are required to inform the public through a Form 4 Filing any transaction, buy, sell, exercise, or any other with 48 hours of doing so. This info is available for free from the SEC’s Web site, Edgar, although we subscribe to SECForm4 as they provide a way to manage and make sense of the vast realms of data. I’ve tried a lot of vendors and SECForm4 is one of the most customer friendly and responsive I’ve used. This is as close to “insider information” that an ordinary investor is likely to see- and it’s entirely legal.

BEWARE– Following insiders can be hazardous to your financial health unless you know what you are doing. Unlike the raw, unfiltered data, The Insiders Fund blog informs you of the purchases that count, the ones that are just window dressing into deceiving the public that all is hunky dory, and those that are just flat out other people’s money and should be just discarded like bad fish. As a rule, we only look at material amounts of money, $200 thousand or more, as anything less could just be window dressing.

The bar is different from selling because the natural state of management is to be sellers. This is because most companies provide significant amounts of management compensation packages as stock and options. Therefore, with selling, we analyze for unusual patterns, such as insiders selling 25 percent or more of their holdings or multiple insiders selling near 52-week lows. Another red flag is large planned sale programs that start without warning. Unfortunately, the public information disclosure requirements about these programs referred to as Rule 10b5-1 is horrendously poor. Also planned sales that just pop up out of nowhere are basically sales and are seeking cover under the Sarbanes Oxley corporate welfare clause. I also generally ignore 10 percent shareholders as they tend to be OPM (other people’s money) and perhaps not the smart money we are trying to read the tea leaves on.

Of course insiders can also be wrong about their Company’s prospects. Don’t let anyone fool you into believe they never make mistakes. No one tracks and understands insider behavior better than us. We’ve been doing it religiously since 2001, when I quit being an insider myself and devoted myself full time to managing my personal investments. They can easily be wrong about how much others will value them, and in many cases, maybe most cases have no more idea what the future may hold than you or I. In short, you can lose money following them. We have and we curse aloud, what were they thinking! Needless to say, past good fortune is no guarantee of future success. We may own positions, long or short, in any of these names and are under no obligation to disclose that. We welcome your comments on our analysis.

This blog is solely for educational purposes and the author’s own amusement. Investing with The Insiders Fund is for qualified investors and by Prospectus only. Nothing herein should be construed otherwise. THE INSIDERS FUND invests in companies at or near prices that management has been willing to invest significant amounts of their own money in. If you would like to hear more about how you can get involved with the Insiders Fund, please schedule some time on my calendar.

Prosperous Trading,

Harvey Sax

The Insiders Fund was the 4th best long-short equity fund in the world in 2019